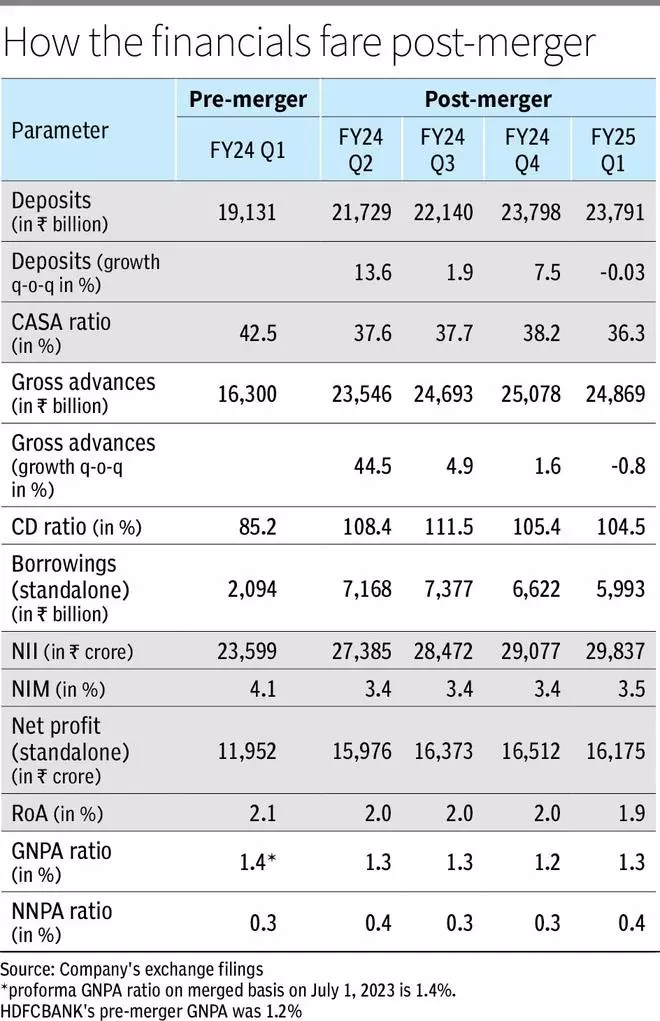

Whereas the financial institution has inherited the mortgage e book of the housing finance NBFC, it has additionally inherited an unfavourable credit-deposit ratio (CD ratio) together with it — one thing as excessive as 109 per cent. Bringing this ratio to safer ranges goes to be a Herculean process for the administration, given the waning patronage for financial institution deposits. Put up the merger, the financial institution has certainly slowed the tempo of mortgage progress and focussed on deposit progress. CD ratio, too, has declined to 104.5 per cent as of June 2024. As the opposite features of the financial institution’s fundamentals are largely all proper, we suggest that traders accumulate the financial institution’s shares, whereas preserving a watch on the deposit progress, going ahead. Learn on as we take a better take a look at how the financial institution has fared within the 12-month interval post-merger.

The credit-deposit conundrum

The merger fetched a cool mortgage e book of about ₹6.25 lakh crore to HDFC Financial institution’s books. However alongside got here a staggering CD ratio of 109 per cent. It is because, deposits made up solely 26 per cent of HDFC Restricted’s monetary liabilities (FY23), whereas loans and debt securities made up for the remainder. That is method decrease when in comparison with HDFC Financial institution pre-merger, the place deposits made up 87 per cent of the financial institution’s liabilities. And deposits, particularly the present accounts and financial savings accounts (CASA), are low-cost basically, versus the loans and debt securities. The Web Curiosity Margin (NIM) additionally took a success because of this and dropped from 4.1 per cent pre-merger to three.4 per cent, 1 / 4 previous the merger.

The administration recognises this and has since gone slower on the advances freeway. Whereas gross advances have grown 5.6 per cent between Q2 of FY24 and Q1 of FY25, deposits have grown 9.5 per cent in the identical interval. Gross advances got here in at ₹24,869 billion as of Q1 FY25, having declined 0.83 per cent on a sequential foundation.

On the deposits entrance, the financial institution registered a minor de-growth of 0.03 per cent on a sequential foundation in Q1 FY25. The administration attributes this to the seasonal nature of the quarter, aggravated by unanticipated run-offs within the present account balances. On a QoQ foundation, time deposits grew 3 per cent and financial savings accounts noticed a gentle de-growth of 0.38 per cent. The QoQ de-growth in present accounts was substantial although, at 13.8 per cent. This even led to a fall within the CASA ratio, from 38 per cent in This fall FY24 to 36 per cent now.

Nonetheless, an evaluation of the knowledge on quarterly common deposits included by the financial institution in its analyst deck paints a unique image. Since FY22, the financial institution has recorded a imply sequential progress in common deposits of 4.98 per cent for the primary quarter of a monetary 12 months. For FY25 Q1, the QoQ progress in common deposits has are available at 4.59 per cent, which appears largely positive. The administration is hopeful of rising deposits, leveraging the financial institution’s mammoth community and repair high quality, with out going aggressive on the deposit charges. The financial institution has added round 2 million clients throughout the quarter.

So far as borrowings are involved, the financial institution has lowered ₹629 billion throughout the quarter. In consequence, borrowings as a proportion of whole capital and liabilities have declined from 21 per cent as of the primary quarter after the merger (September 2023), to 17 per cent now. The administration expects to settle one other ₹350 billion at maturity and a few extra earlier than maturity, throughout the upcoming quarters of FY25.

Revenue, prices and asset high quality – a better look

Web Curiosity Revenue (NII) has grown 26 per cent for the 12 months post-merger, in comparison with the NII for the 12 months previous the merger. For Q1 FY25, regardless of the sluggish deposits, particularly the low-cost CASA deposits, the financial institution managed a marginal enhance in NIM of three foundation factors (QoQ) to three.47 per cent, owing to spreads remaining intact.

Web revenue has grown 39 per cent for the 12 months post-merger, in comparison with the 12 months previous the merger. For Q1 FY25, web revenue declined 2 per cent sequentially. This is because of two causes. First, This fall FY24 noticed sure one-off objects reminiscent of transaction good points and tax credit, giving a excessive base. Second, payment revenue throughout the bygone quarter declined by ₹10 billion, spearheaded by the autumn in payment revenue from third-party merchandise. Working bills have been down 7.5 per cent, resulting in a cost-to-income ratio at 41 per cent, having shed 30 bps on a QoQ foundation. The administration is sanguine about taking this additional right down to round 30 per cent ranges because the financial institution settles high-cost borrowings and replaces them with deposits within the transition interval.

Asset high quality has largely remained regular post-merger. Q1 FY25 GNPA ratio rose marginally from 1.24 per cent to 1.33 per cent sequentially owing to a 20 bps and a ten bps rise within the GNPA ratio of CRB (Business and Rural Banking) and company segments, respectively. Asset high quality deterioration within the CRB phase is basically because of seasonality. Credit score prices have declined and are flat at 42 bps.

Backside line

The shares of the financial institution are down near 10 per cent from the latest highs of ₹1,794. The financial institution is buying and selling at a trailing price-to-book worth of two.59 occasions on a consolidated foundation. The FY25 and FY26 ahead price-to-book worth stands at 2.49 and a pair of.2 occasions. Therefore, accumulating the financial institution’s shares could be applicable for many who want to stand with a resilient financial institution because it finds its seemingly misplaced glory by means of a troublesome transition interval. Given its pristine monitor document, underperformance within the shares throughout the transition part provides a great alternative for long-term traders.

#HDFC #Financial institution #Traders