What binds them is the engaging valuations which the 2 banks are in search of within the IPO. At lower than 1.2x one-year ahead worth to e-book, Jana has actually held out a carrot to draw buyers. At 1.5x one-year ahead valuations, Capital additionally presents a proposition price contemplating. Although compared, the latter’s asking worth for its dimension of enterprise appears to be a tad greater, it’s properly inside the acceptable valuations for banks at 1–2x worth to e-book.

However past valuations, there may be nothing related between them. Whether or not when it comes to mortgage e-book composition, yield and margin profile or the enterprise focus, Jana and Capital are very totally different. What explains Capital’s marginally greater asking charges over Jana is its totally secured e-book over the latter’s 43 per cent share of unsecured loans. Nevertheless, contemplating that Jana is a a lot greater entity this shouldn’t be considered negatively.

As for dangers, buyers shopping for into each or both of the shares ought to be aware that the IPO is primarily to lift capital from the market and not one of the massive buyers in both financial institution are liquidating their holdings within the financial institution considerably. Nevertheless, publish itemizing, given the requirement to scale back the promoter holding to 40 per cent and subsequently to 26 per cent, one ought to brace for secondary market sale by promoters.

Jana SFB

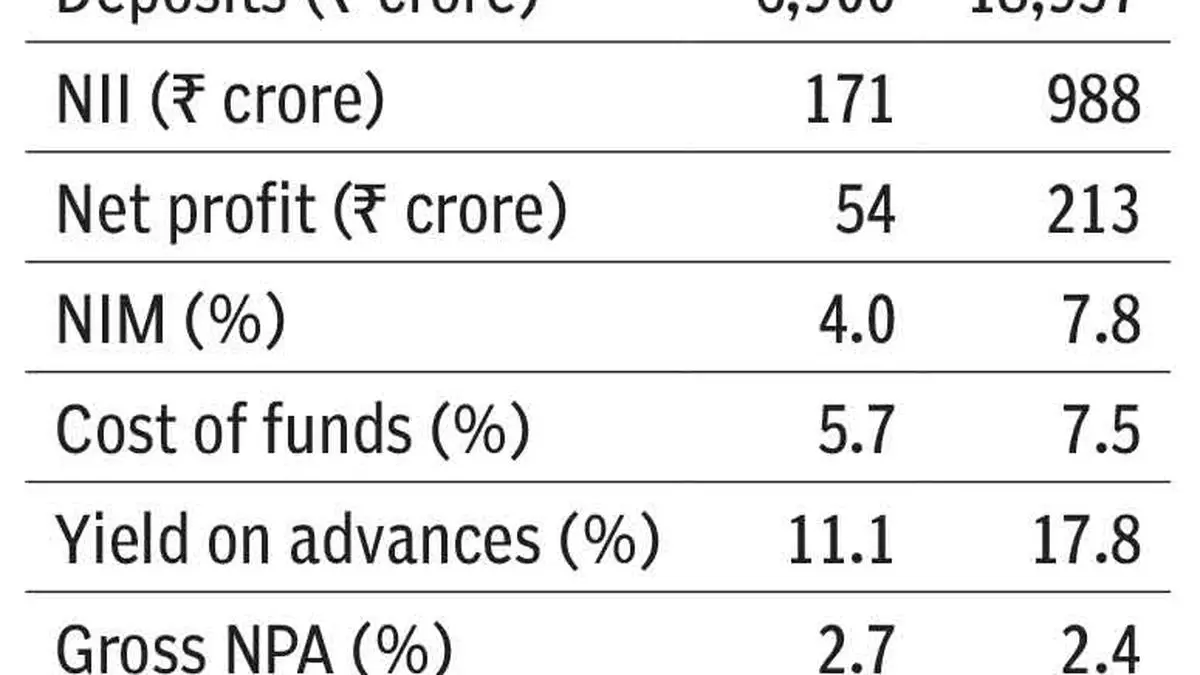

Within the two dangerous spells encountered by SFBs — 2016’s demonetisation and Covid which impacted the banking sector for nearly two years beginning March 2020, Jana was the worst affected. To that extent, previous efficiency is barely an indicator of the financial institution’s capabilities. What’s considerable although is the financial institution’s skill to remain targeted on increasing its secured loans e-book, which accounts for 57.4 per cent whole loans now, from round 40 per cent three years in the past. The financial institution rebounded in FY23 posting spectacular progress and return ratios (see desk). Having gone by way of crises and funding constraints prior to now, the financial institution has adopted a mannequin the place it’ll originate and sell-down a small a part of its MFI loans which helps the financial institution in preserving a lid on its unsecured loans and preserve wholesome capital pool, liquidity and yield on belongings. Immovable properties largely account for collaterals within the secured enterprise, with micro LAP and reasonably priced housing accounting for 32 per cent of whole loans, MSME loans account for 15 per cent, 7 per cent publicity to time period loans and the remainder cut up between mortgage towards deposits, two-wheeler loans and gold loans. That stated, in H1 FY24, unsecured advances accounted for 43 per cent of whole disbursements and buyers have to be careful whether or not this development persists. Additionally, because the share of secured loans enhance, NIM or internet curiosity margin (7.8 per cent in H1 FY24) might proportionally decline. Nevertheless whether it is maintained within the 7 – 8 per cent vary, buyers shouldn’t be involved.

Capital SFB

If Jana, like many different SFBs, is a case of microfinance lender changing to a financial institution, Capital SFB stands as the one native space financial institution to grow to be a SFB. To that extent, Capital’s enterprise mannequin is tried, examined and has withstood extra cycles. Aside from the truth that practically 100 per cent of its enterprise is secured, the distinctive promoting proposition is its main concentrate on small companies. Capital’s core mannequin is to make sure that your complete cash of a enterprise and/or the folks working it’s retained by the financial institution, whether or not as deposits and/or loans secured by some collaterals. The financial institution presents agriculture loans, MSME and buying and selling loans (for working capital, equipment purchases and many others) and mortgages (housing loans and loans towards property). In comparison with a pan-India outfit like Jana, Capital is basically concentrated in north India and operates out of Punjab, Haryana, Delhi, Rajasthan, Himachal Pradesh and Union Territory of Chandigarh. Being secured loans-focused, Capital’s NIMs are the bottom amongst SFBs at 4.04 per cent in H1 FY24. Whereas an enchancment in operational efficiencies and scale may assist transfer the needle, it’s seemingly that Capital might all the time stay a laggard within the section as all its friends are helped by a component of high-yielding unsecured loans, which may by no means be the case for Capital.

When it comes to asset high quality, Jana and Capital posted gross non-performing belongings of two.7 per cent in H1 FY24. Whereas 1.5 – 2 per cent gross NPA is changing into the appropriate threshold for SFBs, with a very secured e-book Capital’s numbers appear to be on the upper aspect. This can be due to greater share of restructured loans in the course of the Covid interval.

#subscribe #Jana #Capital #SFB #IPOs