Divi’s operates three segments. Generics (40 per cent of Q4FY24 revenues), nutraceuticals (8 per cent) and customized synthesis (51 per cent ). Generics section operates a number of large-volume APIs (round 20), that are absolutely backward-integrated and have 50-70 per cent of world market share. In customized synthesis (CS), Divi’s companions early to late stage builders in growing APIs for merchandise in medical trials and advantages from giant orders as soon as commercialised.

Progress avenues

Divi’s is more likely to increase its portfolio of generic APIs in its conventional method — backward built-in for low-cost high-volume management. It expects patent expiries within the subsequent three years to launch seven extra molecules. It has the requisite regulatory legwork (plant, product and trial paperwork) submitted. The corporate continues to increase market share in its current portfolio as effectively.

Within the CS section, Divi’s is now engaged on late-stage merchandise with greater probability of economic provides. Two new merchandise have been introduced in Q3FY24, which ought to ramp up within the 12 months. The corporate additionally introduced devoted capex for a product at a value of ₹650-700 crore anticipated to be commercialised by FY27, partnering an MNC. The corporate additionally talked about a surge in preliminary enquiries by clients, which ought to translate to business alternatives within the medium time period.

US and European innovators diversifying from China, usually known as China +1, received a regulatory enhance with the US Congress contemplating a Biosecure Act, which tries to limit partnerships with a number of companies in China. Though restricted to biotechnical collaboration whereas Divi’s is main in small molecules, the final route and firm previous commentary on greater curiosity appears to be aligned.

Divi’s has made headway within the small natural molecule house with GLP-1 merchandise, at the moment the main class in anti-diabetes with newfound utility in weight reduction. The corporate has developed three to 4 chain amino acids, that are key beginning supplies for GLP-1 class, and is anticipated to begin provides to innovators in FY25.

Together with GLP-1, FY25 can also be anticipated to witness ramp-up in distinction media merchandise. Three or 4 gamers management the section value $10 billion (on the innovator degree) break up equally between Iodine-based and Gadolinium-based merchandise. Divi’s has made headway in Iodine-based profile and expects to realize the identical within the different this fiscal.

Divi’s has a report of capex-driven progress and is once more within the midst of one other spherical. Section-1 of enlargement in Kakinada value ₹700 crore is anticipated to commercialise in FY25, which ought to assist each the segments. The Section-2 (₹800 crore) and the brand new devoted facility (₹650–700 crore) are anticipated to commercialise within the subsequent two years.

Headwinds

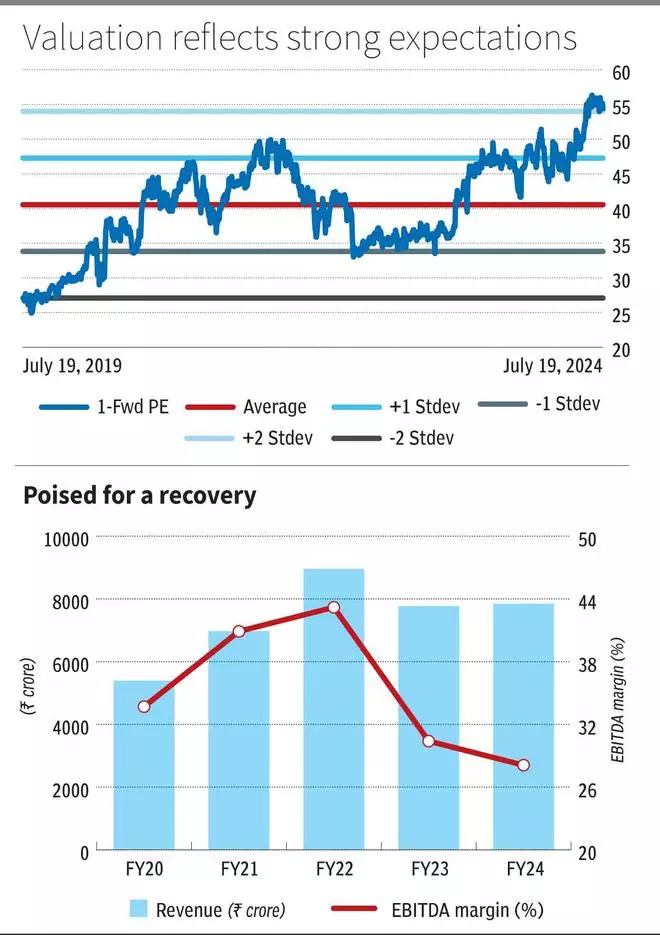

There’s pricing strain within the enterprise, which is obvious within the lowered margin vary of the corporate. In comparison with 40 per cent EBITDA margin vary in FY21-22, Divi’s reported 31 and 28 per cent within the final two years. At the moment, generic APIs are within the worth erosion cycle, which the corporate expects to have stabilised. The CS section can also be going through pricing downcycle as competitors emerges. The brand new segments will not be anticipated to considerably enhance past including 200-300 bps, which incorporates the generic pricing reversal and continued enchancment in uncooked materials prices. However the firm has reported 32 per cent margin in Q4FY24.

Valuations are at a premium to the upper vary that Divi’s normally trades at. In comparison with final five-year common of 40 occasions one-year ahead earnings, Divi’s is at the moment buying and selling at 55 occasions, which is nearer to 2 commonplace deviations above the imply. Whereas the outlook on progress is powerful, the excessive expectations should mood down earlier than one invests within the inventory. Consensus estimates count on 16/25 per cent income and EPS CAGR in FY24-26.

#Divis #Labs #Traders