Additionally learn: Metal exports surge in February, however India nonetheless internet importer

Metal and vital metals resembling copper, aluminium and so on., hit document highs in early 2022 because the Russia-Ukraine struggle broke out, on worry of provide disruption that would hit the provision of commodities due to the battle.

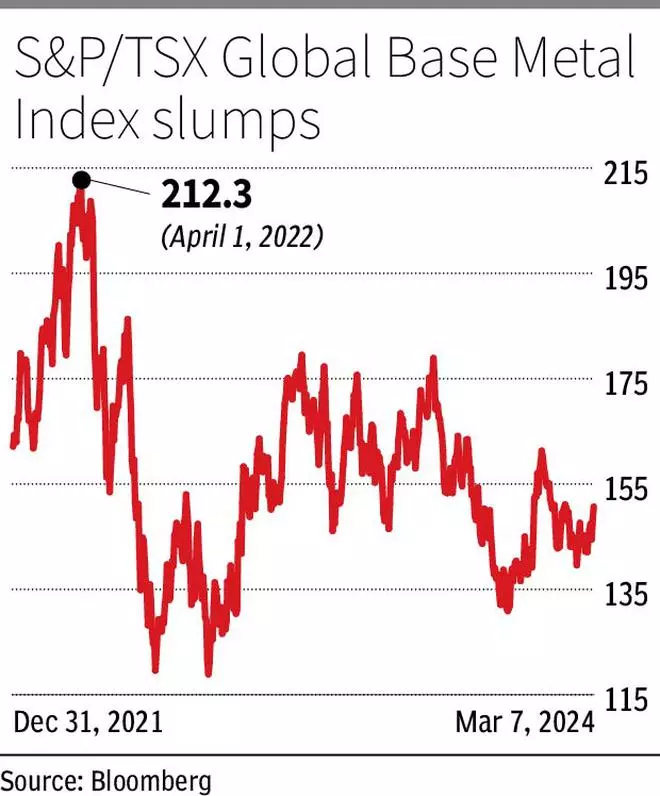

Nonetheless, costs have tumbled since then, resulting from weak demand and the speed hike cycle initiated by central banks, particularly the Fed. S&P/TSX World Base Metallic Index(150.7) is down about 30 per cent from its peak of 212.3 hit on April 1, 2022.

Decrease commodity costs helped India Inc with margin enlargement in the previous few quarters. What’s the outlook on the metals entrance for FY25? Right here, we have a look at the important thing components that would determine the worth trajectory of metals within the coming months.

The Chinese language angle

China’s share of steel consumption accounts for 60 per cent of the worldwide metals demand, in line with the World Financial institution. This signifies the significance of this nation within the commodity worth chain. So, the Chinese language demand is essential for value restoration.

The property sector in China, which has been on a downward spiral for the reason that breakout of the Evergrande disaster in 2021, continues to be ailing. Whilst the federal government is making makes an attempt to revive it by easing financing, cautious method by banks in the direction of lending to realty companies might drag the revival.

This aside, the large stock and the housing inventory beneath development might take years earlier than they’re cleared. In accordance with the Worldwide Financial Fund (IMF), housing begins have now dropped by 60 per cent in comparison with pre-pandemic ranges and actual property funding might drop by 50 per cent within the subsequent decade. Manufacturing too, is just not encouraging. A Manufacturing PMI (Buying Managers Index) degree of lower than 50 signifies contraction and it remained beneath that degree in China for 8 out of 12 months in 2023.

However, the decline in demand from the property sector was largely counter balanced by demand from renewable power and Electrical Autos (EVs) segments.

In 2023, China added 301 gigawatts of renewable power capability, which is sort of 60 per cent of the worldwide addition of 510 gigawatts for the 12 months. Throughout the inexperienced theme, the gross sales of EVs grew 38 per cent in 2023 and their share of complete gross sales reached over 30 per cent in December final 12 months. Thus, the demand for metals resembling copper, which have inexperienced purposes and aluminium, used extensively within the automotive sector, remained regular.

Nonetheless, going forward, these could not repeat. Whereas China might add between 200 and 260 gigawatts of inexperienced capability in 2024, it will nonetheless be decrease in comparison with 2023. Additionally, China has already reached its 1,200-gigawatt inexperienced capability goal for 2030 and so, the incremental additions will solely go down. However, the expansion charge in vehicle gross sales, which stood at practically 12 per cent final 12 months, might considerably gradual to three per cent this 12 months. Total, China, estimated to develop by 5.2 per cent in 2023, has set a decrease goal of 5 per cent for 2024. The IMF forecasts China to develop at a decrease charge of 4.6 per cent.

Additionally learn: Metal demand to decelerate subsequent fiscal: ICRA

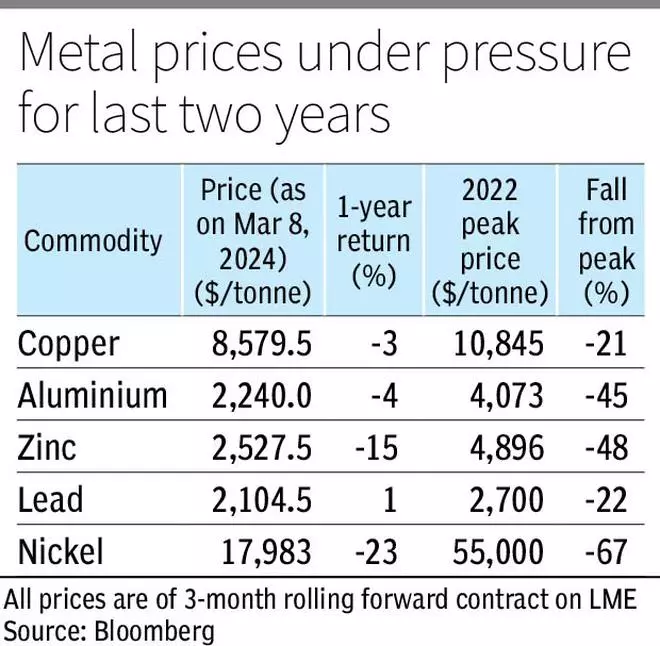

Although the demand from the inexperienced sector remained sturdy in 2023, the costs of key commodities resembling copper and aluminium rose solely 2 and 1 per cent respectively. Because the consumption slows within the coming months, costs are much less more likely to be supportive. That is very true, when provide is forecast to be in extra of the demand in 2024 for many of the metals.

Extra provide

For commodity gamers, what might be going to play spoilsport on metal and steel costs is relatively quicker progress in provide than demand.

In accordance with the World Metal Affiliation, the demand in 2024 is about to extend by 1.9 per cent to 1,849 million tonnes. Nonetheless, due to the overcapacity in China and absence of decarbonisation measures, the manufacturing might simply exceed the consumption, weighing on the metal value. In 2023, provide exceeded manufacturing by 77 million tonnes and the hole can go up additional.

The Worldwide Copper Research Group forecasts that the worldwide copper stability might shift from a 27,000 tonnes deficit in 2023 to 4,67,000 tonnes surplus in 2024. Whereas manufacturing outages in Chile, China and Indonesia supported costs to some extent in 2023, no main disruptions are anticipated in 2024. Mining output is predicted to develop in Chile, the Democratic Republic of Congo, Indonesia, Peru, Russia and Uzbekistan.

Likewise, the Worldwide Lead and Zinc Research group, expects international lead and zinc stability to be at a surplus of 52,000 tonnes and three,67,000 tonnes respectively. That is practically a 50 per cent improve in comparison with 2023. That is due to the rise in major lead manufacturing in nations resembling Australia, Canada, China, India and South Korea. For zinc, a powerful rebound in Chinese language manufacturing and enlargement of provide from giant initiatives within the Democratic Republic of Congo, Russia and South Africa may end up in manufacturing outpacing demand progress this 12 months.

With respect to aluminium, at the same time as China is nearing its self-imposed manufacturing cap of 45 million tonnes per 12 months, enlargement plans are on in different South-East Asian nations resembling Indonesia. Consequently, the provision will proceed to movement. Equally, for nickel, provide progress from Indonesia, which accounts for over 50 per cent of the worldwide provide, may end up in extra stockpiles of this steel.

Typically, subdued international financial exercise and easing of provide constraints are more likely to have a detrimental impact on costs in 2024.

Macroeconomics and geopolitics

World GDP progress, in line with IMF estimates, is more likely to keep flat at 3.1 per cent in 2024. However importantly, giant economies such because the US and China are anticipated to see appreciable slowdown. The previous might develop at 2.1 per cent this 12 months in contrast with 2.5 per cent final 12 months and the latter might gradual to 4.6 per cent in 2024 as towards 5.2 per cent in 2023.

Whereas the Euro space is predicted to see the next progress charge of 0.9 per cent in 2024 versus 0.5 per cent in 2023, larger rates of interest may very well be a dampener. So, the assist for commodity costs from this area may very well be restricted. Increased rates of interest within the US will also be a drag. Total, you will need to be aware that, as we now have mentioned earlier, the restoration in China is vital for commodities.

The upside dangers for the costs can come up from provide disruption resulting from causes resembling escalation of battle within the Center East and the Russia-Ukraine struggle. This aside, there are points on the traces of governments not allowing growth of latest mines resulting from environmental considerations and manufacturing outages resulting from energy or water constraint, and so on. Antagonistic developments on these fronts can push the costs up significantly.

That mentioned, at this juncture, the dangers are broadly tilted to the draw back due to potential weak financial exercise, notably in China and rising provide of metal and virtually all metals. A restoration in costs may be seen in 2025 resulting from potential enchancment in demand nevertheless it stays unsure. So, corporations in India with metal and base metals as key inputs are anticipated to get continued assist from the benign costs in FY25.

Technical evaluation

Extra provide is anticipated to exert downward stress on the costs. Broadly, the charts don’t present indications of a bullish turnaround at current.

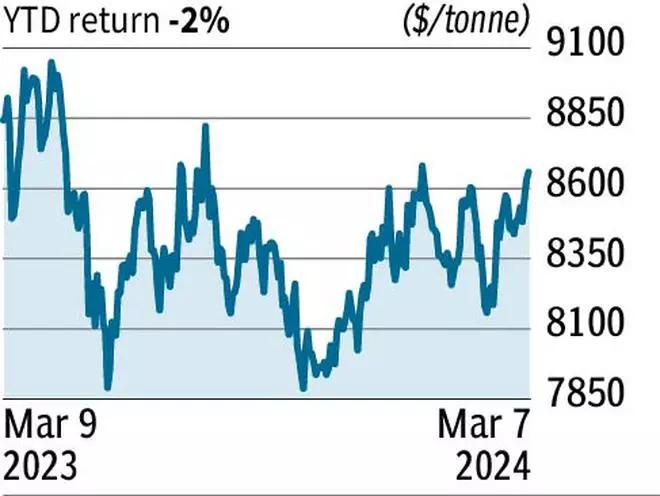

LME Copper ($8,579.5)

Copper futures on the London Metallic Trade (LME) has been oscillating between $7,900 and $8,700 since Could final 12 months. Resistance above $8,700 are at $9,000 and $9,400. However, assist beneath $7,900 might be noticed at $7,200. A break beneath $7,200 can set off one other spherical of sell-off, presumably dragging the contract to $6,500 after which to $5,800. Going forward, copper futures might fall to the worth area between $7,500 and $7,200 within the coming months after which set up a long-term uptrend. Observe that for the contract to show the development bullish, it ought to decisively invalidate the barrier at $9,400.

Help: $7,900 and $7,200

Resistance: $8,700 and $9,400

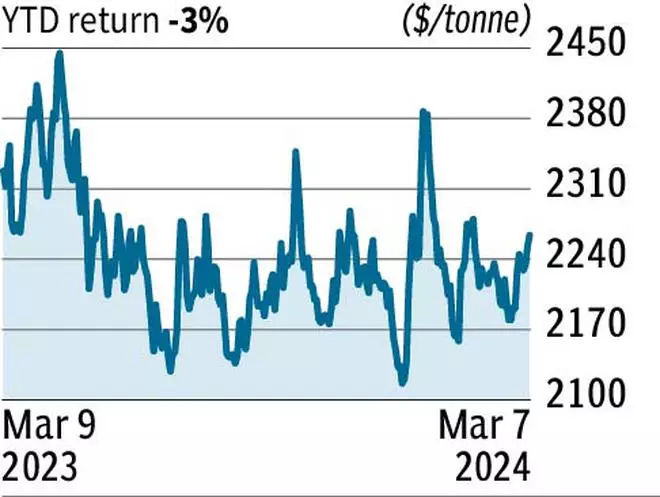

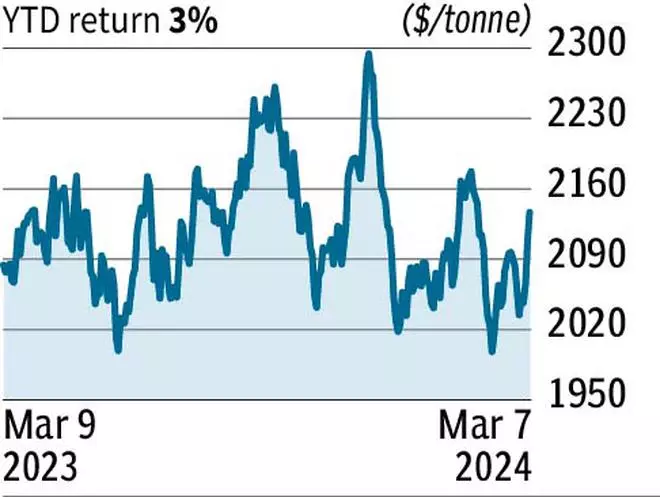

LME Aluminium ($2,240)

Aluminium futures on the LME has been charting a sideways development since Could, 2023. It has been fluctuating between $2,100 and $2,385. The chart exhibits no bias on both aspect and so, the possibilities for the consolidation to proceed are excessive. A breakout of $2,385 can raise the contract to $2,500 and $2,650. Observe that $2,650 is the essential degree and provided that aluminium futures surpass this degree, can it set up a sustainable rally. However, in case the contract slips beneath the sturdy base of $2,100, we’re more likely to see a fast fall to $1,950, a assist. Subsequent assist is at $1,830.

Help: $2,100 and $1,950

Resistance: $2,385 and $2,500

LME Lead ($2,104.5)

Lead futures on the LME, for the reason that starting of 2023, is shifting horizontally. It has been tracing a broader sideways vary of $2,000 and $2,300. Inside this value area, there’s a resistance at $2,170. However even earlier than 2023, lead futures haven’t been steadily trending in both path. So, we are able to anticipate the contract to behave that method within the coming months. We anticipate lead futures to remain within the $2,000-2,300 vary over the medium time period. Even when both of the boundaries of the vary is damaged, there are resistances and assist close by, which might hold motion restricted on both aspect.

Help: $2,000 and $1,915

Resistance: $2,170 and $2,300

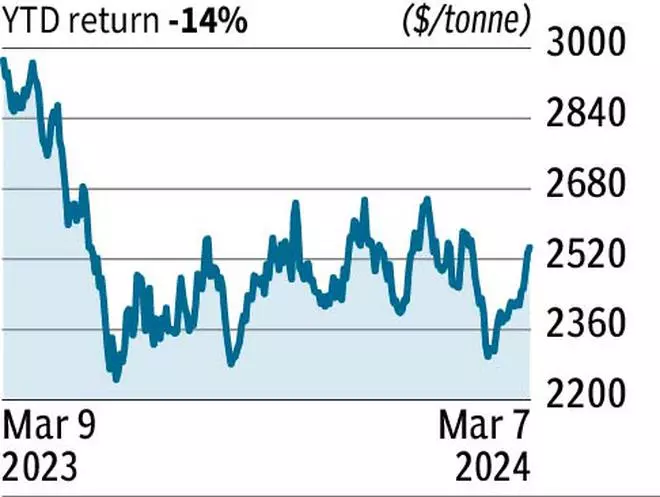

LME Zinc ($2,527.5)

Zinc futures, like the opposite base metals, has been in a sideways crawl. It has been oscillating between $2,270 and $2,650 since Could, 2023. Instantly above $2,650 is one other vital hurdle at $2,700. So, the worth band of $2,650-2,700 is a resistance band. If that is taken out, zinc futures can rally to $2,900. A breakout of $2,900 can result in the contract establishing a powerful upswing. However, if zinc futures decline from right here and drop beneath $2,270, it could fall to $2,040 and $1,800. If the downtrend to $1,800 occurs, we are able to anticipate zinc futures to see a major bullish reversal off this assist.

Help: $2,270 and $2,040

Resistance: $2,700 and $2,900

LME Nickel ($18,011)

Additionally learn: India to be again as internet exporter of metal by fiscal-end: Scindia

Nickel futures, which was caught between $15,900 and $17,200 since November 2023, noticed a contemporary breakout final month. So, there’s a likelihood for the contract to see additional upside. Nonetheless, the rally might be restricted as there are resistances at $18,500 and $20,300. If the bulls can push the worth above $20,300, then the long-term development can flip bullish. However because it stands, the chance for that to happen is low. The upswing may very well be a corrective rally and we’d see the worth falling after reaching both of the resistance. If the assist at $15,900 is breached, nickel futures can witness a fall to $14,280.

Help: $15,900 and $14,280

Resistance: $18,500 and $20,300

Observe: Charts of metal contracts present that the information is just not steady. Therefore, we’ve not thought of it for technical evaluation.

#Huge #Story #Whats #Retailer #Metal #Base #Metals