Why so?

There may be sturdy coverage assist from the federal government for the sector, the push for indigenisation has by no means been higher, and order books for Indian defence firms are so sturdy. So what’s the case for a retreat, when the Indian defence story is so good? A comparability with international defence shares lays naked the information.

- Learn:NSE launches Nifty India Defence Index

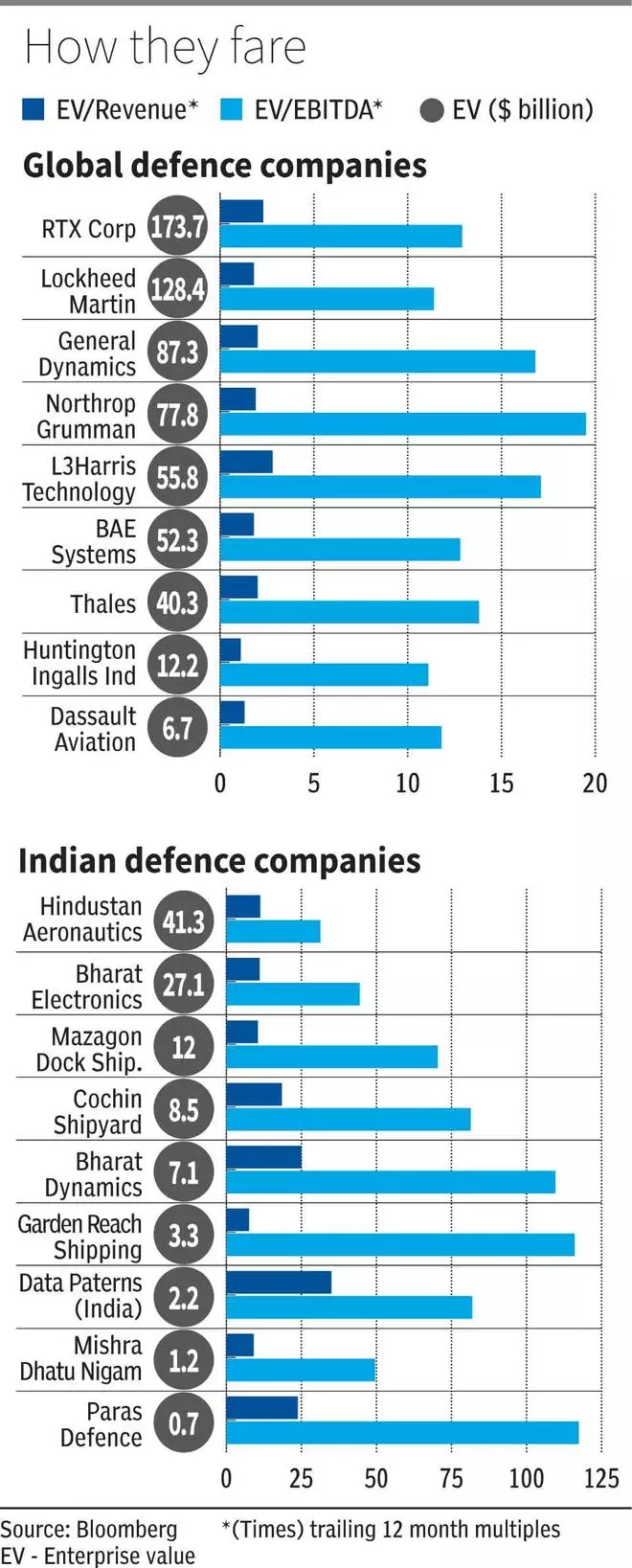

Whereas we’ve got made strides in defence know-how, the truth that we nonetheless have a heavy import invoice in our annual defence capex signifies that there’s a lot extra know-how hole to be crammed. Whereas HAL’s LCA Tejas is making waves and is about to change into the second largest fleet in Indian Air Drive in few years, we nonetheless covet the Rafale manufactured by French defence firm Dassault Aviation for strategic functions.

In not too long ago concluded FY, Dassault Aviation posted income of $5.19 billion and internet revenue of $974 million, whereas HAL posted income of $3.67 billion and internet revenue of $921 million. Nonetheless, HAL trades at enterprise worth (EV) of a staggering $41 billion, whereas Dassault Aviation is valued at a mere $6.7 billion.

A bull would argue the expansion alternative that favours Indian defence shares. However, listed here are some attention-grabbing information – over the following two years Dassault Aviation income/earnings is predicted to develop at a CAGR of round 24/12 per cent, whereas that of HAL at round 13/8 per cent, respectively. Even once you examine the order backlog, Dassault Aviation exited its current FY (CY23) with a backlog of $41 billion, whereas HAL backlog is at round $11 billion.

- Learn:4 the reason why defence shares must be in your radar

In the event you come to future alternatives, it will be price noting that not simply India, however many different nations are also on a major re-armament cycle given the present geopolitical dynamics. For instance, in a current report on European defence shares, international brokerage home JP Morgan refers to a ‘Europe’s Rearmament Cycle’ that might final not less than a decade. This has been triggered by Russia-Ukraine conflict which dropped at the highlight the underinvestment of NATO nations of Europe in defence capabilities. In response to a report by the German ifo institute, Europe had extracted a peace dividend of $1.8 trillion between 1991 and 2023, by spending lower than their NATO mandated goal spending on defence. It’s now catch-up time and will current a bonanza for defence firms there, extra in influence when it comes to future alternatives than that for Indian defence firms. However traders there will not be even remotely reflecting euphoria as witnessed right here (see desk).

- Learn:Motilal Oswal AMC launches its Nifty India Defence Index Fund

One other instance is once you examine shipbuilders like Mazagon Dock with the biggest shipbuilders within the US and main defence firm there – Huntington Ingals. Mazagon Dock has an EV of $12.03 billion that values it virtually as a lot as Huntington Ingals, though its income at current is lower than 10 per cent of that of Huntington Ingals!

What’s amiss?

Shares are well worth the internet current worth of their future money flows, which aren’t completely forecastable. So the talk on truthful valuation will all the time be by no means ending. However then when shares proceed to maneuver on no vital information, outpace their enterprise progress and commerce at valuations completely incomparable with international friends, a few of them with superior know-how, lengthy execution monitor file and equally good prospects, traders have to take inventory.

As Warren Buffet as soon as mentioned – ‘Sadly, nonetheless, shares can’t outperform companies indefinitely’ A painful retreat in defence shares is sort of a believable state of affairs, and it’s higher that basic traders take cowl.

#HAL #BEL #Cochin #Shipyard #Mazagon #Dock #GRSE #Midhani #Goliath #valuation #visavis #international #friends