Ahluwalia Contracts (India) is one such main development participant with operations in numerous segments, unfold throughout 16 States, with a robust execution monitor report and an order guide cut up amongst assorted clientele — Central, State governments and personal sector firms.

Buyers with a 2-3-year perspective should purchase the inventory of the corporate in small portions at present ranges. At ₹810, Ahluwalia Contracts inventory trades at 24.5 occasions its trailing 12 months per share earnings and 20 occasions its doubtless per share earnings for FY24. This valuation a number of presents cheap consolation regardless of the share working up over 52 per cent within the final six months and about 20 per cent in simply the final couple of weeks since its Q2FY23 outcomes have been introduced. Any corrections within the inventory linked to the broader markets can be utilized to load up on the inventory.

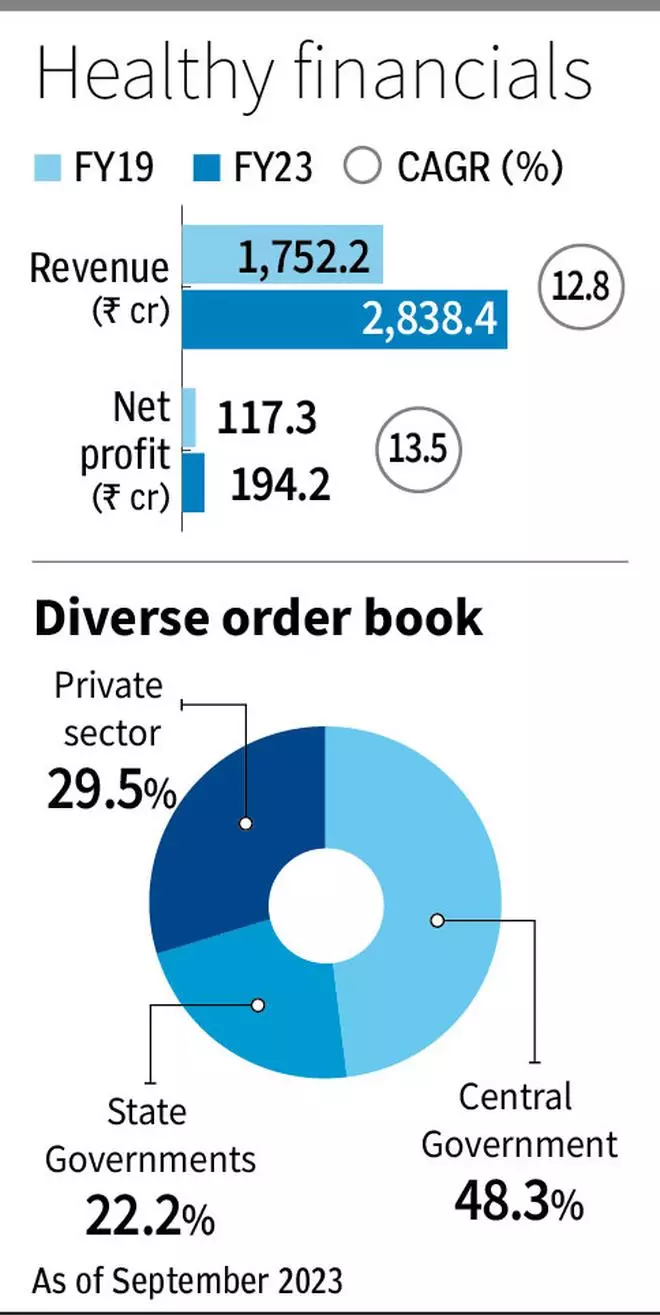

Within the first half of FY24, the corporate’s revenues have been up 35.1 per cent over the identical interval in FY23 to ₹1,665.2 crore, whereas internet earnings rose 36.5 per cent to ₹105 crore. Over FY19 to FY23 the corporate’s revenues grew at a compounded annual price of 13 per cent to ₹2,838.4 crore and the web earnings too expanded at 13 per cent to ₹194.2 crore.

The corporate’s return on capital employed has been in extra of 25 per cent for FY22 and FY23 and for a lot of the pre-Covid years as effectively.

Execution throughout numerous shopper base

As talked about earlier, Ahluwalia is into development. The corporate builds industrial and residential complexes, resorts, hospitals, schooling establishments, IT parks and automatic automobile parking tons. It is usually into redevelopment initiatives resembling these of railway and metro stations, depots and in addition builds city infrastructure. The corporate has been round for greater than 50 years and has a strong execution monitor report.

Ahluwalia Contracts is an EPC (engineering, procurement and development) participant and therefore bids for offers with an inexpensive margin profile and people which guarantee regular money flows.

A few of its marquee ongoing initiatives embrace redevelopment of Chhatrapati Shivaji Maharaj Terminus at Mumbai (₹2,450 crore), AIIMS Jammu, Bihar Animal Science College, Tata Memorial Centre, The Arbour Challenge for DLF, Max Tremendous Speciality Hospital and Dharavi Wastewater Remedy Facility, amongst others.

For many initiatives, the corporate payments its shoppers on a month-to-month foundation and in addition primarily based on milestones achieved. Often, because the work progresses in direction of completion, the margins from the entire undertaking begin to enhance for the corporate. It seems to be to keep up 11 per cent working margin. The corporate has ensured double-digit margins barring the Covid-19 disruption interval (2020-22), when lockdowns harm execution.

With uncooked materials costs stabilising, strong execution and talent to generate worth hikes ought to imply that margins stay wholesome over the foreseeable future.

Strong order guide

Ahluwalia Contracts has a big order guide, lending it a substantial income and execution runway. As of September 2023, the corporate has an order guide of over ₹12,000 crore, which is over 4x the revenues of FY23. Given the income progress price, there’s visibility for no less than the following 2-3 years. The corporate expects some slowdown in tenders within the subsequent few months as State and Common elections take centre stage. However the present pipeline is massive sufficient to maintain execution sturdy.

Over the previous 12 months or so, the corporate has been diversifying its order guide to absorb extra non-public shoppers on a selective foundation, principally in geographies the place it already has operations.

From an 82 :18 public to non-public sector order guide ratio final 12 months, Ahluwalia’ Contract’s guide is now at a 70:30 ratio and is seeking to transfer it in direction of a 60:40 ratio sooner or later.

The undertaking base can be numerous: infrastructure (29.7 per cent of order guide as of September 2023), hospitals (25.4 per cent), institutional (24.2), residential (12.4 per cent) and others (industrial and hotel-8.3 per cent).

Mounted worth contracts are coming down and during the last one 12 months the proportion has decreased from 30 per cent to 24 per cent, because it focuses most on common project-based ongoing billing.

Ahluwalia Contracts has money and financial institution balances totalling to ₹522 crore in its steadiness sheet as of September 2023 and has a debt of simply ₹32 crore.

#Ahluwalia #Contracts #Building #Participant #MustHave #Construct #Portfolio