Traditionally, PSU shares, whether or not within the defence, engineering or energy sectors, have traded beneath ebook values and to that extent PSBs are not any exception. However do they make for worth traps or worth picks? Which of them must you add to your procuring cart?

Why PSBs are a draw

PSBs have been within the ‘keep away from’ zone for a number of years.

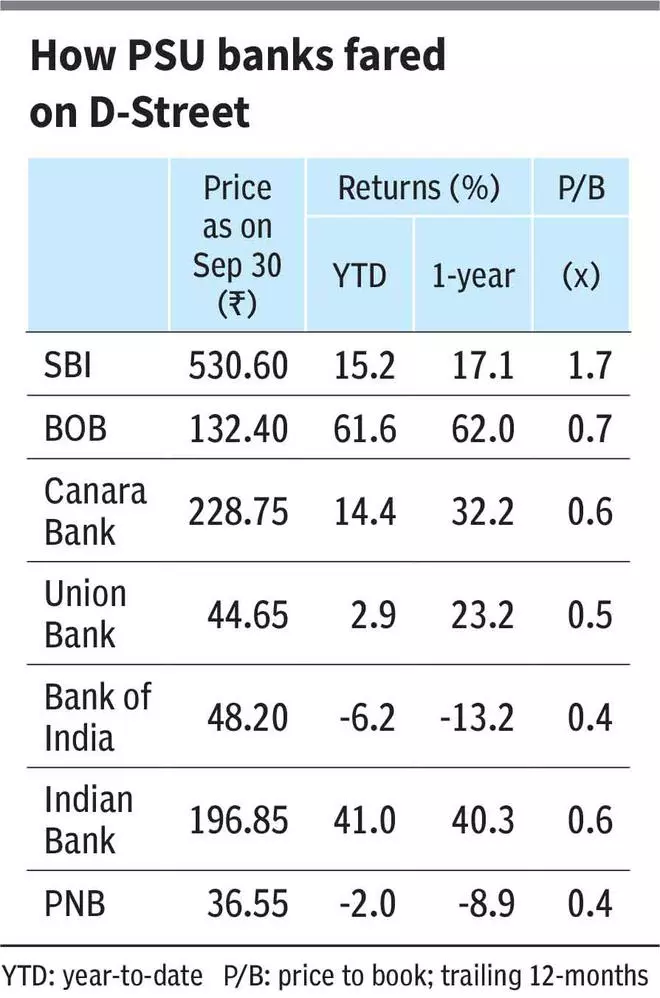

State Financial institution of India (SBI) was the primary to (re)seize investor consideration in 2018, when it demonstrated that it might efficiently take in its subsidiaries and but present indicators of turnaround in its asset high quality. Vijaya and Dena Financial institution have been folded into Financial institution of Baroda (BOB) that yr and this was adopted by the mega-merger that noticed 10 banks folding into 4. For BOB, the benefits of the merger began reflecting solely by mid-FY20 whereas for Punjab Nationwide Financial institution (PNB), Union Financial institution, Canara Financial institution and Indian Financial institution, outcomes grew to become seen in FY21.

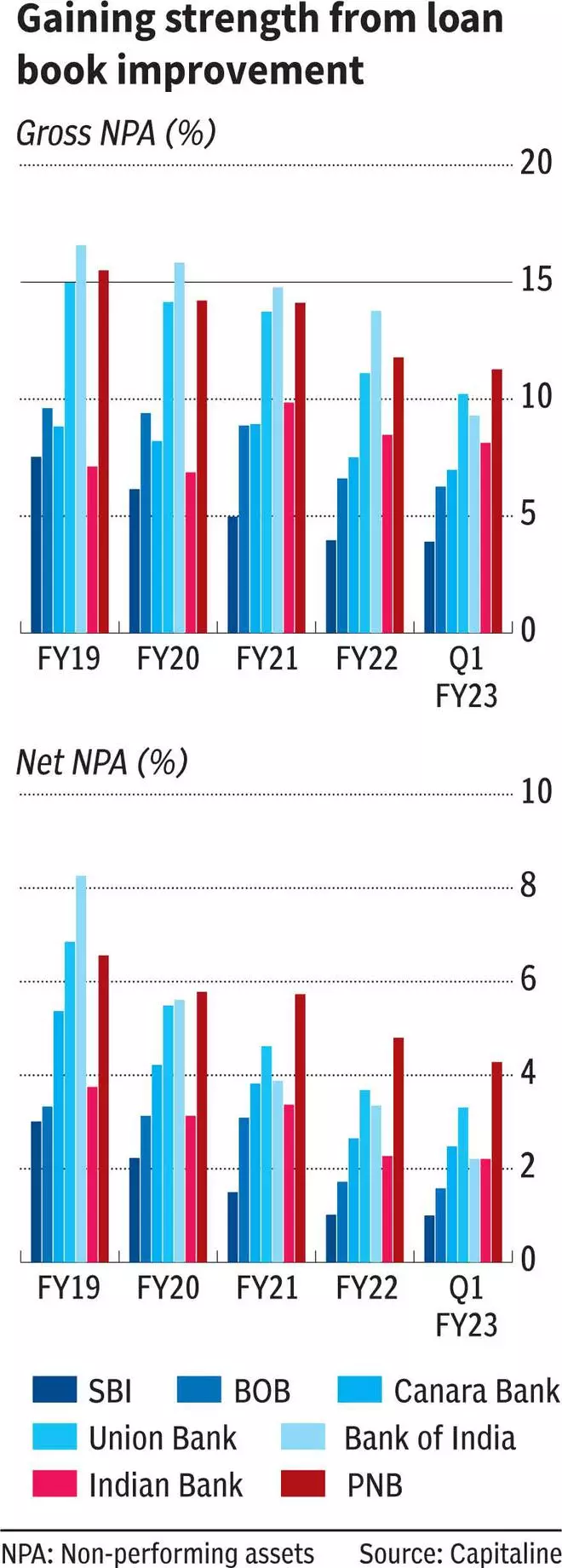

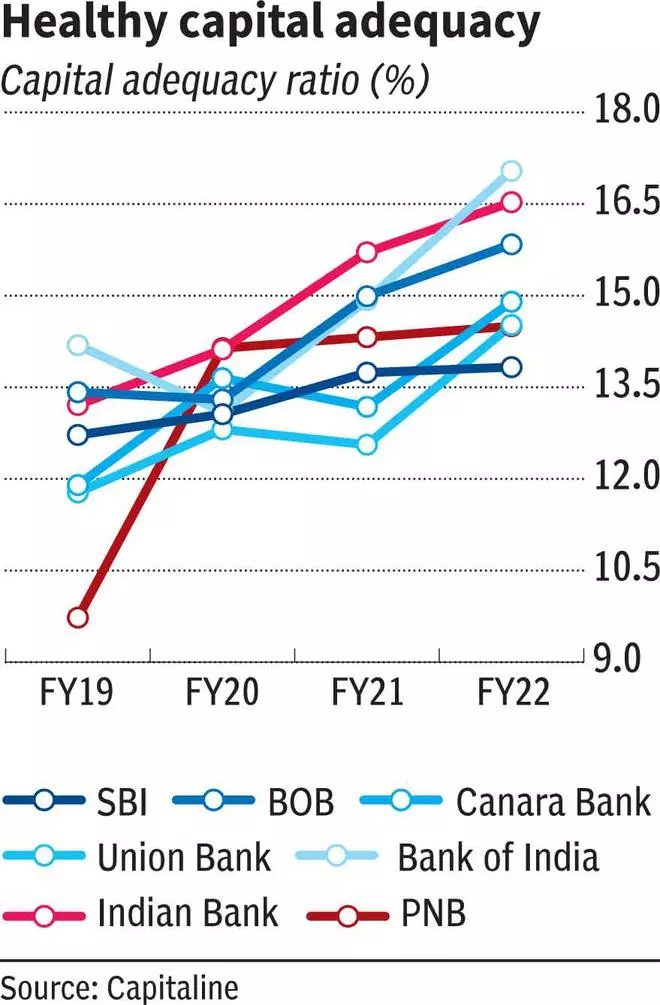

The merger has helped these banks in 3 ways. First, with the difficulty of fragmentation addressed, banks that led the merger moved up the league desk considerably. Second, the scale acquired by way of the consolidation helped them climate the pandemic at the same time as they have been redoing their processes and operations. Lastly, it boosted their capital adequacy, and opposite to the favored notion, their asset high quality is at an 8-year finest, in tandem with the general tendencies (see desk).

However don’t get enticed simply but.

When analysed by way of the three broad parameters — profitability, underwriting strengths and market share — right now, not all could move the litmus check.

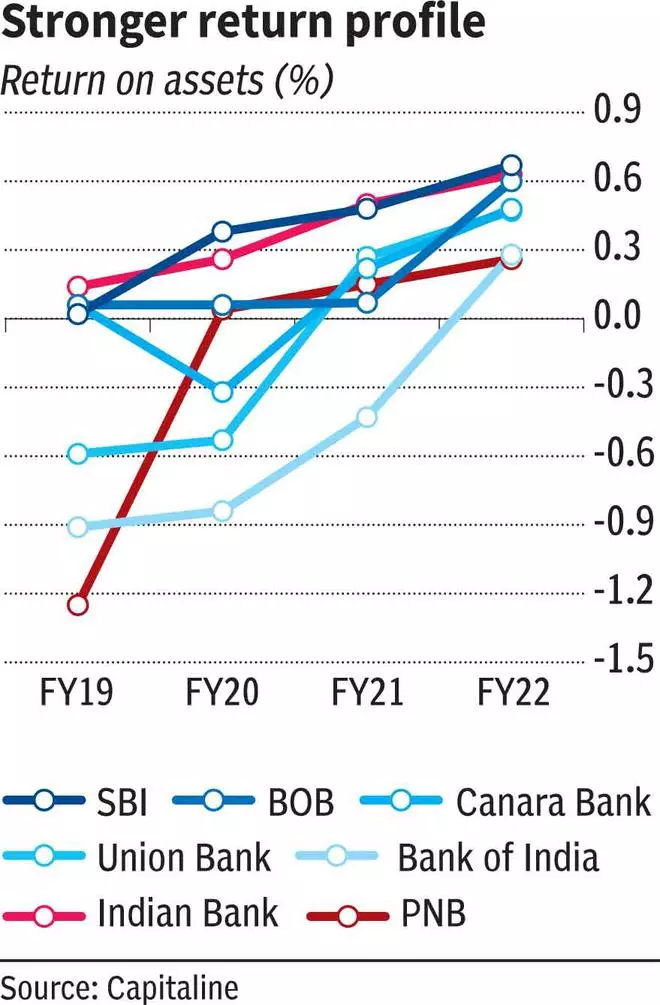

Profitability

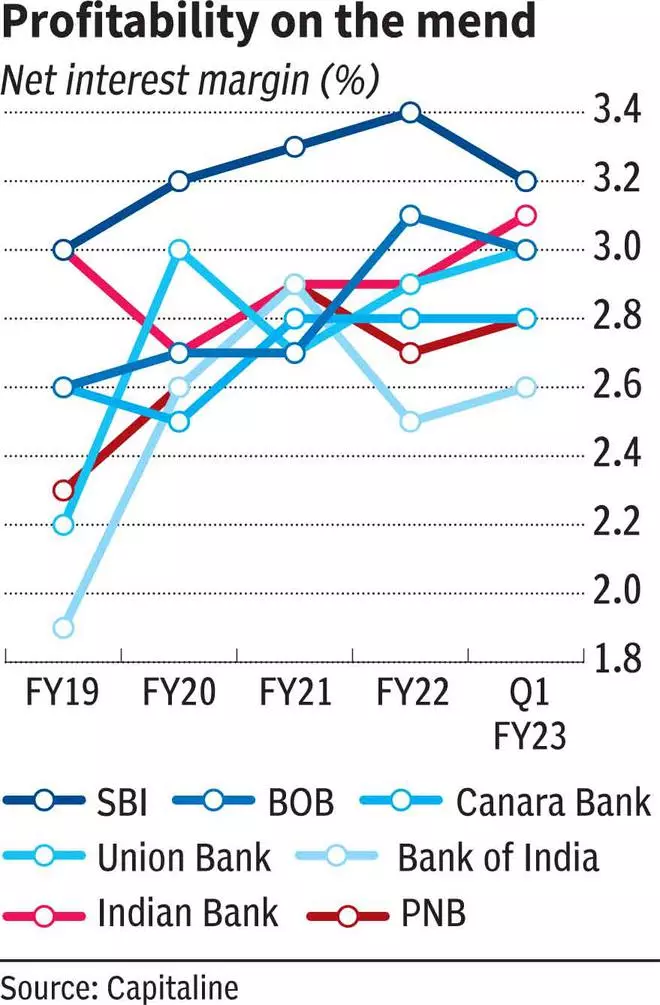

There’s a extensive hole between personal banks and PSBs by way of web curiosity margin, which is a measure of profitability. Whereas personal banks common at 4 per cent plus NIM, the typical of PSBs was three per cent in June quarter of FY23 (Q1). SBI is a transparent outlier, adopted by BOB, Union Financial institution and Indian Financial institution. Given PSBs’ mortgage ebook assemble, value constructions and their general yields being at a drawback to their personal friends, bridging the hole is nearly unlikely.

What must be seen in an rising rate of interest situation is whether or not they can preserve the NIMs at present ranges. Regardless of value of deposits not transferring up considerably thus far, yield on advances got here below strain by 10–40 foundation factors for PSBs in Q1 FY23. Consequently, in comparison with FY22’s NIM, profitability was below stress in Q1 itself. Due to this fact, whereas the general development of earnings enchancment could effectively proceed, as PSBs have the buffer to soak up asset high quality points, a qualitative enchancment in earnings is unlikely.

What’s extra, hardening bond yields impacted banks and extra so the PSBs in Q1. Whereas a number of the giant gamers corresponding to SBI have adopted a brand new technique for his or her funding ebook to minimise the influence of marked to market losses, with repo charges getting repriced upwards, this headwind, and drag on general earnings, can’t be prevented.

Threat administration practices

One of many key the explanation why PSBs commerce at a large low cost to their personal friends is the inherent weak point of their threat administration or underwriting requirements. High quality of the board, governance requirements, threat evaluation instruments and, extra importantly, the visibility and continuance of management groups have traditionally been notches beneath their personal friends. Empirically, we do not need a lot proof to display that PSBs have seen an enchancment on these parameters.

For example, the Monetary Stability Report of the RBI dated June 2022 factors out that PSBs have the next publicity to below-prime clients (56.2 per cent as of March 2022) in comparison with personal banks’ common at 32.9 per cent. Likewise, their publicity to super-prime and prime-plus clients stood at 16.2 per cent as in opposition to personal banks’ common of 31.5 per cent throughout this era. Clearly, if retail delinquencies witness a surge — which has been the development, extrapolating previous experiences — in an rising rate of interest situation, PSBs are extra weak to asset high quality shocks.

However what wants monitoring is the recent lending to corporates, which is about to select up within the coming months. PSBs have been decreasing the share of company loans of their stability sheets. The current inventory of those loans is totally offered for and is nearabout clear by way of asset high quality. Within the subsequent 12–18 months, the business expects demand from company India, together with State-owned infrastructure corporations, to select up. However does that insulate the system from one other scenario like FY10–FY13 when loans have been sanctioned with out sufficient cowl? The doubt lingers.

What gives solace is the tightening of regulatory necessities, corresponding to capping the group publicity, NPA recognition norms, and so forth. Likewise, the federal government, notably on highway and different infra initiatives, has finetuned the suitable of method norms which, to some extent, would be sure that venture loans can’t be sanctioned with out the fundamental necessities, in contrast to within the earlier decade.

But, the proof of the pudding is within the consuming and if the subsequent leg of progress is anticipated to return from India Inc, traders have to be additional cautious with PSBs. It might be applicable to quiz the managements on how they’ve improved their threat administration practices within the quarterly earnings name earlier than taking the plunge on PSB shares, particularly the layer after SBI and BOB.

Market share

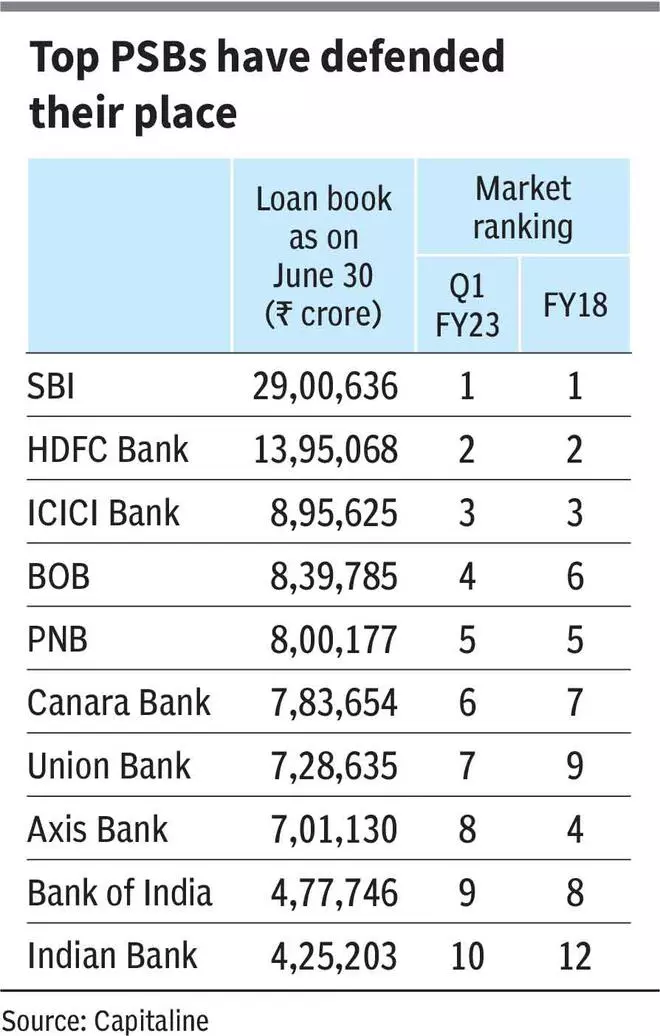

There may very well be some excellent news for PSBs on this facet. Whereas PSBs collectively have been shedding floor to their personal counterparts for over a decade, the stronger banks or the banks which have witnessed a wave of mergers corresponding to BOB, Canara Financial institution, Union Financial institution and Indian Financial institution, have moved up the rating (see desk).

Having touched ₹29-lakh crore of mortgage ebook in Q1, SBI has undisputedly retained its No 1 place within the banking system for a number of a long time. The one exception is PNB, which has maintained its No 5 place within the league desk regardless of the merger. Likewise, the one PSB among the many high 10 that has moved a notch down since FY18 is Financial institution of India. However Financial institution of India hasn’t participated within the consolidation course of thus far.

Due to this fact, whereas the lack of market share for PSBs is actual, it could be extra to do with the market base itself increasing considerably within the final decade and probably not their skill to maintain tempo with progress, particularly after 2019’s mega merger.

It is a optimistic takeaway for traders, the worry of putting a wager on a shrinking pie is dispelled.

Nonetheless, contemplating that PSB shares have witnessed a large rally within the final one yr, largely reacting to an enchancment in headline earnings numbers, it will be important for traders to concentrate to the primary two features talked about earlier — qualitative enchancment in earnings and profitability, and gauging the chance administration practices. At current, the conviction on these elements isn’t excessive.

Pecking order

With SBI representing a fourth of India’s mortgage excellent, it’s logical that traders betting on the economic system take a optimistic stance on SBI. For the primary time in over a long time the inventory is buying and selling effectively above its ebook worth, indicating the premium that traders are prepared to pay for a behemoth posting nearly a proportion of web NPAs.

BOB is the subsequent most well-liked PSB. Its skill to display management, develop a well-dispersed retail ebook and cut back its NPAs through the years is working in its favour.

Currently there may be elevated curiosity in Indian Financial institution, Canara Financial institution and UnionFinancial institution. Whereas the monetary efficiency of those banks has considerably improved within the final three years, Union Financial institution has a comparatively longer rope to climb by way of asset high quality. It might nonetheless be early to take a long-term view on these shares.

Curiously, continuously battling scams and fraud, regardless of its No. 5 place by way of mortgage ebook measurement, PNB hasn’t managed to return out of the ‘no-go’ zone for traders.

For the names beneath this league, corresponding to Central Financial institution of India, Financial institution of Maharashtra, Indian Abroad Financial institution and UCO Financial institution, the thrill is basically round additional consolidation and privatisation leading to inventory worth motion. Due to this fact, barring SBI and BOB, the remainder of the pack don’t qualify as excessive conviction bets.

They might find yourself being worth bets or worth traps — and solely time will inform.

#PSU #financial institution #shares #picks #traps