Since our ‘Accumulate’ advice in bl.portfolio dated April 16, 2023, the inventory has gone up by 33 per cent and its trailing P/E has additionally expanded from 28 occasions to 35 occasions throughout the interval. With this, the valuation has moved up from its historic P/E vary of 25-30 occasions. Whereas the amount addition of minimal 30,000-40,000 tonnes can result in income rising at greater than 10 per cent CAGR, the EBITDA margin normalisation from present ranges of greater than 30 per cent to a sustainable stage of 20-22 per cent over the long run may not result in comparable development in EBITDA and PAT.

Thus, whereas enterprise prospects look good for the long run, to some extent that is countered by comparatively increased valuation and scope for margins to normalise at decrease stage in the long term.. For these causes, whereas present buyers can proceed to carry the inventory, contemporary positions needn’t be thought-about at this juncture.

Enterprise

AIA Engineering is the world’s second largest producer of HCMI (excessive chrome mill internals). Collectively referred to as mill internals, HCMI consists of excessive chrome grinding media (grinding balls), mill liners and diaphragms. Mill internals are primarily utilized in crushing and grinding operations of mining, cement and thermal energy technology industries. The grinding media balls are positioned in a grinding mill (a hole cylindrical shell) the place the supplies get crushed into an especially high quality type for his or her additional utilization.

Excessive chrome grinding media is the corporate’s core product. About two-thirds of the corporate’s complete gross sales is contributed by mining area (predominantly copper and gold) whereas the remainder comes primarily from cement and thermal energy. Whereas within the cement area, majority of the gamers at the moment are utilizing excessive chrome grinding media, the identical stands at solely 20 per cent in case of mining business, with the remainder utilizing standard cast grinding media. Within the Indian cement area, the corporate has 95 per cent market share whereas the identical is 35 per cent on the international stage (ex-China).

Although chrome-based grinding media value increased than cast ones, by 20-40 per cent relying on the chrome content material, that is compensated by put on, corrosion and abrasion resistance, elevated throughput, decrease energy consumption and chance of excessive stage of customisation.

Scrap steel and ferro chrome are the uncooked supplies used for the method. The corporate has a value escalation clause in its contracts, which permits it to cross on the prices to its prospects with a lag of about one to 2 quarters.

At present the corporate earns 75-80 per cent of its revenues by way of exports and the remainder from promoting its merchandise in India. The US (12 per cent) and Australia (10 per cent) have been main markets for it, aside from India. The corporate provides merchandise within the worldwide markets (about 120 international locations) by way of its wholly-owned subsidiary Vega Industries. Its shoppers embody giant mining and cement firms equivalent to BHP Billiton, Rio Tinto, Vale, Barrick Gold, Holcim-Lafarge, and Heidelberg Cement. Greater portion of revenue outdoors India exposes the corporate to foreign exchange fluctuation which it makes an attempt to hedge by means of derivatives.

Efficiency

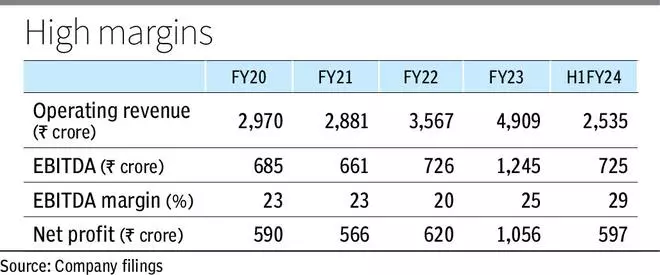

Throughout H1FY24, the corporate reported manufacturing quantity according to H1FY23 at 1,48,744 tonnes and registered a YoY development of 4 per cent in gross sales quantity, delivering 1,51,771 tonnes. Whereas mining volumes noticed a development of 5.5 per cent, the identical for non-mining phase remained flat. Beforehand, the administration guided for quantity addition of 30,000 tonnes throughout FY24, which it has diminished to 10,000-15,000 tonnes on account of given slower tempo of latest buyer conversion. Nonetheless, administration expects the annual gross sales quantity addition of a minimal 30,000-40,000 tonnes. by the top of FY25.

The corporate reported YoY working income development of round 5 per cent to ₹2,534.38 crore in H1FY24. Additional, its EBITDA elevated by 38 per cent at ₹725 crore and margins expanded from 25 per cent to 29 per cent, pushed by beneficial product combine and decrease uncooked materials and freight value. As per the administration, EBITDA margins can normalise to 20-22 per cent on a sustainable long-term foundation.

During the last 10 years, throughout FY2013-23, the corporate has been in a position to develop its revenues at a CAGR of round 11 per cent with consistency in EBITDA margins ranging at 22-28 per cent. This reveals its skill to cross on its uncooked materials costs to its prospects. Additional, with development in volumes, the corporate is anticipated to extend its income at the same CAGR within the close to time period.

It has a powerful stability sheet with web money of round ₹3,135 crore, which permits it to incur capex with out exterior borrowings.

Outlook

AIA Engineering has a dominant place within the chrome grinding media area after Magotteaux with gross sales volumes of round 2,91,000 tonnes (FY23). As presently, solely 20-25 per cent of the grinding mill inner area is roofed by the chrome grinding internals in mining business, there may be an addressable market alternative of 2-2.5 million tonnes of conversion, which gives vital headroom for development.

To capitalise on conversion, the corporate has deliberate to incur a complete capex of ₹500 crore until FY25 of which ₹300 crore will likely be executed in FY24. With 80,000 tonnes capability enhancement mission on Kerala JIDC plant and debottlenecking sure crops, which might add 15,000-20,000 tonnes of capability, the corporate goals at increasing its manufacturing capability from the present ranges of 4,40,000 tonnes to five,40,000 tonnes by the top of FY25.

#AIA #Engineering #Traders #Maintain #Inventory