The present taxation helps taxpayers declare losses in eventualities the place the property worth didn’t admire consistent with inflation as throughout actual property downcycles.

Now underneath the proposed taxation, it is going to be a easy direct math subtracting the acquisition value from the sale value. And the place the distinction is optimistic, pay tax at 12.5 per cent on the identical, assuming you could have held the property for a minimum of 2 years.

Comparability

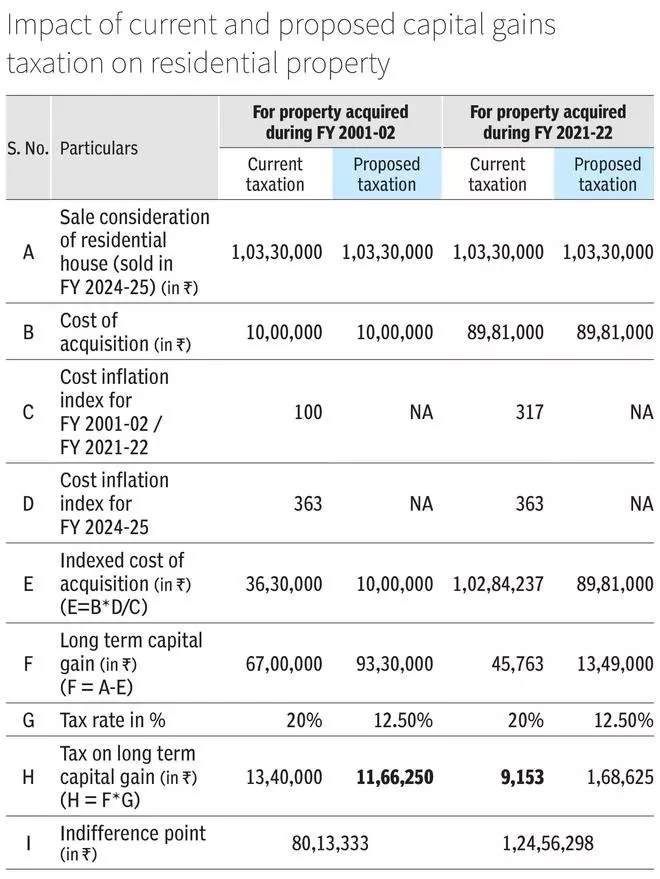

The federal government’s stand is that the proposed scheme with out indexation will assist save taxes higher in most eventualities, than the present taxation with indexation. Within the accompanying desk, we cowl a number of broad eventualities to see in case you profit from the transfer or not.

The numbers thought-about within the illustration are primarily based on market worth of a 1000 sq. ft. condominium in Pune, utilizing NHB’s Residex.

The place the sale consideration as on date, of a property bought for ₹10 lakh throughout FY 2001-02, stands at ₹1.03 crore, the taxpayer would technically profit underneath the proposed taxation because the lowered tax fee helps beat the indexation profit.

However the tax outgo could be detached underneath each the current and proposed taxation at a sale value of round ₹80.1 lakh. Nonetheless, any improve within the sale value past this indifference level, would make the brand new taxation useful.

That mentioned, for a property bought as lately as in FY 2021-22, the indexation profit supplied by the outdated tax taxation comfortably beats the advantage of the lowered tax fee.

The indifference level for this is able to be round ₹1.25 crore and equally, any sale value above the indifference level makes the brand new taxation useful.

Gray Space

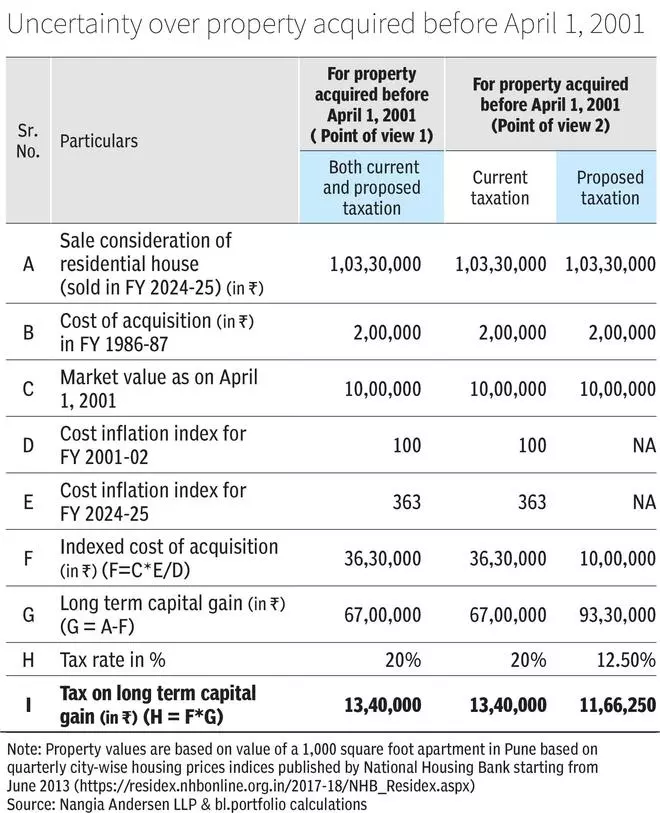

On the face of funds paperwork, it was plainly mentioned that the indexation profit is eliminated as an entire. Nonetheless, within the post-budget convention, it was acknowledged that within the case of properties acquired earlier than April 1, 2001, the indexation profit is obtainable solely as much as April 1, 2001.

Assume that this property was purchased in FY 1986-87 for ₹2 lakh. That is introduced as much as the Honest Market Worth (FMV) as on April 1, 2001, as per tax legal guidelines, which might be ₹10 lakh, consistent with the illustration.

Consultants we spoke to are of the view that the indexation profit is obtainable until the date of sale, and that the proposed taxation will not be relevant, thus ensuing a tax outgo of ₹13.4 lakh (as per present taxation).

Nonetheless, there’s additionally one other interpretation that no indexation profit accrues publish April 1, 2001 and the preliminary train to deliver the acquisition value to FMV as on April 1, 2001 is simply allowed. This could lead to a tax outgo of ₹ 11.7 lakh as defined within the illustration.

Readability is awaited on this regard.

#change #capital #features #tax #property #impacts