The shares of GGL have rallied round 41 per cent within the final one 12 months and in addition reacted positively to the merger announcement. The corporate is richly valued at PE of 38.1 instances TTM earnings and is now buying and selling a 38 per cent premium to its five-year historic common of 27.7.It’s also costlyin comparison with its friends – Mahanagar Gasoline (PE of 14.8 instances) and Indraprastha Gasoline (21.6). Most positives — structural push from the GoI, synergies on merger and the falling crude costs, appear to be priced in publish this rally. Dividend yield, which is an added issue to put money into PSU shares can be not engaging any extra at 0.9 per cent. With volatility and cyclicality being an inherent a part of the enterprise and the identical being enhanced with the possible merger of exploration and manufacturing (E&P) phase of GSPC into GGL, buyers can think about reserving earnings and locking in on the features. It is a valuation name. One other issue to notice is that, given the merger swap ratio favours GSPL at present costs, GGL could also be a relative underperformer.

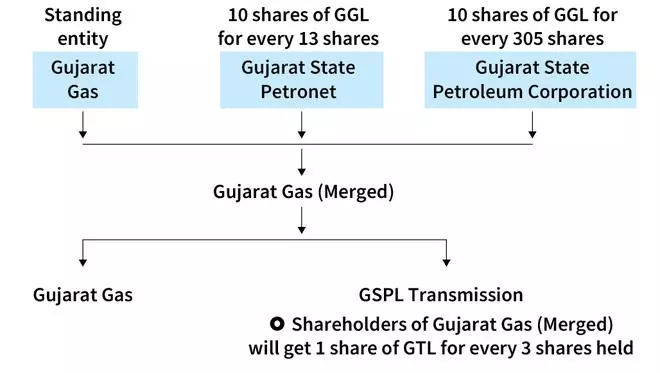

Scheme of association

The scheme proposes to merge GSPL, Gujarat State Petroleum (together with its wholly-owned subsidiary GSPC Power) — with GGL. Share-swap ratio is as defined within the illustration. Submit-merger, gasoline transmission and associated investments can be carved out right into a separate entity – GSPL Transmission Ltd (GTL). Whereas investments pertaining to transmission enterprise alone can be carved out, all different investments will stay with the built-in GGL. This scheme of association is proposed to be wrapped up by August 2025, topic to approval of shareholders and all related authorities and regulatory our bodies.

This association, amongst different issues, disentangles the possession construction. As painted by the administration, the merger is geared toward enhancing the working efficiencies boosted by merger synergies. Presently, gasoline is traded from Gujarat State Petroleum to GGL, and will get distributed to the end-customer (B2B2C). Submit merger, by changing into an built-in entity, this can be simplified by immediately promoting to the end-user (B2C).

There are extra tangible advantages from this merger: One, the purpose of taxation for oblique tax can be one entity (built-in). Two, accrued losses within the books of Gujarat State Petroleum to the tune of ₹7,200 crore might be utilised to set off future earnings of the resultant entity, roughly over the subsequent two years.

Enterprise

GGL is a metropolis gasoline distribution (CGD) participant with distinguished presence in Gujarat alongside some presence in 5 different States. The corporate is the biggest CGD participant in India when it comes to quantity and in addition operates round 810-plus CNG (compressed pure gasoline) stations throughout the above areas. Enterprise includes sustaining and working the gasoline distribution community and including new connections (prospects), whereas monetising the gasoline distribution — including a mark-up on the price of gasoline distributed. Based mostly on the end-use, the corporate has 4 segments – CNG (27.1 per cent of income), PNG (Piped Pure Gasoline) – Industrial (66 per cent), PNG-Home (5.7 per cent) and PNG-Business (1.2 per cent).

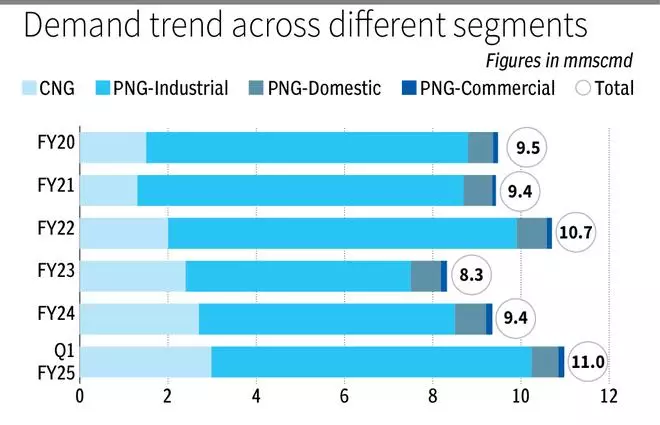

Volumes surged for GGL in Q1 FY25, primarily on the again of Morbi-led demand restoration from the commercial phase, enhancing from 9.4 mmscmd (million metric commonplace cubic metre per day) in FY24 to round 11 mmscmd in Q1 FY25. Nevertheless, the administration has guided for softer volumes in Q2 owing to container shortages, which is predicted to negatively hit companies in Morbi and subsequently, gasoline consumption.

Morbi, a metropolis in Gujarat, popularly generally known as the Ceramic Capital of India, accounts for round two-thirds of GGL’s provide of PNG for industrial use circumstances. Morbi is predominantly provided with imported pure gasoline, which is comparatively costly, as home pure gasoline underneath the cheaper administered worth mechanism (APM) route is earmarked to satisfy the demand from PNG-Home and CNG segments. Anyhike in LNG costs negatively impacts the commercial demand, with LPG being a less expensive alternate supply, as has been noticed previously (refer illustration). Switching from PNG to propane is usually noticed when Gasoline – Propane worth premium is larger than ₹1-2/scm. Thus, the impression of the current fee hike train by GGL within the Morbi area, is a key monitorable for Q2.

Demand for CNG, though a fraction of commercial PNG volumes, has improved steadily since FY20. Nevertheless, long-term threat exists, as EVs acquire share within the mobility house. Alternatively, PNG for business and home use has comparatively stayed flat since FY20.

Working metrics

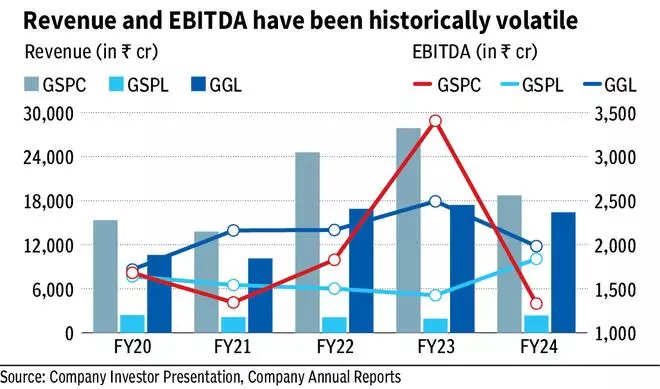

Income and EBITDA grew at 11.5 per cent and three.7 per cent CAGR respectively for GGL since FY20, whereas the numbers had been risky for Gujarat State Pertroleum and GSPL, as noticed within the desk above. The numbers pertaining to Gujarat Power usually are not materials in relation to total dimension of the merged entity.

Presently, the contracts on the availability aspect, predominantly managed by Gujarat State Petroleum (which then sells to GGL), are within the ratio of 60:40, long-term and short-term respectively. Lengthy-term contracts are linked to crude costs, whereas short-term contracts are largely primarily based on spot-LNG costs. GGL additionally has round 25 per cent spot-dependence. Thus, even publish the scheme of association, the volatility on account of spot-dependence will proceed.

Outlook

Although the present situation of descending and deflated costs of crude is the most effective the sector may ask for, the enterprise is essentially cyclical in nature, and therefore the present valuation seems costly.

One other vital issue to notice is that per the scheme of association, buyers will get 10 shares of GGL for 13 shares of GSPL. Assuming the merger will undergo, GGL is buying and selling at 15 per cent premium to worth of GSPL primarily based on share-swap ratio. This will additionally end in some relative underperformance in GGL, as new buyers could select to purchase GSPL over GGL.

Why

GGL may underperform GSPL at present swap ratio

Enterprise may stay risky

#Gujarat #Gasoline #Scheme #Association #Add #Fizz #Counter