Provided that tier-2 is an extra choice given to buyers in order that they’ve some flexibility in withdrawals. It’s a voluntary saving choice, in contrast to the tier-1 funds that are retirement autos with guidelines on contributions, taxes and withdrawals.

Particularly, tier-2 funds additionally supply the identical choices as equities, company bonds and authorities securities as tier-1 schemes. You may make contributions to tier-2 schemes at any time and in addition withdraw quantities with none restrictions. In fact, you might be allowed to open a tier-2 account solely if in case you have an lively tier 1 NPS account.

Nevertheless, the one key distinction is that tier-2 schemes don’t take pleasure in any tax advantages.

Like tier-1 funds, many tier-2 funds have been round since 2009. And the fund administration prices stay very low – 0.09 per cent for the primary ₹10,000 crore property beneath administration (AUM). Some fund homes cost even decrease sums. Even when different transaction, upkeep and repair prices are considered, the bills are a lot decrease than every other market-linked funding.

As we did with the tier-1 schemes that had a monitor report of 10-plus years in our bl.portfolio version dated July 13, 2024, Selecting the Greatest Tier 1 Nationwide Pension System Fund, we evaluate tier-2 funds’ efficiency right here.

Particularly, we assess the efficiency of tier-2 NPS schemes over September 2014 to September 2024.

We additionally current the return state of affairs when fairness, company debt and authorities debt are combined in a hybrid set-up. We’ve ignored scheme A (different asset funds), as it’s but to select up considerably and property managed are nonetheless fairly insignificant.

Learn on to take an knowledgeable name about how you need to use tier-2 funds suitably regardless of it not having any tax advantages.

The methodology

We assume that ₹1 lakh is invested on the 15th of each September for the previous 10 years.

Then, utilizing the web asset worth (NAV) information and items collected over time within the case of fairness, company debt and g-sec schemes of varied pension fund homes, we calculate the XIRR (prolonged inner fee of return) proportion for the 10-year interval. That is much like calculating XIRR for an annual systematic funding in mutual funds.

The identical train is completed with the benchmarks. For fairness funds, we now have taken the Nifty 50 TRI because the benchmark.

Within the case of company debt and g-sec schemes, information on particular indices aren’t simply accessible.

Due to this fact, we determined to select from among the many prime 5-star-rated mutual funds from bl. portfolio’s Star Observe MF Rankings within the case of company debt. ICICI Prudential Company Bond Fund was taken for evaluating the efficiency of company debt schemes.

Within the case of g-secs, SBI Magnum Fixed Maturity was taken as a benchmark, because it had a wholesome monitor report in extra of 10 years, although there is no such thing as a ranking for the fund.

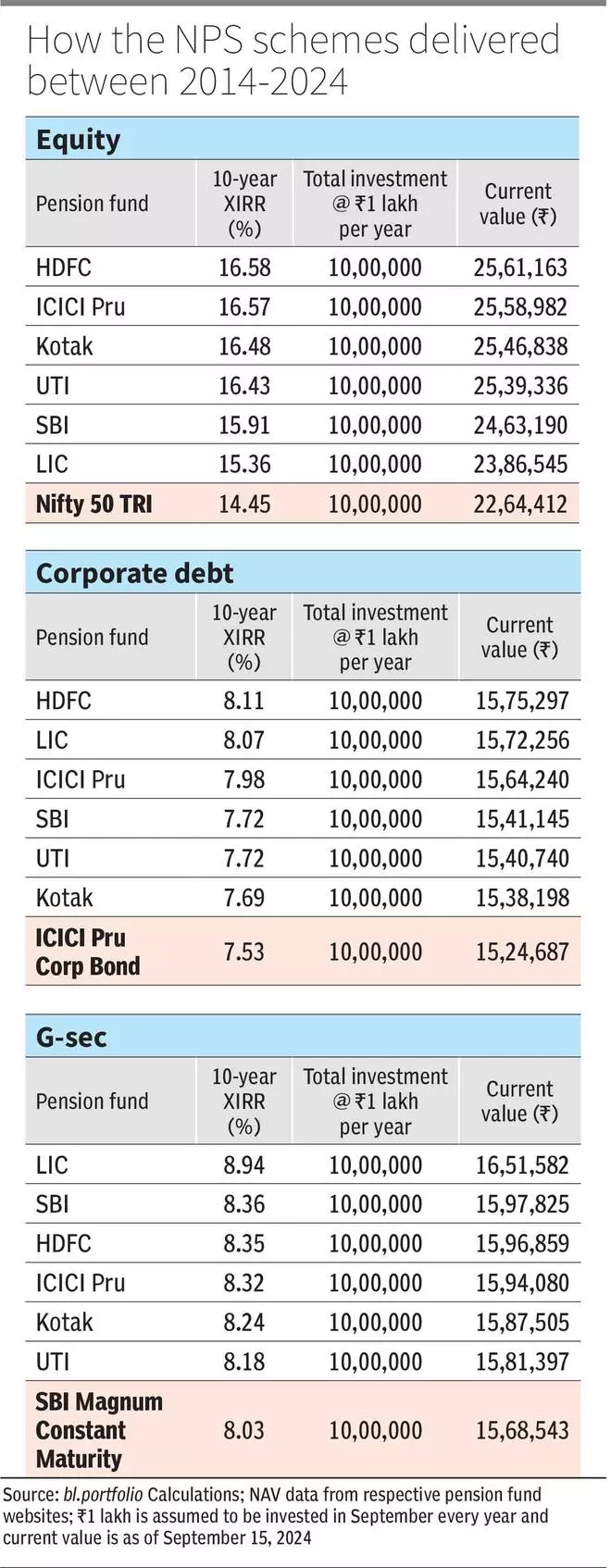

Solely six pension fund homes have a efficiency report of greater than 10 years with tier-2 schemes. Schemes of SBI, UTI, LIC, ICICI Prudential, HDFC and Kotak have been taken for evaluation.

All tier-2 funds outperform

Throughout classes, the evaluation of scheme performances reveals that each one fund homes have executed higher than benchmarks and delivered properly. Their XIRR was greater than these of the benchmarks we used.

Within the case of fairness funds (E), the six funds have delivered XIRR within the vary of 15.36-16.58 per cent over the 10-year interval. HDFC pension Fund topped the charts with 16.58 per cent returns, adopted by ICICI Prudential at 16.57 per cent. LIC recorded the bottom return, however was nonetheless affordable at 15.36 per cent.

The Nifty 50 TRI’s returns on an XIRR foundation over these 10 years stood at 14.45 per cent. Thus, all of the fairness schemes of all six fund homes beat the benchmark convincingly.

The small distinction in returns nonetheless become massive sums when taken over the long run. For instance, the ₹10 lakh invested over 10 years in HDFC’s fairness scheme gave over ₹25.61 lakh, whereas LIC’s fund was value slightly over ₹23.86 lakh, almost ₹1.75 lakh lower than the previous!

With respect to company debt schemes, once more, all of the six schemes outperformed the benchmark ICICI Prudential Company Bond Fund’s 10-year XIRR of seven.53 per cent.

HDFC as soon as once more topped the chart with 8.11 per cent, adopted by LIC at 8.07 per cent. Kotak’s scheme was comparatively lukewarm, at 7.69 per cent, however nonetheless outperformed our benchmark.

The distinction within the worth of the fund after 10 years between the perfect and worst performer was a comparatively low ₹37,099.

Lastly, with respect to g-sec schemes, LIC got here on prime with 8.94 per cent returns, adopted by SBI at 8.36 per cent and HDFC at 8.35 per cent. UTI’s fund was on the backside of the pack, although returns have been nonetheless affordable at 8.18 per cent returns.

All schemes outperformed the SBI Magnum Fixed Maturity Fund’s 10-year XIRR of 8.03 per cent.

The distinction within the fund worth of the perfect and worst performer was a comparatively massive sum of ₹70,185.

Deciding the perfect

To get a transparent image on which fund to decide on primarily based on completely different asset-class performances, we assumed ₹1 lakh could be cut up throughout the three classes. So, 50 per cent funding could be in equities (E), 25 per cent in company debt (C) and 25 per cent allocation to authorities securities (G) over the identical 10-year interval.

A 50:50 equity-debt hybrid fund construction is what we envisaged as a generic hybrid fund like case. Some buyers could have a unique allocation sample.

Primarily based on this allocation sample, HDFC got here throughout as the perfect pension fund home with an XIRR of 12.92 per cent, carefully adopted by ICICI Prudential at 12.88 per cent.

For perspective, a benchmark with 50 per cent Nifty, 25 per cent ICICI Prudential Company bond Fund and 25 per cent SBI Fixed Maturity Fund would have delivered an XIRR of 11.44 per cent over the September 2014-24 interval.

HDFC and ICICI Prudential pension fund homes might be thought of by buyers in the event that they intend to take a position throughout all three lessons.

However right here is a crucial level.

The NPS tier-2 funds take pleasure in no taxation advantages – whether or not within the type of deductions on the time of contribution or on the time of withdrawal. This has been clearly specified within the NPS Belief web site itself.

All positive aspects made in NPS tier-2 funds are added to your earnings and taxed on the relevant slab fee, regardless of the proportion of fairness and debt in your funding combine.

Does all this imply that these funds should be shunned? Not essentially. Provided that the expense ratio may be very low and returns moderately engaging, these schemes are nonetheless related.

The scheme selections C and G can be utilized for fixed-income allocation in your portfolio much like debt mutual funds, particularly as expense ratios are decrease than the latter and returns comparably good and even higher in some circumstances.

These wanting debt publicity alone by way of their NPS tier-2 funds can think about LIC and HDFC.

The place do schemes make investments?

The investments throughout classes in these schemes are considerably comparable with key holdings largely differing solely in weightages accorded to securities – fairness or debt.

When the scheme E of fund homes is taken, investments are principally within the top-100 market-cap shares.

Nevertheless, many of the tier-2 NPS funds limit themselves to large-cap shares from the Nifty 100 or largely to the Nifty 50 basket.

The likes of Reliance Industries, HDFC Financial institution, ICICI Financial institution, Infosys, TCS, L&T, HUL and Bharti Airtel determine within the portfolios of just about all of the six fund homes. The highest-five holdings account for 25-32 per cent of their portfolios.

With out moving into the frenzy of mid-cap shares or taking undue dangers, these funds have managed above-average returns over the long run.

In portion C, NPS funds aren’t allowed to take credit score danger of their bond investments. So, most of those funds put money into debt securities which can be rated AAA or AA for many half.

Bonds and non-convertible debentures of acquainted private and non-private sector corporations determine of their portfolios.

Debt securities of Bajaj Finance, Bajaj Housing Finance, NHPC, PFC, IOC, Reliance Industries, Shriram Finance, NaBFID, aside from SBI Infra bonds are generally held by tier-2 funds.

The holdings are additionally subtle, with the top-five holdings in most of those funds lower than 20 per cent of the portfolio.

The maturity profile is 4-15 years typically. Since investments are made to reputed company homes with rankings of AA or AA, the credit score danger is low.

Schemes investing in scheme G, too, have a good diploma of overlap when it comes to preferences for bonds.

NPS funds put money into authorities securities in addition to State improvement loans (SDLs). A superb a part of the g-secs of the Central authorities purchased are these maturing many many years from now. Some maintain g-secs maturing in 2064. Basically, most funds have securities maturing 15-25 years away.

The odd variation is funds investing in g-sec STRIPs maturing in 2029 or SDLs of Uttar Pradesh maturing in 2038.

Exposures to particular person securities are a bit extra concentrated with g-sec funds – the highest 5 holdings account for 33-50 per cent of the portfolio.

When rates of interest begin to decline and bond inflows change into heavy after India’s inclusion in world indices, yields could have a tendency downwards on longer-tenor authorities securities. This may increasingly end in a upmove in bond costs, thus aiding fund NAVs. In actual fact, even with none fee cuts in India, bond yields have fallen considerably within the final six months to 1 12 months.

Throughout asset lessons, NPS tier-2 stays a reasonable danger funding.

The tier-2 could not take pleasure in any tax advantages. However you’ll be able to think about using them for debt investments. You would additionally switch proceeds from tier-2 schemes to the principle tier-1 funds. You may swap the tier-2 to tier-1 on-line or strategy the middleman you employed to put money into the primary place. Tier-2 company bond and g-sec funds are taxed like debt mutual fund schemes. The benefit you have got is that there is no such thing as a TDS deducted and taxes are payable solely when positive aspects are realised. You may think about allocating, say, 20 per cent of your debt portfolio to those funds. In fact, the day you shut the tier-1 account, the tier-2 schemes would even be closed routinely.

#Selecting #NPS #Tier2 #Fund #Home