Take into account these numbers: Underneath the Nationwide Infrastructure Pipeline (NIP) plan launched in 2020, roads and highways tasks account for ₹32.9 trillion, constituting 22.3 per cent of whole envisaged outlay for the programme. Price range 2023 noticed total allocations for capital expenditure for FY23-24 pegged at ₹10 lakh crore, inside which the allocation to Ministry of Highway Transport and Highways (MoRTH) stands at ₹2.7 lakh crore. This quantity is 35 per cent larger than the allocation for 2022-23. Along with this outlay, the Centre’s funding in NHAI for 2023-34 is ₹1.62 lakh crore, which is round 21 per cent larger than the earlier fiscal. The elevated allocation to MoRTH and NHAI brightens the prospects for the street sector, going ahead.

Listed here are the important thing metrics to look at when investing in street infra shares:

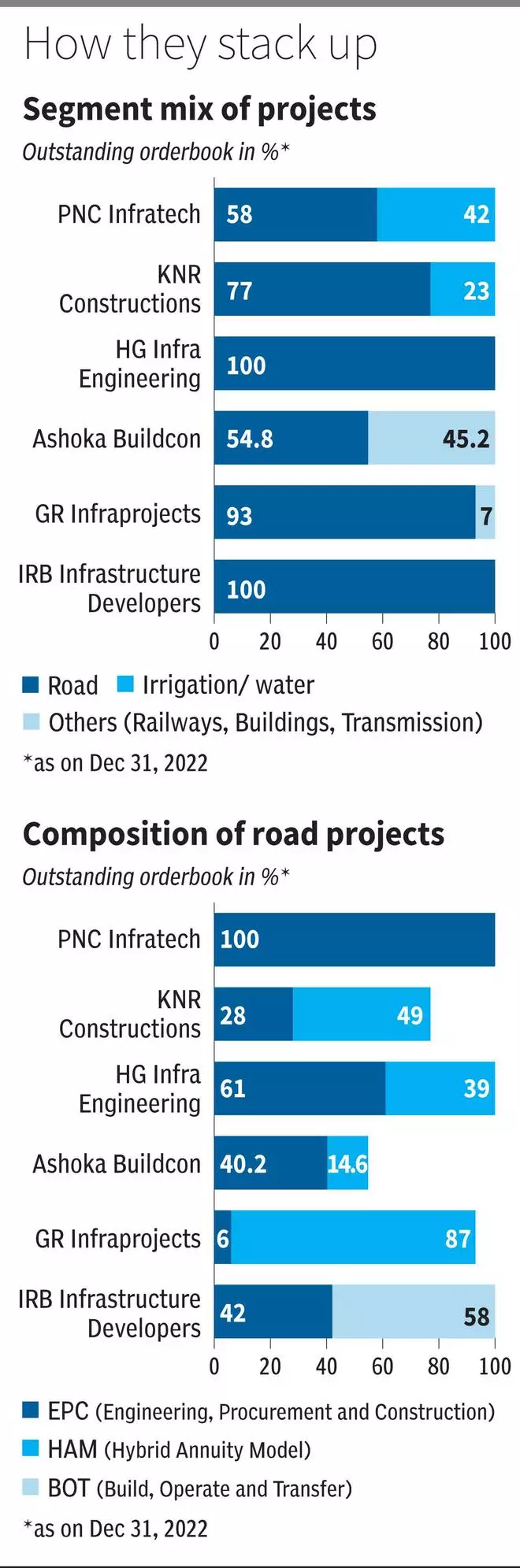

Mission combine

To grasp the roads sector, it’s important to know the sort of street tasks which might be often awarded to firms. In India, street building tasks are broadly of three varieties — EPC (Engineering, Procurement and Building), BOT (Construct, Function and Switch) and HAM (Hybrid Annuity Mannequin).

EPC contract is an easy one the place the entire value of the development of the street is borne by the federal government. The non-public contractor designs and lays the street and palms it over to the federal government. The cost to the contractor is as per the progress of the development. These tasks have comparatively low margin however are thought of very safe as the quantity is paid upfront and isn’t depending on elements like site visitors and toll assortment. PNC Infratech, Ashoka Buildcon and H.G. Infra engineering are amongst firms which have an EPC-heavy order guide.

BOT contract is a PPP (public-private partnership) mannequin. Right here, the contractor constructs, operates and maintains the street for a sure time-frame, known as the concession interval. Throughout this era, the developer collects toll costs from the individuals who use the street. On this mannequin, the developer wants to rearrange the financing, purchase the land, construct the venture, and hand it over to the federal government, publish concession interval.

That is probably the most most well-liked mannequin with regards to awarding of presidency tasks. The lengthy gestation and staggered revenues are a disadvantage. . Nonetheless, because the developer has to recuperate the funding from the toll income, the scope for profitability is excessive, which appeals to some gamers. IRB Infrastructure has a BOT-heavy order guide (58 per cent). IRB enjoys first rate rewards for the chance taken and has an EBITDA margin of 50-55 per cent at consolidated ranges.

HAM mannequin was launched in 2016 as an alternative choice to BOT, which had began to grow to be unviable. Right here, the federal government bears 40 per cent of the bid venture value, which can be paid in 5 equal instalments linked to venture completion milestones. The remaining 60 per cent of the capital introduced in by the developer can be repaid via semi-annual annuity funds by the federal government. The federal government may even service the curiosity on the mortgage taken by the developer — financial institution fee + 3 per cent. Since common annuities are paid below HAM agreements, firms can count on a daily stream of money flows. The margins in HAM are larger than EPC contracts however decrease than BOT tasks — a key cause being that in HAM, the contractor doesn’t acquire toll income.

Going by the proportion of tasks awarded, HAM and EPC fashions are equally fashionable now. As per an HDFC Securities report, out of 127 tasks awarded by NHAI and MoRTH in FY22, 62 (49 per cent) have been HAM tasks, whereas 63 (50 per cent) have been EPC and stability 1 per cent have been BOT tasks.

Order flows and execution

Whereas NHAI contract awards from FY19 to FY22 grew at a CAGR of 32.33 per cent (from 5,493 kilometres in FY19 to 12,731 km in FY22), the awarding in FY23 (April 2022-February 2023) noticed a 2 per cent decline year-on-year to 7,497 km. On the again of elevated budgetary allocation to MoRTH and NHAI, firms count on the order influx to choose up within the coming months.

The execution tempo from FY15 to FY21 was first rate as the common building per day of Nationwide Highways rose from 12 km in FY15 to 36 km in FY21. However there was a drop in FY20 — as firms confronted execution delays on account of a number of causes together with embargoes associated to air pollution management and State-level political upheavals.

In FY23 (April 2022-February 2023), the common building per day additional dropped to 24 km — this slowdown in freeway building has primarily been because of the extended monsoon in some elements of the nation, spike in uncooked materials costs and land acquisition points, amongst others. Nonetheless, firms appear assured on the tempo of execution selecting up in FY24, going by the administration commentary of listed gamers reminiscent of Ashoka Buildcon, H.G. Infra Engineering and PNC Infratech.

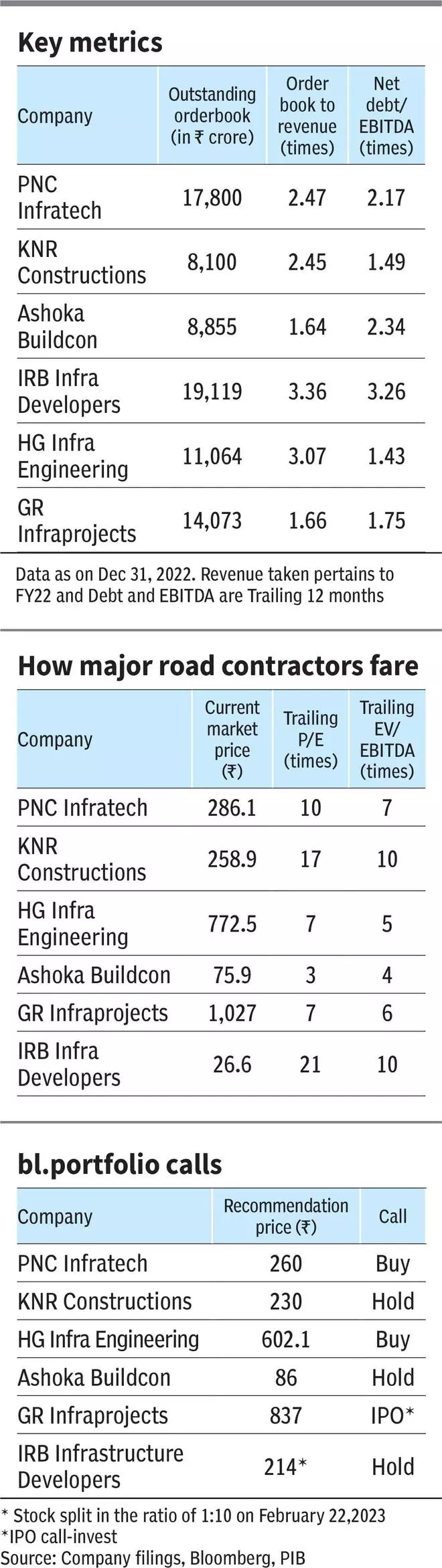

The order guide of a street building firm is the excellent work it has to execute. When seen within the mild of what number of years of income it covers, order guide provides an concept of the income visibility of the corporate.

As of quarter ending December 31, 2022, Ashoka Buildcon and G R Infraprojects have an order guide to income ratio of 1.64x and 1.66x. IRB Infrastructure, H.G. Infra Engineering, KNR Constructions and PNC Infratech have a better ratio of two.5 to three.5 occasions.

.jpg)

Profitability

Bitumen, asphalt, concrete and metals reminiscent of metal are key uncooked supplies for street gamers, with the prices being linked to petroleum merchandise and power costs.

Often, authorities tasks include a value variation clause that compensates the contractors for any spike in enter prices. In case of EPC contracts, the value variation clause hedges the contractor as the quantity is paid as and when venture progresses. Nonetheless, in case of HAM tasks, though the value variation clause is offered, the funds are made semi-annually; on account of staggered money flows, the contractor might face stress on the margins.

Take into account KNR Constructions, as an illustration. The corporate has 49 per cent of its order guide from HAM tasks with the remaining being EPC/BOT and Irrigation contracts. The administration said that the steep value rise in metal and cement has put stress on the margins (in 9 months FY23). The price of supplies rose 24 per cent whereas the income rose solely 14 per cent (in 9 months FY23). This appears to have triggered a decline of 90 foundation factors within the EBITDA margins YoY throughout 9 months ending December 31, 2022, and 350 foundation factors decline on QoQ foundation. However, PNC Infratech has an order guide of 58 per cent street EPC whereas the remaining are irrigation tasks, which appears to have helped in sustaining margins. The EBITDA margins of the corporate noticed a 191 foundation factors rise YoY in Q3FY23.

The administration of KNR Constructions has said that their EBITDA margins could be 15-16 per cent (yearly) with out irrigation venture however 19-20 per cent, with it. PNC Infratech has 42 per cent of its order guide from irrigation/canal tasks and Ashoka Buildcon 45 per cent of its order guide from Railways, Buildings and Transmission tasks.

Leverage

Highway building is capital-intensive and lengthy gestation debt isn’t unusual in these firms. Nonetheless, larger leverage in a rising fee situation might have a detrimental affect on the profitability of the enterprise. The rising rate of interest situation is especially a problem for HAM and BOT tasks as these require important debt for venture execution and the money flows are staggered over the concession interval of anyplace between 15 and 20 years. Firms typically resort to monetising the belongings by transferring to InvITs to repay the debt and free the fairness capital to spend money on newer tasks.

As an example, IRB Infrastructure Ltd. had a consolidated debt of ₹14,290 crore as on September 30, 2022, however in December 2022 quarter the corporate bought its HAM asset VK1 to IRB InvIT for ₹340 crore. The consolidated debt as per the administration is ₹13,260 crore as on December 31, 2022. The curiosity expense of the corporate at consolidated stage additionally diminished by ₹350 crore in 9 months FY23 in opposition to the identical interval the earlier yr. KNR Constructions is one other firm that has diminished its consolidated debt to ₹456 crore from ₹1,864 crore in September 2022 quarter, backed by sale of three SPVs.

Traders should subsequently weigh firms on the premise of the above parameters — together with the general exercise of presidency venture awarding and rate of interest cycles — so as to shortlist street infrastructure shares.

#elements #selecting #street #infra #shares