For an anxiety-free life in your silver years, your retirement corpus should be capable of generate an earnings that may comfortably meet all of your bills, and even emergency wants.

Among the many many choices accessible, the one which comes with an assured stage of earnings all through your life is the quick annuity plan supplied by insurance coverage corporations. A right away annuity provides you an outlined pension for all times. Your partner, too, can obtain a pension for all times. The acquisition value (or the premium paid at first) could be returned to the partner or another nominee, because the case could also be.

Even the Nationwide Pension System (NPS) requires subscribers to annuitise (i.e., purchase an instantaneous annuity plan) to the tune of 40 per cent of the amassed corpus. Somehow, you will have to take care of quick annuity plans sooner or later near your retirement.

After mountaineering rates of interest by 250 foundation factors over the previous one 12 months, the Reserve Financial institution of India has hit the pause button. The overall consensus is that inflation has peaked, and rates of interest within the economic system could also be at or near their highs.

Annuities are additionally a operate of rates of interest and the yields have elevated with the rise in charges over the previous few quarters.

Some insurers provide pensions that evaluate favourably with the yields of long-term authorities securities as nicely.

Right here’s extra on how one can select the correct annuity product in your requirement to generate part of your post-retirement earnings. We talk about the yields, taxes and competing (or complementing) choices you could have, so that you just get the correct perspective earlier than parking your cash in quick annuities. .

The various pension choices accessible

A right away annuity product supplied by a life insurance coverage firm requires you to make a lumpsum fee upfront. That is the premium paid or the acquisition value of the product. This quantity is utilized by the insurer to offer you a daily pension stream until the top of your life.

There’s a GST part (1.8 per cent normally) added to your premium on the time of buy. This tax quantity will not be returned together with the acquisition value in any of the choices.

Ideally, it’s best to take an instantaneous annuity after turning 60 or from the time you retire.

There are a number of choices to decide on your annuity payout.

First is the pension for all times or single annuity with out the acquisition value being returned upon dying. So, if a subscriber takes such an choice, she would obtain a daily earnings until her life time and the coverage would stop after her time, with none return of the acquisition value.

This is able to go well with people who’re single or haven’t any surviving partner, and no different dependents to whom they would want to depart a legacy.

Then, there’s an choice to take annuity of life and still have the premium returned to your nominee after your time, i.e., annuity for all times with return of buy value. When you have a partner or a detailed dependent, you possibly can mark the particular person because the nominee. You too can mark the acquisition value for a charity organisation should you so want, by making the entity the nominee to obtain the proceeds after dying.

The third variant is the choice that enables you first to obtain the pension quantities and, afterward, after your time, provides your partner the identical pension quantity — joint annuity with or with out return of buy value. After your partner’s dying, the coverage ceases to exist with no additional funds made.

Each married couple would discover this feature helpful for his or her wants. After all, the acquisition value doesn’t get returned.

The fourth choice is much like the third, besides that the acquisition value is returned to the nominee after each the annuitants die.

Now, every of those choices needs to be rigorously weighed earlier than taking a call because the payouts range — fairly considerably at that — relying on the selection you make.

For instance, the only annuity with out return of buy value choice pays the very best pension quantity. However should you select the choice and if an unlucky occasion had been to occur to you early on in your retirement, a big corpus goes waste. And, attracted by the excessive yield, should you select the choice regardless of having a partner or dependent, the monetary crunch confronted by them could also be tougher.

Annuity is paid periodically — month-to-month, quarterly, half-yearly and yearly. The older you get, the upper are the payouts made by insurers. The utmost age of entry allowed is normally 80 years.

After you purchase an instantaneous annuity product, you can begin receiving pension funds from as early as the subsequent month after buy.

The speed of annuity payout varies relying on the choice you select. So, should you go for a single annuity for all times with out return of premium, you’d get the next payout than whenever you select to present again the premium paid to a partner or relative.

Yields from annuities enhance

The rate of interest hikes over 2022-23 have had a optimistic impression on quick annuity yields.

Now, earlier than moving into the precise yields on provide for subscribers, you will need to set the assumptions in place to take an knowledgeable name.

The age of the particular person shopping for the quick annuity or the primary annuitant is taken as 60. The pension is assumed to be acquired from the subsequent month after buy.

For all of the choices, ₹1 crore is assumed to be the premium or the acquisition value. With the GST added, the acquisition value turns into ₹1,01,80,000.

For all of the 4 choices, the primary annuitant or the principle policyholder is anticipated to reside until the age of 85. The partner is at the moment assumed to be 55 and can also be anticipated to have a life expectancy of 85 years.

The annual payout choice is taken into account for all selections as that ensures a bit extra by way of yield in comparison with different modes.

We now have taken the quick annuity plans supplied by insurers corresponding to HDFC Life, SBI Life, Kotak Life, ICICI Prudential, Bajaj Allianz and Tata AIA and IndiaFirst, to calculate the yields on provide.

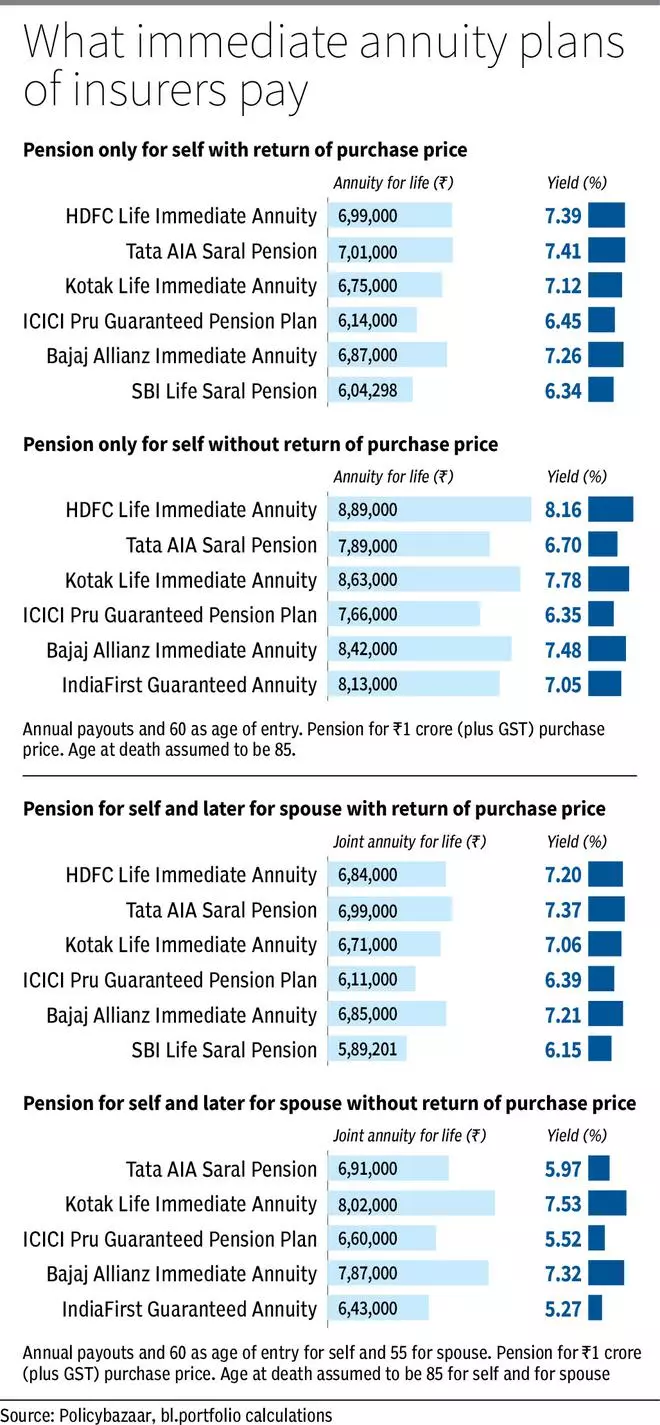

Single annuity with return of buy value: Knowledge from PolicyBazaar signifies that for the annuity for all times with return of buy to the nominee choice, these six insurance coverage corporations pay ₹6.04 lakh to ₹7.01 lakh on annual mode for a ₹1-crore coverage.

Based mostly on XIRR calculations, these payouts translate to annual yield of 6.34 per cent to 7.41 per cent. The quick annuities of HDFC Life, Tata AIA, Kotak Life and Bajaj Allianz provide 7.12-7.41 per cent yield.

For perspective, the yield on the 10-year g-secs is at 7.06 per cent. The 06.64 GS 2035, 08.30 GS 2042 and 07.17 GS 2050 commerce at 7.18 per cent, 7.27 per cent and seven.29 per cent respectively, in accordance with CCIL information as on June 22.

Due to this fact, the yields on provide are comparable with g-secs of longer maturity profiles, making them engaging.

Single annuity with out return of buy value: Insurance coverage corporations pay ₹7,66,000 to ₹8,89,000 for these taking this feature. Whereas the payouts are increased, you should weigh the choice rigorously as illustrated within the earlier part earlier than making a selection. The yields vary from 6.35 per cent to as excessive as 8.16 per cent. Greater pensions are paid beneath this feature because the premium will not be returned.

Right here once more, 4 insurers are providing greater than 7 per cent to subscribers.

Joint annuity with return of buy value: The yields from the choice given by insurers are within the 6.15 per cent to 7.37 per cent vary. Pensions supplied yearly are within the band of ₹589,201 to ₹699,000. Yields are decrease as there’s a pension to be paid to the second annuitant and the acquisition value additionally needs to be returned.

Joint annuity with out return of buy value: The payouts vary from ₹6,43,000 to ₹8,02,000 and the yields on provide are within the 5.27 per cent to 7.53 per cent vary.

If inflation is assumed to be at 6-7 per cent yearly, many of those insurance policies provide yields that beat the speed of value rise.

Buyers can contemplate HDFC Life Speedy Annuity, Bajaj Allianz Speedy Annuity, Tata AIA Saral Pension and Kotak Life Speedy Annuity in case they select the only or joint life annuity with return of premium choice. For a similar choices with out return of buy value, the quick annuity plans of Kotak Life, Bajaj Allianz and HDFC Life could be taken.

Taxes and competing choices

Within the case of quick annuities, the important thing optimistic issue to notice is that the quantity paid out is fastened and warranted for all times, no matter any change in rates of interest sooner or later. The truth that there’s certainty of cashflows as you might be locked into a selected fee is reassuring, particularly in your retirement years. And these are protected investments, with no threat of default in pensions.

As talked about earlier, rates of interest in India are near their peak. As with deposits, locking into annuities at comparatively increased yields can be helpful in the long term for earnings technology because the payout stays the identical even when charges decline.

If you’re single, with no dependents, you possibly can go for simply single annuity with out return of buy value and revel in a 20-25 per cent increased annual payout than you’d with return of buy value.

In case you might be married, you possibly can go for annuity with return of buy value. However should you doubt your partner’s potential to deal with a big sum after your time, you possibly can go for joint annuity for all times in order that your partner continues to obtain a pension.

One other key side to notice is that you should have a number of sources of earnings and never simply rely upon annuities alone. Annuities can maybe be used to generate 25-30 per cent of your post-retirement common bills.

Moreover, systematic withdrawal plans (SWPs) from debt or fairness funds (as per your threat urge for food), curiosity from financial institution and NBFC deposits, and small financial savings schemes corresponding to SCSS (Senior Residents’ Financial savings Scheme) should be a part of your post-retirement portfolio for normal earnings technology.

However with deposits and small financial savings schemes, the rates of interest are reset periodically by the federal government banks or non-banking finance corporations primarily based on prevailing rates of interest (although you lock into the speed for the time interval chosen beneath deposits and for 5 years beneath SCSS). Due to this fact, you face reinvestment threat during times when rates of interest are low. Your deposits would earn lower than inflation.

Taxation on annuities is like how it’s with common earnings. All payouts from quick annuities are added to your earnings and taxed on the slab relevant to you.

#Exploring #Annuity #Plans #Assured #Revenue #Retirees #Engaging #Yields