Unsurprisingly, the outcomes mirrored the bottom actuality and earnings progress has taken a breather within the quarter. The present valuation of Nifty 50 at 19 instances one-year ahead earnings will demand the next earnings progress within the the rest of the yr.

Whereas value pressures have eased in some pockets, worries nonetheless stay in others. Curiosity prices transferring up will even be a priority henceforth. Nevertheless, what can assist earnings is healthier demand. Even because the managements acknowledged the high-cost atmosphere, the commentary following Q1 outcomes additionally mirrored optimism on the demand outlook. The sharp restoration in broader index because the outcomes season handed (Nifty 50 returned 8 per cent from mid-July 2022) has been supported by persevering with plans for progress, both in capability or in worth supply throughout sectors. Thus, whereas the print in Q1 FY23 is adverse for buyers, the bigger demand outlook appears encouraging. Right here’s an in depth have a look at the traits on this quarter and what might lie forward. The evaluation is for 1,268 listed firms whose Q1 FY23 numbers have been out till August 7.

Revenues profit from low base

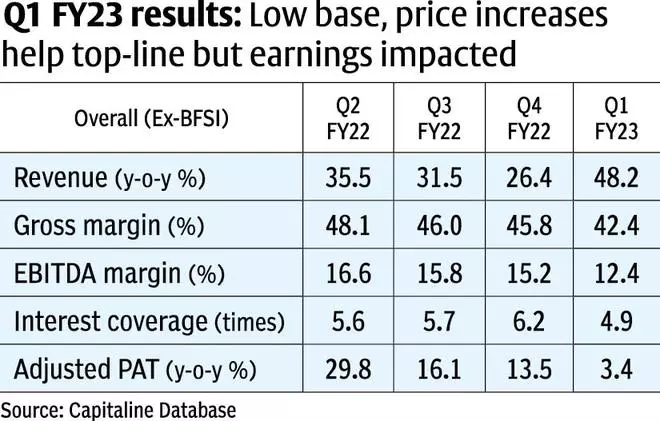

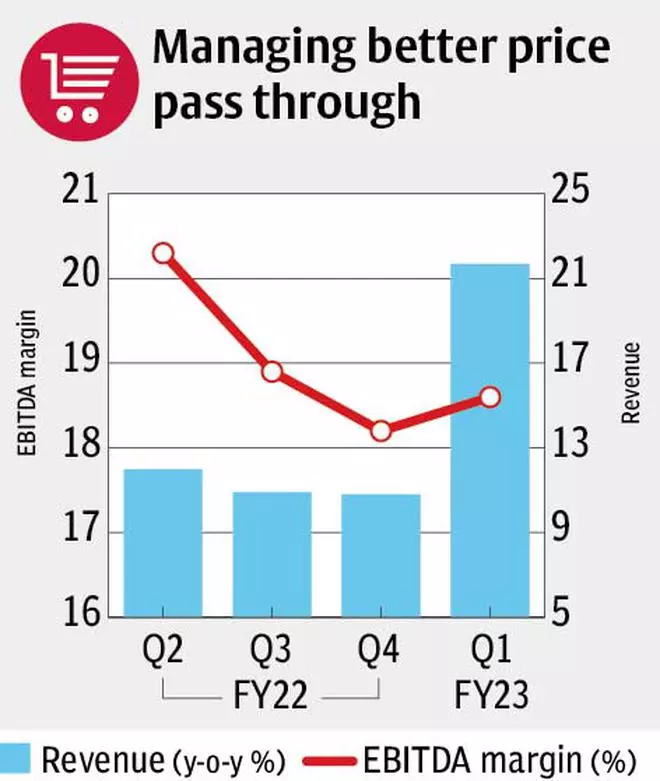

Income progress (excluding financials) was reported at 48 per cent year-on-year in Q1 FY23 in comparison with a median 31 per cent year-on-year progress within the earlier three quarters. However contemplating the weak base of Q1 FY22 (peak second wave in Could-June 2022), a sequential progress could also be indicative. The income progress was at 7 per cent quarter-on-quarter in Q1 FY23, decrease than the 9-13 per cent sequential progress seen within the earlier three quarters. Seen along side steep decline in each gross and EBITDA margins, defined beneath, it implies that the income progress was a operate of value pass-through at the price of quantity progress. Segments using on power value inflation — refineries, energy and gasoline sectors reported sequential progress of 17, 19 and 32 per cent respectively, quarter-on-quarter. Then again, cement sector noticed revenues falling 1.3 per cent quarter-on-quarter. Metal sector, which witnessed a pointy correction in metal costs, additionally witnessed 10 per cent quarter-on-quarter decline in revenues.

Margins beneath stress

Excluding financials, gross margins have been on a continuing decline in latest quarters owing to provide chain constraints earlier and important commodity value inflation now. From gross margins of round 50 per cent in Q1 FY22, each quarter witnessed steady decline and reported 42 per cent gross margins in Q1 FY23. However on the operational stage, greater asset utilisation and price efficiencies had restricted EBITDA margin decline until This autumn FY22 (solely 140 foundation factors year-on-year decline). The present quarter witnessed EBITDA margins at 12.4 per cent, which is a 470-basis level year-on-year decline or 280 foundation factors quarter-on-quarter. So, regardless of passing on greater enter prices to the extent potential which helped the topline, EBITDA margin declined as gross margins got here down. Financial savings from worker and different bills as a proportion of gross sales have been restricted this time round. Therefore, the decline in gross margins mirrored in EBITDA margins this quarter. All this weak point flowed by to the underside line.

Earnings (progress) resilience lastly cracks

Even within the face of constant inflation from the center of final yr, India Inc was capable of shield earnings progress till now. PAT (adjusted) progress (excluding financials) was at 14 per cent in This autumn FY22, declining from 30 per cent in Q2 FY22. However within the present quarter (Q1 FY23) when nearly all the basket of uncooked supplies examined new highs, the PAT progress lowered to three.4 per cent year-on-year progress (even on a weak base of Q1 FY22). Partial pass-through of enter value inflation and decline in gross sales quantity impacted revenue progress, aside from the elevated debt financing prices. Because the pandemic, one of many causes for improved outlook of India Inc was the deleveraging story. But when the profitability continues to stay pressured for the remainder of the yr, this issue could come into focus once more. Curiosity protection ratio had been ascending from 4.2x in mid-FY21 to six.2x on the finish of This autumn FY22, but it surely has contracted to 4.9x at present. That is even earlier than most firms’ debt phrases have mirrored the upper rate of interest traits that began solely in Q1 FY23. The excessive capex plans introduced, if unchanged, mixed with greater debt-financing prices, on a shrinking profitability base can have a big sufficient affect. Capital-intensive sectors like cement and metal have a snug ratio of 6.7x and 5.7x respectively, however are 30 per cent decrease than solely the earlier quarter. Car sector’s curiosity protection ratio was at 1.7x in Q1 FY23, down from solely a slightly snug vary of two.8x in This autumn FY22. Tata Motors, Ashok Leyland and TVS Motors might enhance their monetary leverage place because the restoration in Auto demand performs out.

Sectoral breakdown

The outcomes evaluation has some pointers in the direction of a adverse outlook owing to value inflation. Some respite has been evident in enter supplies led by metals together with metal. At the same time as different commodity prices stay unstable within the quick time period, the demand pick-up ought to support most sectors. Going past reported numbers, the sectoral commentary on outcomes efficiency has been optimistic. Right here’s the outlook for key sectors which have confronted robust value headwinds in latest instances.

FMCG

In accordance with Nielson analysis, post-Covid FMCG progress has been price-led with flattish quantity progress over a three-year interval. In Q1 FY23, business leaders corresponding to HUL, Nestle and Dabur reported a robust value progress (12-15 per cent year-on-year) and decrease quantity progress (3-4 per cent year-on-year). The partial pass-through of the uncooked materials inflation (15-20 per cent year-on-year) resulted in gross margin contraction of 240 foundation factors year-on-year within the sector. The one solace witnessed in costs by July-August 2022 has been from edible oils and packing supplies to an extent. The subdued quantity progress of the final three years ought to present a softened base for quantity progress when value financial savings, if any, are handed on.

Whereas the short-term outlook grapples with value points, the longer-term outlook is constructed on premiumisation and rural progress. Past value and quantity, the business can be aiming for greater contribution from premium product combine (HUL and Godrej Client merchandise) and a stronger rural push (Nestle). The shortage of downtrading even in high-cost inflation interval factors in the direction of a robust demand atmosphere and accordingly ought to assist the following leg of progress, in accordance with firms.

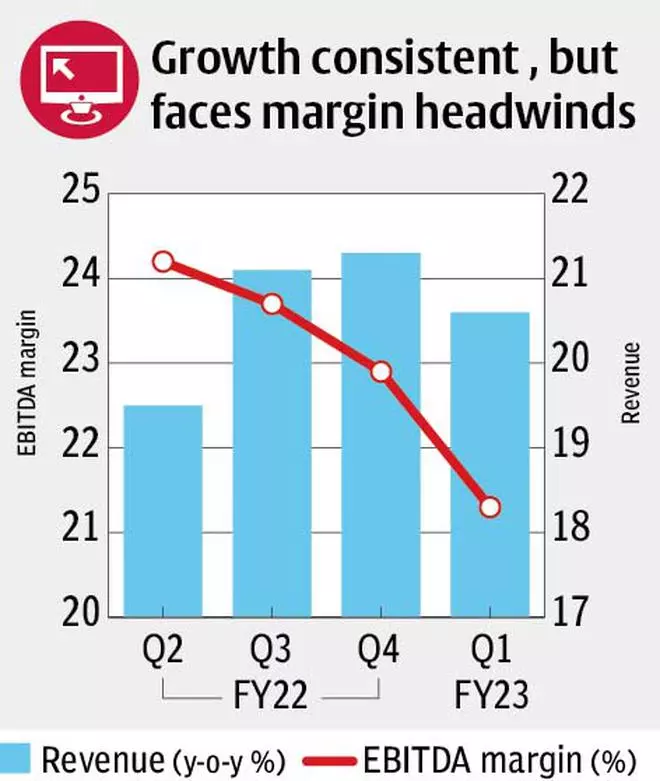

Vehicles

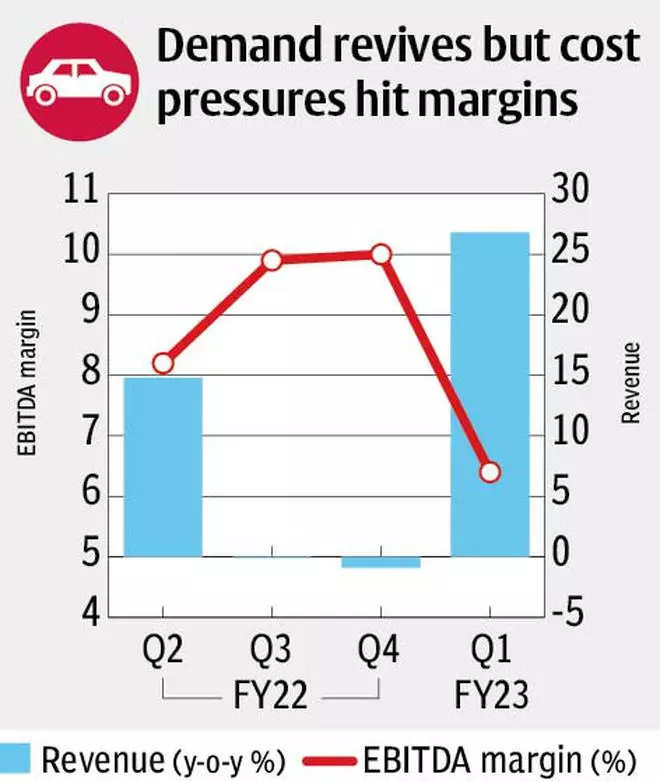

The demand outlook for Autos led by four-wheelers is robust. Whereas the persevering with chip shortages have created provide challenges, that is including to the already-strong order e-book place of the businesses. The business has been capable of moderately go on the upper commodity costs of This autumn FY22 (primarily metal) with 100-200 foundation factors value will increase. Even so, the margins are beneath stress owing to greater advertising spends and decrease utilisation because of chip shortages in some instances. The 20 per cent correction of metal costs throughout March-August 2022 ought to be mirrored within the second half of the yr.

The demand for SUV autos has elevated together with demand for a lot of options (car kind, design and comfort). That is mirrored within the product combine as effectively, driving greater realisations for firms. Led by launch of recent fashions within the SUV class the topline progress ought to be led by greater quantity and value realisations whilst cooling enter costs are handed on. Business chief Maruti Suzuki is continuous with their capability growth plans unabated to serve elevated demand.

The CV (industrial car) market can be within the midst of a cyclical restoration in demand. The agricultural demand outlook remains to be weak which is mirrored in bike gross sales with restoration depending on higher monsoon. The export market, even when numerous sufficient, is beneath systematic world stress resulting in volatility in gross sales.

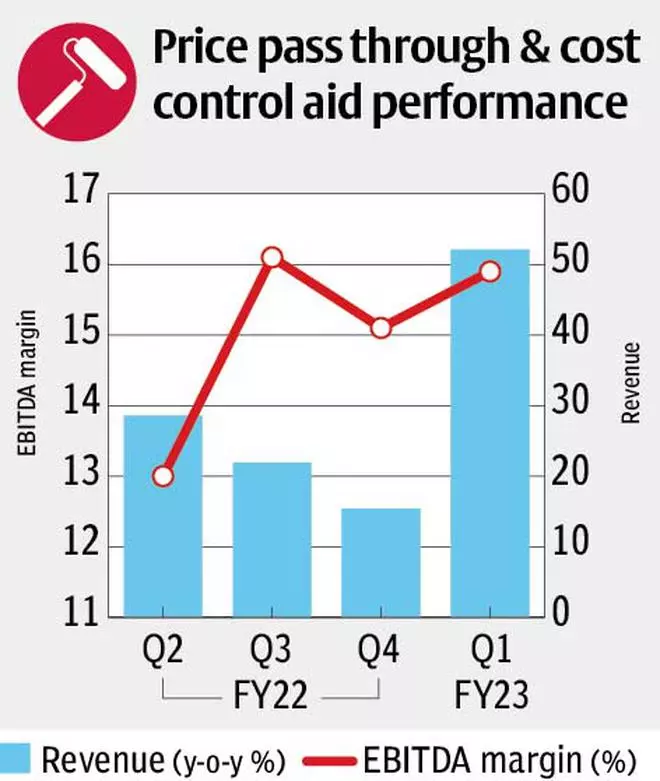

Cements and Paints

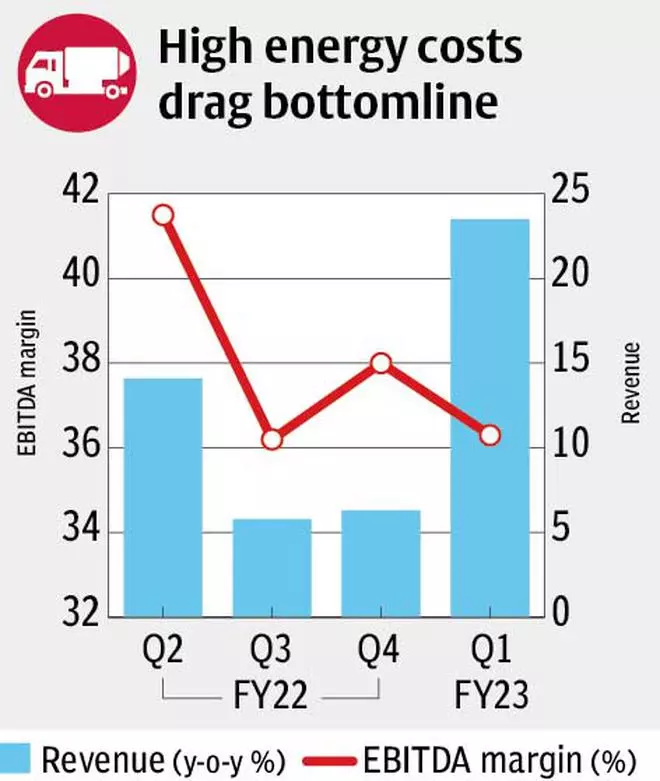

Supplying to the development business, paints and cements face various prospects. Vitality-intensive cement business confronted 50 per cent year-on-year power value inflation together with different uncooked materials inflation in Q1 FY23. The cement business handed on the upper prices by value will increase various from 25 per cent to 50 per cent year-on-year. The excessive value pass-through impacted quantity progress resulting in weak income progress within the quarter. The power prices (petcoke, crude and derivatives) have marginally eased at present in comparison with Q1 FY23. This could bode effectively for quantity off-take. In the long run, demand progress expectations are nonetheless excessive mirrored within the capability addition plans of firms. For instance, UltraTech and Shree Cement count on so as to add capability within the close to time period.

The paints business continues to face robust progress as evidenced by the chief Asian Paints and different members reflecting comparable progress. The sector managed each quantity and value progress as whole income reported 14 per cent quarter-on-quarter progress in Q1 FY23, even after passing 300-400 foundation level value will increase within the quarter. The gross margins, nonetheless, declined marginally, however higher management of worker and different prices managed the affect on EBITDA margins. The softening of crude derivatives is anticipated to circulation by to base chemical compounds, then to specialty chemical compounds earlier than softening solvents prices which ought to support the paints business. This suggests a gradual profit from decrease present crude costs. The improved product combine in tier-1 and tier-2 centres for Asian Paints is offsetting to an extent the weak point in remaining centres, that are additionally anticipated to choose up shortly.

If excessive curiosity prices don’t play spoilsport, the restoration in actual property demand, continued progress in inexpensive housing and authorities push on infrastructure ought to act as tailwinds in institutional demand for each paints and cements business.

Data Know-how

The highest-line progress continues unabated for IT majors at 20 per cent year-on-year. The sequential progress from Europe was weak throughout most firms, whereas North American progress continues. The outlook commentary for the first area (North America) will be characterised as optimistic with just a few {qualifications} as of now. Both progress of funds allocation or velocity of deal finalisation are the seen sore spots. This suggests a slight headwind for progress in e-book to invoice ratio. Whereas S&P earnings throughout US firms proceed to develop, shopper going through industries are exhibiting indicators of stress. Infosys not too long ago introduced weak point in mortgage section and there was a slew of earnings revision in retail together with Walmart in July 2022. A powerful restoration from recessionary overhang within the US shall be required by IT business to beat any lingering doubts on its sectoral outlook.

IT companies majors reported 100-200 foundation level EBITDA margin decline as primarily worker prices elevated with additional will increase pending in Q2 FY23. Different prices, together with subcontracting and normalisation of journey and visa bills, have additionally impacted margins. The business additionally reported a greater scope for pricing progress in contracts based mostly on cost-of-living index, trickling down in a single or two quarters.

#India #fared #highway #forward