Then again, the US FDA incentivised generic submitting, which introduced in additional competitors, additional weakening sellers of generics. Generics, going through 5-8 per cent erosion earlier, at the moment are observing 15-20 per cent erosion yearly. This suggests that for a base portfolio of 100 merchandise, 15-20 new launches are wanted yearly to report marginal optimistic development from generics.

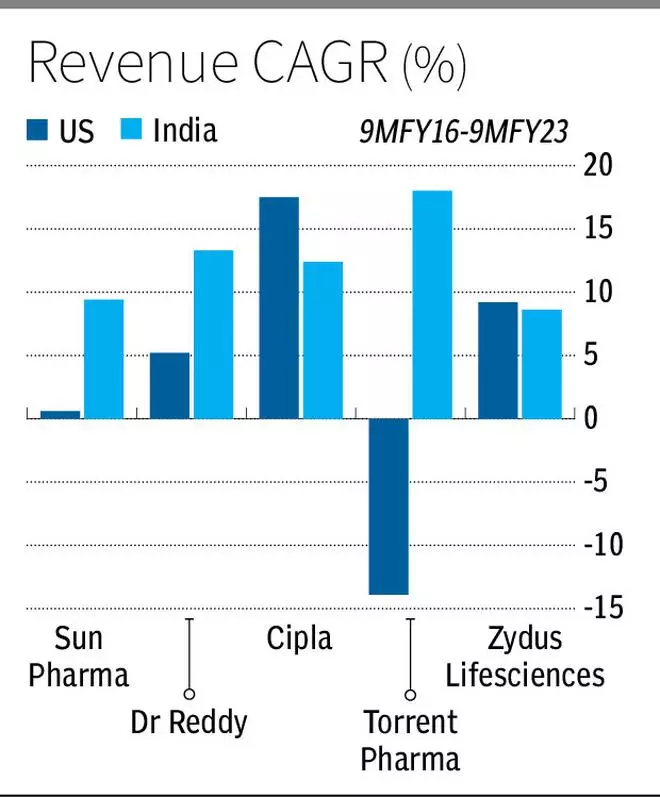

With the highest Indian firms having publicity of 12 to 42 per cent on this geography, worth erosion in generics has impacted them deeply. In opposition to common Indian income CAGR development of 12.3 per cent for the highest 5 firms, the US reported 3.7 per cent CAGR in 9MFY16-9MFY23. To mitigate this, Indian pharma gamers have been making an attempt out varied routes so as to add worth and enhance profitability from the US markets. Right here’s how they’ve been navigating difficult roads:

Para IV software underneath ANDA

Abbreviated New Drug Software or ANDA is the foremost pathway for Indian generics. ‘Abbreviated’ on this case refers back to the efficacy and security analysis of the innovator reused by the generic whereas submitting, thereby saving time. Primarily based on innovator’s patent standing, this pathway has 4 routes or Paragraphs to file. Para I, II and III are used when no patent problem is concerned and no exclusivity is focused. In these routes, assuming ten different filers collect within the first six months for the product, erosion can attain 95 per cent and EBITDA margins meander in 15-20 per cent vary at finest.

A Para IV certification, alternatively, can grant a 180-day exclusivity to the generic filer, a interval whereby the innovator and the generic are allowed to function available in the market — permitting for lumpsum revenues and a better 20-30 per cent EBITDA margins. Therefore, this route is extra value-adding. Beneath a Para IV software, the generic filer asserts that innovator patents are both unenforceable or are usually not infringed or are invalid. The generic filer notifies the innovator of the Para IV submitting inside 20 days, after which there might be an automated 30-month keep holding again FDA approval, in order to conclude the authorized proceedings. Inside the 30-day interval, if the generic firm wins the ruling, they’ll have the ability to market the product instantly (earlier than the patent expiry) and completely for a interval of 180 days, ranging from the day of commercialisation.

The generic filer may additionally enter right into a settlement settlement with the innovator for a delayed launch. If there isn’t any consequence after the 30-month interval, the generic filer can probably think about an at-risk launch, that’s launching the product (with 180-day exclusivity) risking patent infringement in case the innovator wins the authorized course. For instance, Dr. Reddy’s launched Suboxone ‘in danger’ in November 2018 whereas in a Para IV litigation with the innovator. Whilst a brief restraining order was filed, it was later lifted. Dr. Reddy’s settled for $72 million from the innovator for the misplaced gross sales after it confirmed that it was non-infringing on innovators’ patent strengthening its steadiness sheet from the one-time ‘different earnings’.

One outstanding instance of settlement in a Para IV is the Revlimid launch. Whereas the patent is meant to run out in April 2027, a number of filers have launched in 2022 after settling with the innovator Celgene. Natco and its associate Teva have additionally secured a 180-day exclusivity for 4 strengths of the drug, being the primary applicant to problem the patents. Natco’s Q1FY23 revenues jumped by $40 million (44 per cent QoQ) with solely a fraction of income share (round 33 per cent). The others have settled for a volume-limited launch till 2026 whereby they’re proscribing themselves to pre-defined volumes. Dr. Reddy’s North America revenues improved by $120 million sequentially (52 per cent) in Q2FY23, pushed primarily by gRevlimid.

Aggressive generic remedy

Aggressive generic remedy (CGT) got here into the image in 2017 to incentivise generic submitting in medicine with insufficient generic competitors. Beneath CGT, a 180-day exclusivity is offered for profitable ANDA submission of the primary applicant, even when no patent safety exists. Candidates can request for CGT classification of the drug previous to or throughout an ANDA submission, which is evaluated based mostly on lack of actively promoting generics. The applicant can even count on an expedited evaluate timeline and an 180-day exclusivity on launch.

There are near 50 filers for Advil (Ibuprofen) within the US, every with totally different dosages and routes of administration, which means a $2-5 million income run price. Strides Pharma secured a CGT approval in such a aggressive area for its Toddler Advil drops in June 2022 together with a 180-day exclusivity and is simply generic for the product. The corporate ought to ideally count on to make $7 million from the product within the first 180 days and round $2 million per quarter publish exclusivity, in comparison with $40-million market dimension. For comparability, if this have been a plain generic with 7-10 filers and no exclusivity, the product would have netted $2 million within the first 12 months. Amphotericin for Solar Pharma, Vigabatrin for Dr. Reddy’s and Dihydroergotamine Mesylate for Cipla are a number of the different examples in current durations. In Q1FY23, Zydus introduced that three of the eight launches within the quarter have been authorized underneath CGT pathway.

.jpg)

505 (b)(2) software

Half-way between a full-blown new chemical entity approval (505(j)) and a generic submitting lies a 505(b)(2) approval. This route is used when a change is made with regard to the unique when it comes to dosage, power, routes of administration, or authorized remedy label with the intention to enhance affected person outcomes, comfort or ease of administration. The pathway incorporates the protection and efficacy knowledge of the innovator and new scientific trials carried out by the filer to substantiate the modifications carried out. Prescription to OTC change, tablets to pellets/sprinkles, a brand new mixture of medication are some types that use this pathway together with a ‘bridging’ scientific trial to substantiate the effectiveness.

The exclusivity underneath this pathway relies on the extent of scientific trials that might be required by the FDA. However even in any other case, the product authorized as model in US markets supplies for a far longer income timeline earlier than erosion.

Solar Pharma’s Yonsa (prostate most cancers), a vital product in its speciality portfolio, was authorized as an NDA (New Drug Approval) underneath the 505(b)(2) pathway with scientific trials. The product has patent safety till 2034, however generics of the unique can nonetheless enter the market. In opposition to the $4-8 million {that a} generic filer ought to have anticipated, the 505(b)(2) pathway might have aided Solar Pharma web $15-20 million from the product per 12 months. Contemplating the branded promotion, the erosion curve is likely to be much less steep and EBITDA margins nearer to innovator stage of 30-35 per cent. Cipla’s Lupron Depot injection and Dr. Reddy’s Bortezomib are another launches which have used this route to enhance profitability of their US publicity.

Biosimilars

Biosimilars are generics of biologics. Biologics, in flip, are usually not chemically synthesised however derived from pure sources, together with micro-organisms, animals or people and are bigger in comparison with ‘small molecules’ (10-100 instances bigger).

Innovators are preferring biologics in comparison with small molecules owing to excessive worth attributed to immunogenicity of biologics (evoking an immune response) and manufacturing complexity. Patent expiry might not suggest a steep fall right here, defending innovators as nicely. This suggests that Indian operators ought to eye this piece of pie to remain related in US markets, they usually have been doing so.

A biosimilar addressing a $2,000 million innovator market in US (Biocon with biosimilars of Pegfilgrastim, Trastuzumab or Glargine, as an illustration) can count on to make $70-150 million per 12 months, going by the height market share of 10-20 per cent and a reduction of 50-60 per cent from innovator worth. Whereas this can be perceived as decrease than anticipated return for the time it takes to go to market, (3-4 12 months improvement timeline), and the related investments required ($100 million in improvement prices), proponents’ concentrate on the elongated timelines with decrease erosion, sticky market share and innovator stage margins at 35 per cent. Additionally, US or European approval paves the best way for rising market play. Most main Indian generic gamers, together with Solar Pharma, Cipla and Aurobindo Pharma, are eyeing a bit of biosimilar franchise by 2030.

Advanced merchandise

Firms at the moment are transferring past plain generics to merchandise which might be differentiated on manufacturing problem. Zydus Lifesciences’ portfolio has had a excessive focus of such merchandise. Mesalamine, a fancy product, as an illustration, has upwards of 20 filers in numerous routes. Nevertheless, Zydus’ delayed launch pill model of this drug now has sole presence as even the innovator has discontinued the product as per the FDA’s authorized drug checklist.

With such low competitors the generic ought to have raked in $40-60 million every year in comparison with a mere $10-20 million that different dosage types of the generic filers count on. Cipla’s Advair Diskus, a mix of inhalation powder and a tool to manage, each of which rating excessive on complexity, have been anticipated to be out in a 12 months (however impeded by plant clearance). Business chief Solar Pharma is now working on the excessive finish of complexity with patent safety for its main drug Ilumya, which took the innovator route for biologics. Accredited for psoriasis, Ilumya has initiated trials for one more indication as nicely. The height gross sales estimates are within the vary of $300-350 million for the one indication.

Erosion, a given

Innovator, generics, speciality, biosimilar — erosion is a given in pharmaceutical merchandise. It’s only the interval of safety and slope of abrasion that will differ. Innovators are protected by exclusivity for a interval of 20 years, that will embody 7-10 years for improvement.

Evergreening was practised the place new patents have been launched on the finish of safety, however FDA plugged it by proscribing the 30-month keep to at least one per ANDA, on being challenged. After the exclusivity, erosion can vary as much as 95 per cent on day-1 of a generic launch, relying on the complexity of the product and the variety of filers and is typically even discontinued in small molecules.

To cope with such a problem, Pfizer, as an illustration, break up Upjohn with legacy of patent medicine portfolio because the division wanted a separate focus. With a brief window of 8-10 years, innovators elevate costs by 8-10 per cent yearly to maximise income. Even in Biologics with complicated manufacturing, the slope of abrasion might be evident if not punishing. For a profitable product like Humira (biologic) with $17 billion in gross sales, 11 purposes might have been authorized to date concentrating on launch in 2023.

Thus, pharma firms at all times have to be on their toes, on the lookout for methods to plug the gaps and defend their profitability.

#indian #pharma #firms #performing