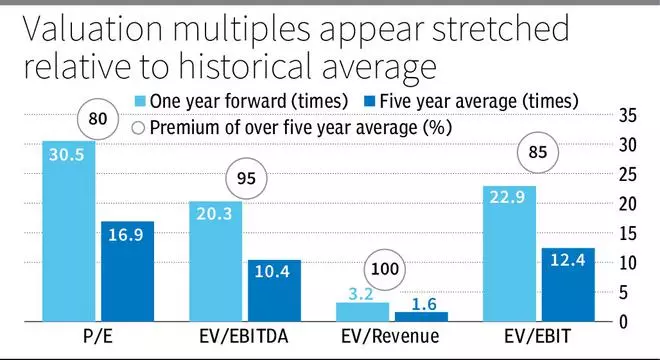

The inventory of Birlasoft is up practically 200 per cent from its lows of ₹250 in April this 12 months. The upside has been pushed by a mix of turnaround in enterprise, after margins had been hit in FY23 and EBITDA/web revenue declined 18/29 per cent. With FY24 efficiency thus far reflecting bettering working efficiency, the valuation of the inventory has re-rated from trailing PE of 21 instances in April to trailing PE of 55 instances now. Even factoring for the turnaround persevering with, the inventory now trades at a one-year ahead PE of 30.5 instances as towards 5 12 months common of 16.9 instances.

At present ranges, the risk-reward isn’t beneficial any extra for the next causes. For one, inventory is already reflecting prospects of improved efficiency and stable execution over the subsequent few years. Birlasoft, like many different corporations within the sector, was a beneficiary of the Covid-induced digitisation increase that resulted in multi-bagger returns within the small/mid-cap IT companies areas.

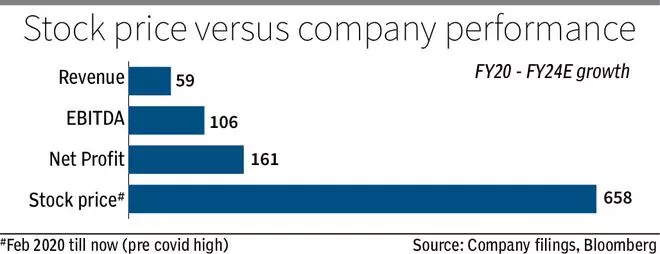

From a pre-Covid degree (February 2020) of round ₹95, Birlasoft is up 658 per cent. Throughout the identical time, its income, EBITDA and web earnings are up by 59, 106 and 161 per cent. This suggests market is already factoring excessive progress prospects over the subsequent few years. On this backdrop, there are just a few dangers that aren’t mirrored, leaving the inventory with low margin of security.

Though the corporate is actively seeking to diversify its geographic publicity, for now North America accounts for a big 85 per cent of income. Whereas the US has managed to shock with stable progress in 2023, the dangers of inflation and recession in 2024 stay as of now. Until there’s readability on this, high-valued IT companies shares are susceptible to important corrections if a recession materialises.

Therefore, we advocate that investorsbook earnings in Birlasoft and lock in on the sizable beneficial properties delivered this 12 months. This can be a valuation name.

Enterprise and up to date efficiency

As a well-established mid-tier IT companies firm, Birlasoft has sturdy presence throughout 4 verticals — Manufacturing (41 per cent of income), Life sciences (24 per cent), BFSI (21 per cent) and Vitality & Utilities (14 per cent). Its comparatively increased publicity to manufacturing and decrease publicity to BFSI is a differentiator versus many friends within the sector. Excessive-growth digital and cloud-related enterprise accounts for round 58 per cent of income (comparable with Tier 1 friends) — up from round 30 per cent in 2020.

After a powerful FY22, the corporate confronted delays in ramp-up of offers that impacted income and some execution points, together with increased hiring prices that impacted margins. This, mixed with broader cautious outlook for the whole sector, resulted within the inventory correcting from a peak of round ₹575 in January 2022 to ₹250 in April 2023.

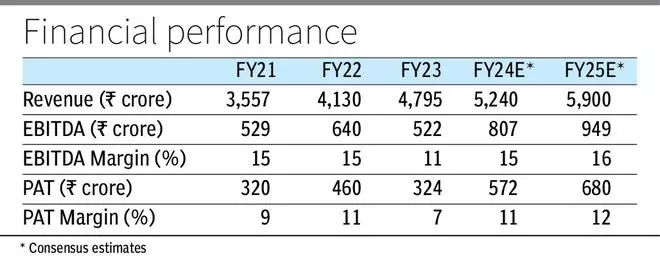

Nonetheless, the corporate’s efficiency has improved after the hiccups, with good restoration within the first two quarters of FY24. Within the lately concluded Q2, Birlasoft delivered income of ₹1,309 crore (up by 10 per cent Y-o-Y), EBITDA of ₹207 crore (up 17.5 per cent) and web revenue of ₹145 crore (up by 26 per cent). Fixed foreign money income progress was at 6.4 per cent.

These outcomes are good, particularly in comparison with the weaker efficiency of many top-tier IT corporations in FY24. Nonetheless, the inventory rally since April seems to issue greatest case state of affairs, which comes with dangers.

Consensus estimates now indicate a 12 per cent progress in income in FY25 and 18 per cent progress in earnings. This may require the present financial momentum within the US to maintain. Additional, the rupee has been flattish versus the greenback for the whole 12 months. If this continues, after some time it may begin impacting margins negatively for IT companies corporations. Mid-tier IT companies corporations with decrease EBITDA margin than top-tier gamers may be inclined to increased affect on web earnings when margins shrink (ie a 1 per cent decline in margins could have increased affect on an organization with decrease margins than one with increased).

As talked about above, this can be a name based mostly on valuation and dangers not factored. Not factoring the dangers is what resulted within the over 50 per cent draw-down within the inventory between January ‘22 and April ‘23. Present Buyers have to take cognizance of present dangers and may lock in on the beneficial properties.

Buyers who’ve remained on the sidelines thus far can anticipate higher entry factors sooner or later.

#Birlasoft #Buyers #E-book #Revenue #Inventory