Whereas Nifty 50, Nifty Midcap 150 and Nifty Smallcap 250 have gained 16, 28 and 29 per cent year-to-date (YTD), Nifty Financial institution has gained simply 6 per cent. The Nifty Midcap 150 and Nifty Smallcap 250 indices are at 18 per cent and 26 per cent premium to their five-year common P/E respectively. In the meantime, the Nifty Financial institution is simply at a 3 per cent premium to its five-year common value to guide worth.

Here’s a lowdown on the best way to use key banking metrics to establish good high quality banking shares.

Do be aware that you could be not need to calculate the ratios mentioned right here all by your self, since all of the banks lay naked these ratios of their investor shows. Simply understanding the place these ratios come from would suffice.

Web Curiosity Margin – Value of Deposits – Yield on Advances

Strain on the NIMs (Web Curiosity Margin) arising from banks’ want to lift deposits to fund credit score progress, on the one hand, and yields on loans coming off their highs, on the opposite, is a pattern seen in latest instances.

Since Value of Deposits(CoD) and Yield on Advances (YoA) closely affect NIM, it is sensible to have a look at them in unison reasonably than in isolation.

CoD is nothing however curiosity expended on deposits throughout a interval, divided by common deposits for that interval. Expressed in share, it signifies how a lot curiosity a financial institution pays its deposit holders. Typically, rate of interest on time period deposits is larger than that of financial savings accounts and banks don’t pay curiosity on present account balances. So, a financial institution with the next proportion of present accounts and financial savings accounts (CASA) will get pleasure from a decrease CoD.

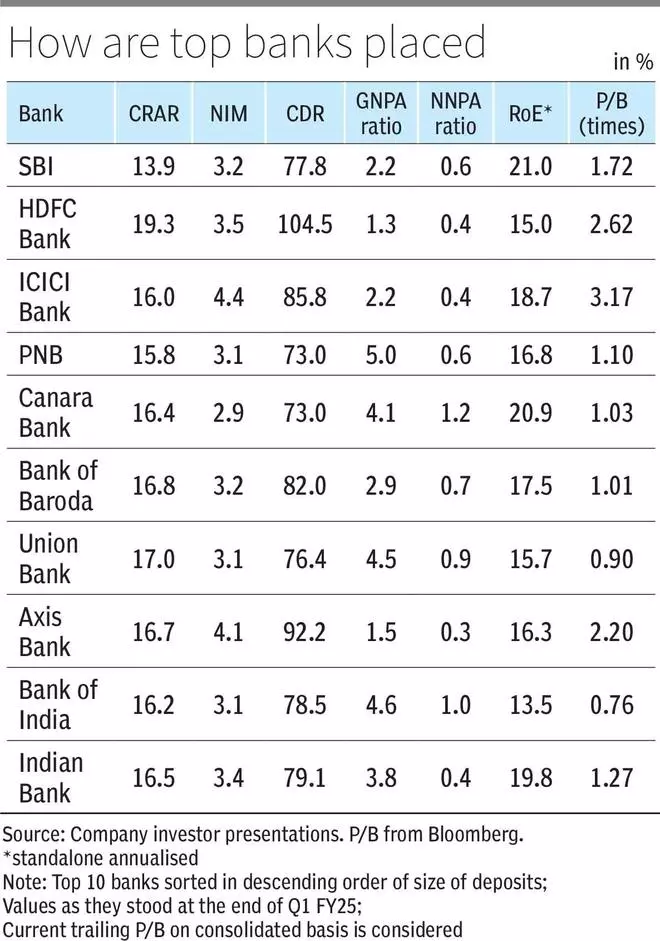

For instance, ICICI Financial institution, which has the next CASA ratio (CASA deposits divided by whole deposits) of 41 per cent, has a CoD of 4.8 per cent, whereas Karnataka Financial institution, which has a CASA ratio of 31 per cent, has a CoD of 5.5 per cent (Q1 FY25).

YoA is solely the curiosity earned on advances throughout a interval divided by common advances for that interval and it’s expressed in share. Mainly, it’s an indicator of how excessive a financial institution’s merchandise are priced. Banks typically value the loans proportionate to the danger that they undertake. A mortgage secured by a collateral may have a decrease fee of curiosity in comparison with one thing like an unsecured private mortgage. And so, banks with larger publicity to riskier loans — equivalent to private loans, bank cards and microfinance loans — have larger YoAs. That doesn’t imply that one ought to hunt for banks with larger YoAs. Whereas such loans have the next yield, there’s a excessive chance of their turning into delinquent and nugatory, if not successfully managed.

NIM is roughly the distinction between the speed (%) at which a financial institution earns curiosity and the speed at which it pays curiosity. A financial institution earns curiosity on loans and investments and pays curiosity on deposits and borrowings. NIM is calculated as internet curiosity earnings earned (curiosity earned minus expended) throughout a interval divided by common curiosity incomes property (loans and investments). CoD and YoA are the main determinants of NIM. A decline in YoA and/or an increase in CoD will have an effect on NIM adversely and a rise in YoA and/or decline in CoD will affect NIM favourably. For instance, in Q1 FY25, Canara Financial institution shed 5 bps of YoA (QoQ) and noticed 20 bps rise in CoD, leading to NIM slipping by 15 bps. Given two related banks, the one with the next NIM is the higher of the 2, supplied it exudes high quality in different facets, equivalent to asset high quality.

Credit score deposit ratio (CDR)

Excessive CDRs have been hitting the headlines within the latest quarterly outcomes of banks, with banks discovering it tough to lift deposits to fulfill the demand for credit score. CDR is the ratio you get while you divide the stability of advances by that of deposits at a selected level of time. For e.g., as of Q1 FY25, State Financial institution of India had advances value round ₹38 lakh crore and deposits value ₹49 lakh crore, making its CDR 78 per cent.

Banks are statutorily required to maintain 4.5 per cent of deposits as reserves with the RBI (CRR) and one other 18 per cent in liquid property equivalent to gold, authorities securities and money (SLR). This aside, banks want to keep up Excessive High quality Liquid Belongings (HQLAs) as a part of their LCR (Liquidity Protection Ratio), massive sufficient to fulfill 30-days’ value of internet outgo from deposits beneath confused circumstances. This leaves banks with a ballpark 75 per cent of deposits to disburse as loans.

Nonetheless, if a financial institution has sufficient borrowings (equivalent to bonds) or sizeable personal funds from its capital to lend out, it might afford to have the next CDR, although at the price of larger curiosity on such bonds consuming into the NIM. For instance, a sure bond of HDFC Financial institution, maturing after 94 months, is obtainable out there with a coupon fee of 8 per cent, whereas the financial institution is providing time period deposits at 7 per cent for a similar maturity. Right here, the price of the bond is larger than that of deposits. In such a case, if a financial institution have been to defend the NIM, it might have to search out methods to spice up the YoA; disbursing riskier loans (assuming high quality loans) being one among them.

HDFC Financial institution has a CDR of 104.5 per cent, pushed by the merger of erstwhile HDFC Ltd’s advances/loans with that of the financial institution. The merger additionally resulted within the financial institution taking up the high-cost borrowings of HDFC Ltd., which has led to erosion of NIM put up the merger. Problem of additional bonds for incremental loans may solely dent the NIM. The administration has guided for mortgage progress to be sluggish in FY25.

SBI, however, is comfortably positioned with a CDR of 78 per cent (even stronger at 69.3 per cent with respect to home operations) and is sitting on a pile of extra SLR property of ₹3.7 lakh crore. Therefore, not like HDFC Financial institution, SBI’s administration has guided for a powerful 15 per cent mortgage progress this fiscal.

Asset high quality ratios

Over the higher a part of the previous decade, shares of personal banks commanded a premium over their public sector counterparts, for the straightforward motive that their asset high quality was superior as compared. Recently, public sector banks too have upped their sport on this regard, with a few of them making an excellent case for funding. Listed below are 4 key measures to evaluate the asset high quality of a financial institution — GNPA ratio, NNPA ratio, PCR and credit score price.

The Gross NPA ratio measures Gross Non-Performing Belongings (GNPAs) as a share of advances. A Non-Performing Asset is one the place curiosity due on a mortgage has not been serviced by the borrower for greater than ninety days. The Web NPA ratio measures Web NPAs (Gross NPAs minus provisions) as a share of advances. It’s fascinating to have each these ratios at ranges as little as attainable.

The Provision Protection Ratio (PCR) measures the extent to which the Gross NPAs have been supplied for. A better PCR and decrease NNPA ratio point out conservative stance of the administration in recognising dangerous loans. However it will have a bearing on earnings.

Credit score price is a ratio of provisions and write-offs to common advances. Once more, the next credit score price would imply decrease earnings. As soon as legacy dangerous loans are supplied for/written off and because the high quality of underwriting incremental loans improves, credit score price will naturally pattern downwards and earnings will enhance.

For instance, in FY20, Punjab Nationwide Financial institution had a GNPA ratio of 14.2 per cent and a credit score price of two.9 per cent. As asset high quality improved over time, the GNPA ratio and credit score price as of Q1 FY25 stand at 5 per cent and 0.32 per cent respectively. Consequently, the financial institution’s valuation (value to guide worth) has gone up from about 0.4x in June 2020 (when FY20 numbers have been launched) to 1.09x now.

Capital to Danger-weighted Belongings Ratio (CRAR)

CRAR signifies the buffer a financial institution has towards sudden losses. It’s calculated by dividing a financial institution’s capital funds by its Danger-weighted Belongings (RWA). RWA is the sum of a financial institution’s numerous property multiplied by their respective threat weights. Riskier property have larger weights.

Capital funds is the sum of CET-1 (Widespread Fairness Tier-1), AT-1 (Further Tier-1) and Tier-II capitals. CET-1 roughly consists of share capital, securities premium, statutory reserves and different free reserves and assumes the very best significance of the three. It’s because, CET-1 capital is of the very best high quality of the three and the primary to soak up losses in stress situations.

As per RBI norms, the minimal CRAR is 11.5 per cent and minimal CET-1 is 8 per cent (5.5% + capital conservation buffer of two.5%). A better ratio means the financial institution is healthier positioned to deal with monetary stress. Whereas a CRAR larger than the regulatory minimal could also be advantageous in instances of economic stress, too excessive CRARs might counsel under-utilisation of capital assets. You will need to have a radical contextual understanding earlier than judging a financial institution’s CRAR as too excessive.

At a given degree of capital funds, the identical financial institution, when it has larger degree of dangerous property equivalent to unsecured private loans, may have a decrease CRAR than when in any other case. Right here’s a simplified illustration to know this. Assume a financial institution’s capital funds to be ₹100 and its mortgage guide consists of ₹300 in housing loans and ₹300 in unsecured private loans. The chance weights for housing loans and unsecured private loans are 50 per cent and 125 per cent respectively. The RWA on this case could be ₹525 (300*50% + 300*125%) and the CRAR could be 19 per cent (100/525). In the identical illustration, if the proportion of private loans have been to be larger, say ₹400, and housing loans have been to be ₹200, then the CRAR would come all the way down to 16.7 per cent (100/(200*50% + 400*125%)).

Valuation, the final word choice maker

Assessing banks on the metrics defined above is simply half the job. Good investing choice is determined by the valuation at which to procure the shares.

With regards to banks, value to guide worth (P/B) is the extensively used valuation metric. It’s obtained by dividing the market cap of a financial institution by its internet property (guide worth). The ratio captures earnings additionally to an extent, as the expansion in internet property largely comes from internet earnings ploughed again into enterprise.

The premium in value over the guide worth will rely upon one’s confidence within the sustainability and trajectory of future earnings. An vital think about assessing that is the financial institution’s RoE (Return on Fairness = internet revenue divided by internet property). RoE is a measure that captures how productively/effectively a financial institution is making use of its internet property or guide worth.

Think about two banks A and B. A has a P/B of 1.5x and B a P/B of 2x. A’s RoE is 10 per cent, whereas B’s RoE is 20 per cent. Taking a look at P/B in isolation leads one to conclude that A is cheaply valued. Nonetheless, taking a look at P/B in tandem with RoE, B is the higher valued financial institution, because it instructions a premium for its larger RoE. Thus, when evaluating the financial institution in query, buyers can use the pair — P/B and RoE — in evaluating the financial institution with friends of comparable measurement.

This aside, taking note of different qualitative facets equivalent to company governance and materials litigations is completely important. As an illustration, if one have been to have a look at the stable fundamentals of Tamilnad Mercantile Financial institution, she or he would conclude that the financial institution is brutally undervalued, relative to friends. However the reality is that, there are a number of legacy litigations in relation to the share capital of the financial institution which are weighing in on the share value, thereby proscribing a premium valuation. Right here is the place qualitative judgements are available. If one believes the legacy litigations within the case of TMB could be resolved, then the inventory will see a re-rating, else it might flip into a worth lure. Traders must assess the implications of such qualitative facets, earlier than taking the funding name.

SOTP

Prime banks equivalent to SBI, HDFC Financial institution and ICICI Financial institution have materials subsidiaries and associates which are engaged within the companies of insurance coverage, asset administration and housing finance, amongst many others. And the share costs of such banks derive vital worth from the efficiency of such entities. So, it requires a Sum of the Elements (SOTP) valuation of such banks, reasonably than valuing the banking enterprise in isolation.

In SOTP valuation, discrete values are arrived at for the standalone financial institution (based mostly on P/B) and every of the subsidiaries/associates (based mostly on related valuation metric for every enterprise); ultimately such values are added as much as get the general worth of the financial institution. In bl.portfolio dated August 25, 2024, we had carried the SOTP valuation of SBI, which illustrates how about 30 per cent of the financial institution’s share value might come from its key subsidiaries.

#learners #information #analysing #banking #shares