Ambiguity on some proposals

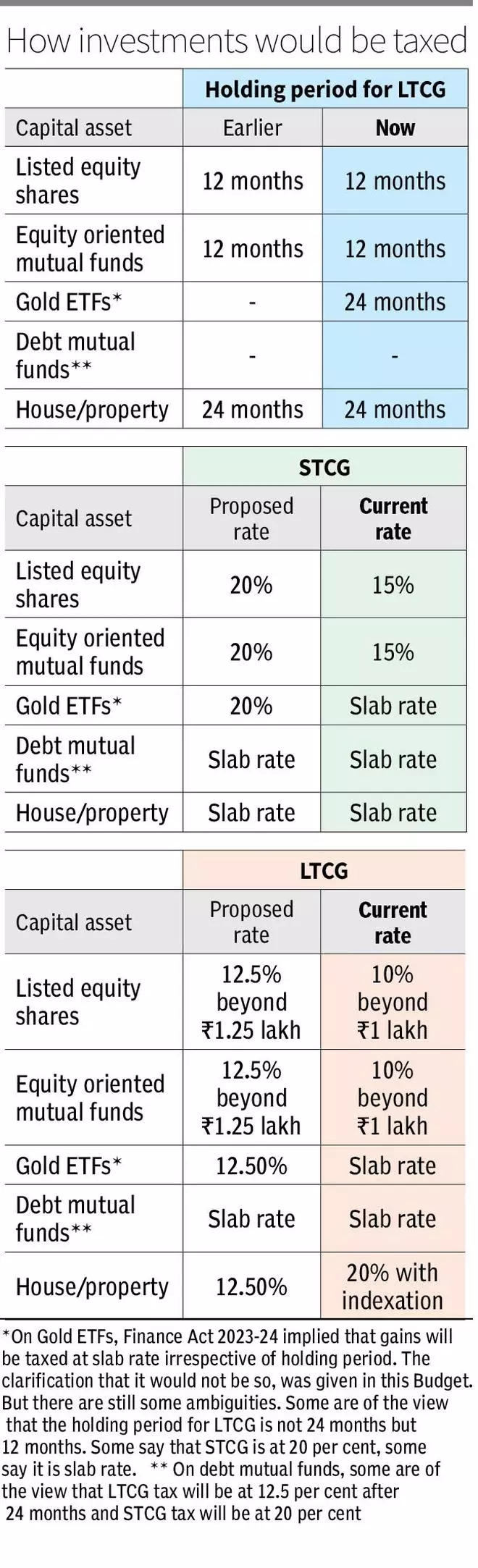

To brush up, earnings from listed shares and equity-oriented mutual funds will qualify for long-term capital beneficial properties if held for 12 months or extra, as earlier than. However tax in beneficial properties in extra of ₹1.25 lakh shall be 12.5 per cent, up from 10 per cent presently for beneficial properties greater than ₹1 lakh.

Within the case of all different asset lessons – property, gold (together with ETFs), bonds, debentures – long-term capital beneficial properties will kick in after a holding interval of 24 months. And LTCG tax shall be 12.5 per cent, down from 20 per cent with indexation advantages in some instances. On gold ETFs, one other view is that since they’re listed, capital beneficial properties made with greater than 12 months holding interval can be taxed at 12.5 per cent (see beneath).

With respect to debt funds – particularly after the clarification given on specified mutual funds – strictly going by the memorandum and Finance Invoice, no matter holding durations, all earnings are added to your earnings and taxed on the relevant slab. Nonetheless, some consultants imagine that long-term capital beneficial properties after 24 months shall be taxed at 12.5 per cent, whereas short-term earnings can be taxed at 20 per cent.

- Additionally learn: The ‘Idea of All the pieces’ in realty capital beneficial properties tax

Extra financial savings to think about tax change

Ideally, market-linked investments should be directed to particular objectives for higher product selections and higher focus.

Typical objectives for retail traders embody saving for youngsters’s schooling, their marriage, retirement, abroad travels and different such targets.

For instance, let’s say an investor deploys a lump-sum of ₹40 lakh over a interval of a few years, with the purpose of reaching a goal of ₹1 crore. With no tax, the earnings required can be ₹60 lakh. Nonetheless, with 10 per cent tax (and ₹1 lakh threshold), the quantity required on a post-tax foundation for reaching ₹100 lakh can be ₹107.66 lakh.

With the brand new Finances proposal that seeks to tax fairness beneficial properties at 12.5 per cent (and ₹1.25 lakh threshold), the investor would require ₹109.82 lakh pre-tax to make ₹100 lakh put up tax.

Within the above instance, the investor has to plan for ₹2.16 lakh extra to achieve the identical aim on account of larger taxes.

With bond funds, it turns into harder – Deposit curiosity of banks or NBFCs, coupons on bonds or debentures, and so on., change into absolutely taxable at your relevant slab charge. Capital beneficial properties would have 12.5 per cent tax on long-term earnings of debentures or bonds.

However investing in a debt fund may imply beneficial properties being taxed at your slab no matter holding durations. In fact, as talked about earlier, the taxation right here nonetheless wants full clarification.

Lowering shares or fairness funds publicity and growing the debt portion as an investor nears a aim is logical – say, promoting small-cap fund items and shopping for cash market schemes. If you pare equities, you’ll have to pay a capital beneficial properties tax. When the stability portion is parked in a debt fund, you might pay 30 per cent tax (assuming that slab charge) on the earnings made.

Planning for a brand new regime

Given all of the adjustments, some key facets of monetary planning change into much more essential now.

First, it is very important get your funding selections proper for probably the most half — whether or not they be mutual funds throughout classes, shares or gold funds. Taking the assistance of an funding adviser or distributor is essential for many who aren’t savvy and knowledgeable DIY traders.

Getting the alternatives improper and having to churn the portfolio ceaselessly may imply extra outflows on account of taxes and appreciable worth erosion.

Second, and the extra apparent half is to make sure you calculate your corpus necessities for particular objectives on a post-tax foundation after which plan investments accordingly.

In fact, tax charges could also be modified sooner or later as properly.

One technique to go concerning the process of planning for larger taxes is to issue that into your return expectations. Let’s say, you’re presently engaged on a long-term aim with an XIRR assumption of 13-14 per cent. You possibly can cut back the XIRR by a few share factors and rework the aim requirement.

One other technique to do it’s to imagine a excessive charge of taxation (say, 25-30 per cent) and add that to the whole corpus calculations.

Third, selections primarily based on the taxation of merchandise ought to not be the main target for traders, because it doesn’t assist attain supposed objectives. Now that charges and holding durations on asset lessons are rationalised, it’s all the extra important to be aim oriented.

Lastly, asset allocation – spreading investments throughout fairness, gold and debt – turns into essential with each churn you propose.

Tax tweaks on gold investments

Gold is taken into account a portfolio diversifer, being an inflation hedge and having unfavorable co-relation with equities over the long-term. Bodily gold together with jewelry, gold ETFs (exchnage traded funds) /funds, Sovereign Gold Bonds (SGBs) and digital gold are the modes by which traders take publicity to gold. The price range has tweaked taxation for traders within the yellow metallic.

For bodily gold corresponding to bars and cash and gold jewelry, LTCG (long-term capital acquire) tax has been introduced right down to 12.5 per cent from the sooner 20 per cent. Nonetheless, the indexation profit has been eliminated. However, the holding interval for LTCG is now 24 months in comparison with earlier 36 months. The STCG (short-term capital acquire) will proceed to be taxed at slab charge.

Gold funds and digital gold get the identical remedy of bodily gold. However traders ought to be aware that digital gold is unregulated.

That stated, some readability is required with respect to taxation of gold and silver ETFs (change traded funds).

In 2023, gold and silver ETFs have been categorised into specified mutual funds, main them to be taxed on the traders’ earnings tax slab, no matter the holding interval. As per the Finances, the LTCG tax on gold and silver ETFs is introduced right down to 12.5 per cent (with out indexation) from 20 per cent (with indexation).

However it’s unclear as as to whether the capital beneficial properties shall be thought of as LTCG above 12 months or 24 months. Some see ETFs to be listed securities and so, the LTCG shall be relevant for holdings greater than 12 months.

One other interpretation is that, LTCG will kick in solely after 24 months and shall be taxed at 12.5 per cent with out indexation and STCG shall be taxed at 20 per cent.

The brand new guidelines are efficient April 1, 2025. Due to this fact, for the present monetary 12 months, the present rule of taxing on the relevant charge shall be retained and traders can wait and look ahead to readability.

After all of the tweaking of taxes in different avenues, SGBs stay probably the most tax environment friendly instrument. In the event you maintain until maturity of eight years, the capital beneficial properties shall be absolutely exempt. Nonetheless, traders ought to keep in mind that as with all gold-linked instrument, the value danger exists even in SGBs.

#Finances #Fairness #Debt #Gold #Investments #Put up #Tax