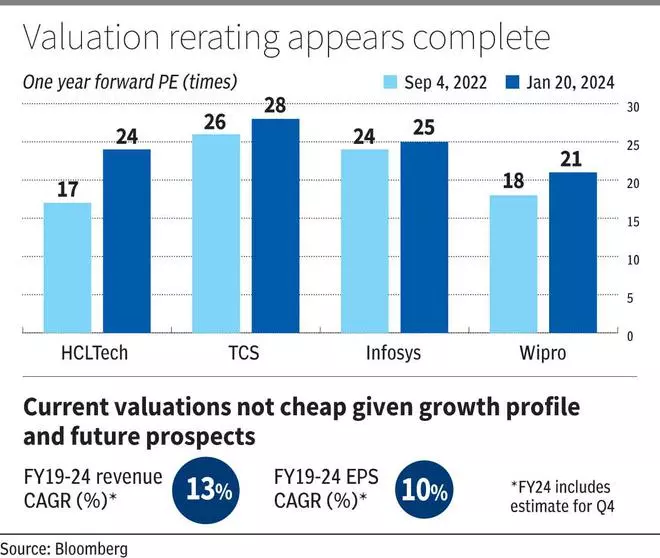

In our version dated September 4, 2022, we had given an accumulate ranking on the inventory when it was buying and selling at ₹924.85. Elements that labored in its favour then had been engaging valuations with one-year ahead PE at 16.9 occasions (vs Infosys buying and selling at 23 occasions and TCS at 26 occasions in September 2022), EV/FCF of 19 occasions and engaging dividend yield of 5 per cent.

Usually, amongst the top-tier IT firms, EBIT margin ranges make a case for distinction in valuation — larger margins suggest larger valuation except variations in long-term development potential are important. Whereas HCL Tech margins (18-19%) had been decrease versus TCS (24-25%) and Infosys (20-21%), given comparable long-term development prospects , our view was that the low cost in valuation versus TCS and Infosys was extreme. Our core expectation was that valuations will re-rate for HCL Tech.

Since then, HCL Tech is up 67 per cent versus TCS, Infosys and Wipro up 25 per cent, 13 per cent and 17 per cent respectively. Nifty IT is up 33 per cent on this time interval. With this outperformance, we consider the valuation re-rating in HCL Tech is essentially full. Therefore, traders can ebook income and lock in on the positive aspects.

HCL Tech now trades at 24 occasions one-year ahead EPS, and nearly on par with Infosys, which has higher margins. Its low cost in valuation with TCS (industry-leading margins) has additionally narrowed, from 35 per cent in September 2022 to 14 per cent now. On a relative and absolute foundation, the inventory of HCL Tech shouldn’t be engaging anymore.

Latest efficiency

Amidst weak {industry} developments, HCL Tech’s December quarter efficiency, whereas reflecting the slowdown, was modestly forward of consensus expectations, with income round 1 per cent above consensus and web revenue 4 per cent above. The earnings beat was pushed by better-than-expected EBIT margins which, at 19.7 per cent, had been 70 bps above consensus. Nonetheless, regardless of the beat in 3Q, the corporate maintained prior FY24 income (fixed forex income development of 5-5.5 per cent) and EBIT margin outlook (18-19 per cent) with minor tweaks. In FY23 CC income development was at 13.7 per cent.

The corporate derives round 88 per cent of income from IT companies (together with 16 per cent from Engineering and R&D companies) whereas its software program merchandise enterprise accounts for steadiness 12 per cent. In December Q, the better-than-expected efficiency was pushed by the merchandise and ER&D segments.

Geographic and vertical developments had been barely opposite to friends, with HCL Tech seeing YoY development in Finance vertical and in North America (round 60 per cent of income). For instance, Infosys witnessed a 5.5 per cent decline in revenues from North America. Nonetheless, it might be too early to conclude that developments have bottomed out in key verticals and geographies. The demand setting stays unsure in keeping with administration, and as such there is no such thing as a uptick in discretionary spending for now.

Whereas the corporate stays well-positioned for the long run, together with tapping alternatives within the area of generative AI, the medium-term outlook stays cloudy. After a few years of double-digit fixed forex income development exiting FY23, HCL Tech, TCS, Infosys and Wipro are seeing mid-single digits to flattish income efficiency in FY24.

Given looming macro headwinds with inflation but to achieve central financial institution goal ranges in developed economies and rates of interest remaining excessive, even when there may be revival in FY25, returning to double-digit income development seems to be two years away (possible in FY27). On this context, the valuations should not low-cost. With HCL Tech shares delivering stable returns in a 12 months of slowdown, restoration prospects are already priced in. This, mixed with the shrinkage in valuation reductions, makes the risk-reward unfavourable from right here.

Why

Valuation on par with Infosys now

Low margin of security at present ranges

Slowdown could persist in FY25

#HCL #Applied sciences #Traders #Ebook #Income #Inventory