The India Shelter Dwelling Loans (ISHL) IPO, which is open from December 13–15, comes at a time when each Nifty and Nifty Financial institution are at a lifetime excessive. We listing 5 related issues concerning the residence finance difficulty. The NBFC is promoted by PE buyers WestBridge Crossover (20.3 per cent stake post-issue), Aravali Funding (26.6 per cent) and Anil Mehta (1.5 per cent). Different funding funds forming a part of the general public shareholding are taking part within the OFS, and are providing a portion of their stake within the IPO.

On the higher finish, ISHL might be valued at ₹5,278 crore, which is 3.8 instances price-to-book – according to its friends in residence finance (HFC) NBFCs. The IPO will elevate ₹800 crore in contemporary difficulty for lending actions and ₹400 crore in OFS.

Retail centered reasonably priced housing loans

ISHL primarily targets self-employed prospects from the low- and middle-income teams (86 per cent of September 23 AUM), residing in Tier-II and Tier-III cities in India. The common ticket measurement is round ₹10 lakh, and the common LTV (loan-to-value) round 50 per cent throughout the years.

Geographically, Rajasthan (31.3 of Sep-23 AUM), Maharashtra (17.5 per cent), and MP (13.9 per cent) are the biggest areas. Karnataka, Gujarat and UP every account for 6-7 per cent of the AUM, with a presence in different areas as properly.

Macro setting – cautiously supportive

Retail credit score development in India at 14 per cent CAGR in FY18-23 has outpaced general credit score development of 10 per cent within the interval. Crisil expects this larger tempo of development to proceed, particularly in underbanked rural markets that ISHL operates in. The agricultural economic system accounts for 47 per cent of GDP, and eight per cent of general credit score, based on the RHP. With last-mile funding capability and rising monetary inclusion metrics aided by connectivity and web, retail lending in rural markets ought to report excessive development.

However there are pockets of concern within the rural markets as properly, which have reported ‘jobless development’ since Covid. FMCG and auto gross sales have indicated an absence of quantity development within the rural phase within the final two years, supporting a weak job market view. The revised rates of interest have pushed up EMIs by 20-30 per cent, which might drive delinquencies available in the market as properly.

Quick rising mortgage e book with high quality enchancment

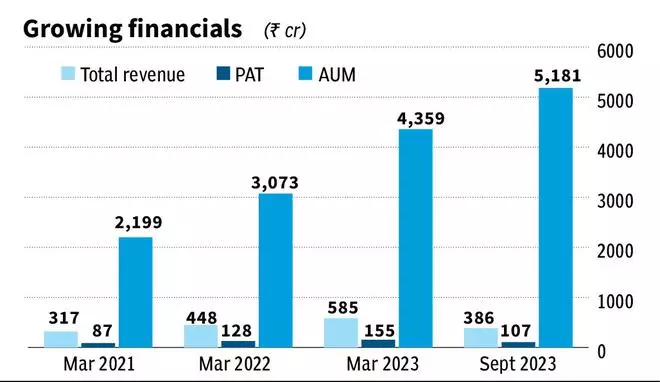

The NBFC registered 40 per cent AUM CAGR within the final 5 years, with an AUM base of greater than ₹5,180 crore by September 2023 (residence mortgage: mortgage towards property in ratio of 57:43). The asset high quality metrics have additionally improved, with Stage-3 belongings at 1 per cent of AUM in September 2023 (stage-3 belongings are NPAs that are due for greater than 90 days), from 2.8 per cent in September 2022. However loans that are 30 days late haven’t improved as a lot, accounting for 3.2 per cent in September this yr, in comparison with 4 per cent final yr. However with near 60 per cent of present AUM constructed solely within the final three years, the NBFC mortgage e book could not have weathered considerably.

ISHL sources its funds primarily from time period loans, accounting for 69 per cent of borrowings in September 2023, adopted by financing from Nationwide Housing Board at 17 per cent, and ECB at 7.6 per cent.

Excessive spreads on lending

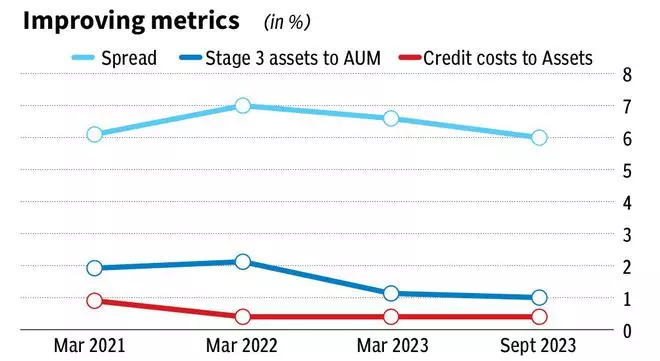

With its lending profile centered on the underbanked segments, ISHL secured a 6 per cent unfold in September 2023. This accounts for yields of 14.9 per cent (flat from final yr) on the belongings, web of borrowing prices, which elevated 60 bps YoY to eight.9 per cent. Publish-IPO, with an enchancment in credit standing from improved capital flows, ISHL could enhance its spreads as value of borrowing eases. With the US Fed outlining an exit roadmap for top rates of interest, each yields and borrowing prices could decline concurrently within the home markets as properly.

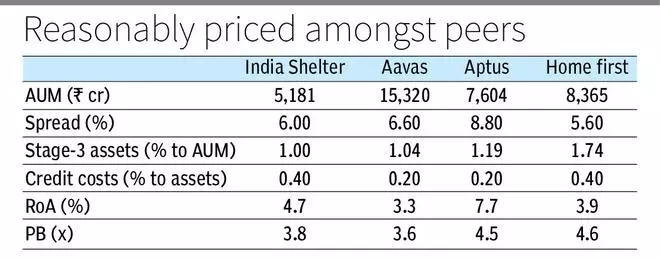

Peer comparability

On the higher vary of the IPO value band of ₹493, ISHL is priced at 3.8 instances price-to-book, which is on the decrease finish of the peer group vary of the three.5-4.6 instances for September. Inside small ticket housing financing firms, Aptus secures the best valuation at 4.5 instances, pushed by yields at 8.8 per cent and an inline NPA ratio of 1.2 per cent. Aavas, with the best mortgage e book of ₹15,000 crore, trades at 3.6 instances e book worth. The valuation vary could also be attributed to a excessive RoA of seven.7 per cent for Aptus, in comparison with 3.3 per cent for Aavas. ISHL with RoA at 4.7 per cent regardless of reasonable spreads, factors to the low influence of operational or credit score prices on return metrics.

#India #Shelter #Dwelling #Loans #IPO