- Additionally learn: Aptitude IPO: Pretty valued story

Even after that, the inventory at present trades at an inexpensive valuation of eight instances its FY24 estimated earnings. The corporate has a powerful stability sheet with money degree to the tune of round 20 per cent of its market cap, which allows it to ship good dividends to traders; the dividend yield is round 7.37 per cent at its present market worth. Therefore, we proceed to take care of a constructive view on the corporate and traders can accumulate the inventory on dips in view of affordable valuation, sturdy fundamentals and constructive business dynamics.

Enterprise

Coal India Ltd, conferred with Maharatna standing, is likely one of the largest coal producers on this planet. It’s primarily concerned within the manufacturing and sale of coal and generates most of its income from its coal operations.

As of now, the corporate has 318 working mines out of which 158 are open-cast, 141 are underground and 19 are blended mines. It produces majority of coal from the open-cast mines. It is because manufacturing from underground mines faces points reminiscent of longer gestation durations with lack of expert labour, unavailability of indigenous gear, and excessive departmental manufacturing value. Nevertheless, open-cast mines are extra impacted by rain than underground mines. The corporate majorly produces non-coking coal to be provided to thermal energy technology firms, moreover supplying coking coal to metal firms.

- Additionally learn: Fedbank Monetary Providers IPO: Promising franchise at an honest valuation

Majority of CIL’s income is tied to the long-term Gas Provide Agreements (FSA) whereby it sells annual contracted amount (ACQ) of coal at a notified worth based mostly on high quality that may be revised as and when required. Such association offers income visibility. If CIL just isn’t in a position to meet demand underneath FSA, it may well meet shortfall via importing coal and might provide it on a cost-plus foundation.

Additional, the corporate sells coal on spot foundation to these whose coal requirement is seasonal and who will not be keen to enter into long-term linkage. FSAs, being agreements for comparatively longer-term body, have fewer provisions for worth modifications. Alternatively, e-auctions are very a lot more likely to mirror the rising world costs, that are usually on the upper facet in comparison with FSA notified worth.

Efficiency

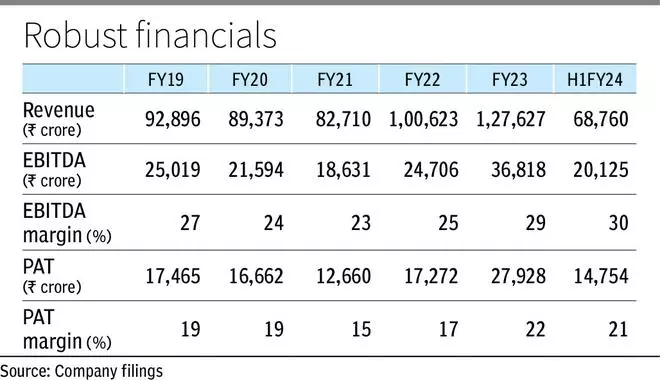

Throughout H1FY24, CIL achieved a YoY progress in manufacturing and offtake of 11.3 per cent and eight.6 per cent, taking it to 332.91 MT and 360.66 MT respectively. Of the entire offtake, practically 91 per cent got here from FSA and the remainder from e-auction as in opposition to round 73 per cent from FSA in final yr. Nevertheless, the administration guides for round 15 per cent of offtake via e-auction throughout H2FY24 — and for 16 per cent YoY progress in volumes throughout FY24 reaching 780 MT.

Additional, the corporate’s realisation throughout the interval slipped by round 4 per cent to 1,696.57 per tonne owing to 33 per cent fall in e-auction realisation, which was compensated by 17 per cent rise in FSA realisation. The rise in FSA realisation is pushed by latest worth hikes for the grades of coal comprising 30 per cent of its volumes.

Of late, there was some motion within the e-auction premium over FSA — it spiralled to round 137 per cent in April, 2023, dipped to 55 per cent in June, then moved increased to 78 per cent in August and has at present stabilised at round 90 per cent.

The corporate noticed round 6 per cent YoY rise in its working income throughout H1FY24 at ₹68,760 crore, pushed by enhance in volumes and compensated by lower in realisation. Its EBITDA and PAT throughout the interval have remained secure at round ₹20,125 crore and ₹14,754 crore respectively. CIL would possibly see a decline in profitability within the close to time period owing to normalising e-auction premium and better wage value. Nevertheless, this shall be supported by annual 5 per cent lower in manpower and the corporate’s plan to extend e-auction combine.

Outlook

CIL targets rising evacuation capability to fulfill quantity goal of round 780 MT, 850 MT and 1,000 MT by FY24, FY25 and FY26 respectively. Consequently, administration guides for an annual capex of ₹16,500–18,000 crore over the subsequent 5 years. These targets are approaching the again of administration’s anticipation of upper coal demand from the ability sector until 2030. Throughout H1FY24, capex to the tune of round ₹7,065 crore has been made whereas for FY24, ₹16,600 crore has been focused.

The capex additionally features a portion for growing first-mile connectivity initiatives (for clean transition from mine to pithead). An estimated complete capex of round ₹24,750 crore shall be made for these initiatives by FY29. Additional, the corporate has a plan to arrange 3,000 MW of photo voltaic within the subsequent 3-4 years. Out of three,000 MW, 250 MW of capability is deliberate to be put in by FY24.

#Coal #India #Accumulate #Inventory