From April 1, with positive aspects being taxed at slab charges, debt mutual funds have joined the ranks of the opposite fastened revenue choices — fastened deposits, NCDs, small financial savings schemes and Authorities of India bonds — the place curiosity is taxed at your slab price. This raises the bar on the returns you should get to a constructive actual return from debt investments.

India’s CPI inflation has averaged 6 per cent over the last decade. At efficient tax charges of 10.4 per cent, 20.8 per cent and 31.2 per cent together with cess, you would want a pre-tax yield of about 6.7 per cent, 7.5 per cent and eight.7 per cent respectively, to match this inflation price.

However in search of increased yields from debt devices comes with the next danger of default. So, are you able to fish for increased yields with out compromising an excessive amount of on the security facet? Sure, you may. We run by means of the whole gamut of debt choices, to supply these actionable concepts.

Good outdated PPF and EPF

With the federal government on a mission to root out tax breaks, the pool of debt devices that give you a tax-free curiosity has been drastically shrinking. However two government-backed avenues that proceed to supply tax-free curiosity payouts are the Workers Provident Fund (EPF) and Public Provident Fund (PPF).

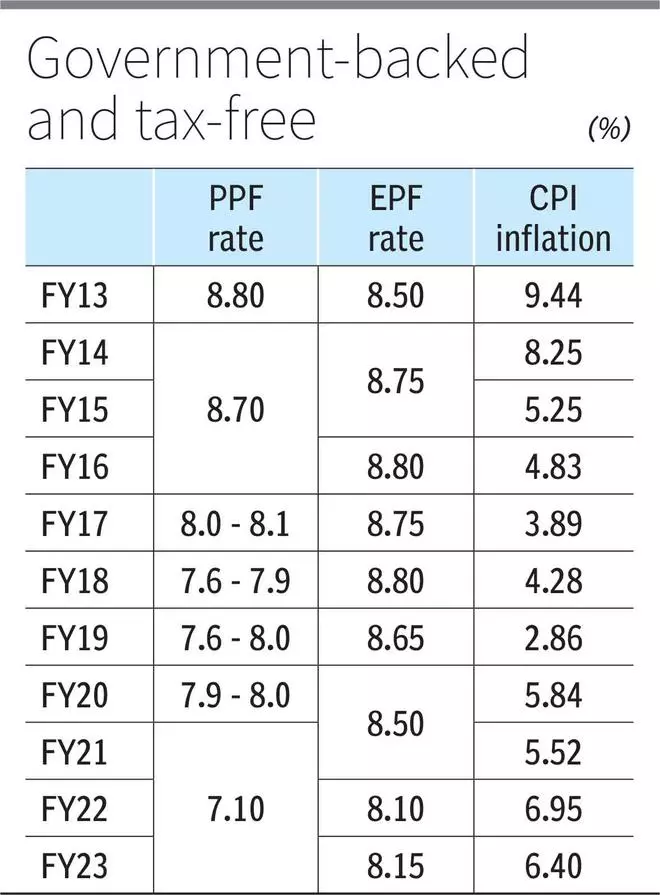

The PPF, which represents a authorities of India borrowing, pays curiosity based mostly on government-declared charges each quarter. It at the moment presents 7.1 for the April-June 2023 quarter. Within the final decade, rates of interest on PPF have ranged between 7.1 per cent and eight.8 per cent.

The Workers Provident Fund (EPF), which invests in Central and State authorities securities and extremely rated company bonds, with a few 15 per cent fairness allocation, has credited curiosity to its subscribers at 8.10 to eight.80 per cent within the final ten years.

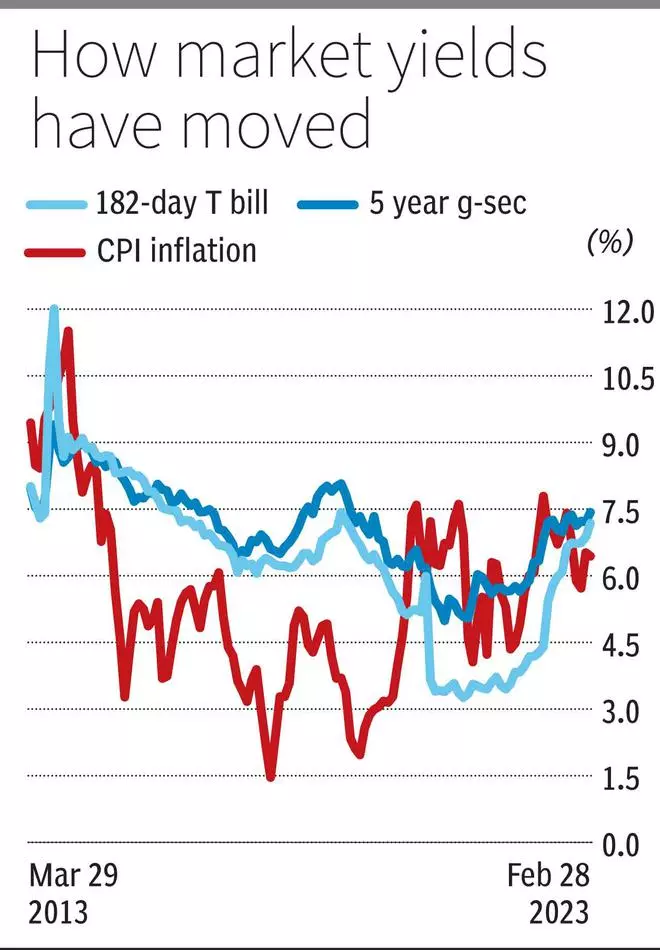

The accompanying desk tells you that each choices have comfortably overwhelmed CPI inflation, in 9 of the final ten years. However can they proceed to take action sooner or later? In resetting quarterly charges on the PPF, the federal government strives for a 25 foundation factors unfold over the prevailing yield on the 5-year Authorities of India bond (g-sec).

Within the final ten years, the market yield on the 5-year g-sec has swung between a low of 5 per cent (July 2020) and a excessive of 9.4 per cent (August 2013), averaging 7.1 per cent. However charges on PPF haven’t been allowed to fall under 7 per cent even when market yields have tumbled. There was delayed catch-up when markets yields have spiked sharply. Internet-net, given the peg to 5-year g-secs, one can anticipate the PPF to higher long-term inflation charges. With investments in market-linked devices, EPF is on shakier floor in delivering its present 8 per cent plus return. However with the fund making fairness allocations, a 7 per cent return shouldn’t be a problem.

Can the tax-free standing of EPF and PPF change in future? As the federal government curbs the tax break (on curiosity) by capping the annual funding in PPF account at ₹1.5 lakh, PPF curiosity is unlikely to show taxable. Within the case of EPF, the curiosity on worker contributions of over ₹2.5 lakh a yr has already been made taxable a few years in the past. Traders can thus make investments a sum of ₹1.5 lakh in PPF and ₹2.5 lakh in EPF yearly for an inflation-beating return. Do word that each choices lock in your cash for the long term. However the 15-year PPF account permits partial withdrawals after 7 years and the EPF permits advances for particular functions.

NPS for debt

Most people affiliate the Nationwide Pension System with fairness investments for retirement. However the NPS presents flexibility to allocate to both equities (E) or company bonds (C) or authorities bonds (G). It presents each a Tier 1 (with lock-in) and Tier 2 account (with out lock-in). So, buyers can use NPS as a pure debt funding automobile too.

NPS managers make investments solely in highly-rated company bonds with a 3-year plus tenure below C and g-secs with medium to lengthy maturity below G. Because the NPS administration charge is simply 3-9 foundation factors and it focusses on medium-long length, returns on the C and G choices of NPS Tier 1 have often overwhelmed each debt mutual funds and choices like FDs. Within the final ten years, consisting of each falling and rising charges, completely different NPS managers have delivered a CAGR of 8.4-9 per cent on the company bond plan and 8-8.5 per cent on the g-sec plan.

Within the Tier 1 account, which is a retirement automobile, last maturity proceeds are usually not topic to tax. Nevertheless, 40 per cent of your last payout must be invested in an annuity, the revenue from which is taxable. This aside, the one adverse with NPS Tier 1 is the requirement to lock in your cash till age 58. Untimely withdrawals are allowed, however capped at 25 per cent. However in case you worth anytime liquidity, you may discover the NPS Tier 2 account the place you may make investments and withdraw at any time, whereas having fun with an identical return at a low charge. Tier 2 doesn’t supply any tax breaks and your returns shall be taxed at slab charges. Nonetheless, it’s a good high-yield choice to discover.

Discover SDLs and FRBs

Till just lately, Indian buyers who needed to personal Central authorities securities (g-secs) or State Growth Loans (SDLs) needed to route their investments through mutual funds, insurance coverage firms or provident funds and undergo a dent to their returns from the charges and prices charged by these intermediaries. However the creation of the RBI Retail Direct Gilt account (you may open this account right here has given you direct entry to the weekly auctions in g-secs and SDLs, with none charges or commissions.

With the opening of an RBI RDG account, you get direct entry to the retail quota weekly auctions of g-secs and SDLs by RBI. This will open up two high-yield choices for a retail investor. One, you get to take part in month-to-month SDL auctions by State governments for tenures starting from 2 to 30 years. Current tranches of SDLs fetched a 7.5 per cent yield for 3-5 years and seven.7-7.8 per cent for 10-year plus. However there have been events previously yr when SDLs provided yields of 8-8.25 per cent for 10 years. SDLs rating excessive on capital security as they’re managed by RBI and backed by escrow preparations.

Two, you may as well look out for the occasional auctions of GOI floating price bonds (FRBs). The curiosity on these bonds, paid half yearly, is reset each 6 months by RBI based mostly on the motion within the 182-day treasury invoice yield. Over a decade, the yield on the 182-day t-bill has averaged 6.4 per cent, hitting a excessive of 12 per cent and a low of three.2 per cent. T-bill yields are extremely delicate to adjustments in market liquidity and RBI’s anticipated price actions.

Due to this fact, when short-term yields out there spike, charges on FRBs routinely rise. With price hikes previously yr, for example, the yield on the 182-day t-bill has spiked from 4.2 per cent to 7.3 per cent now. This has seen RBI sharply peg up the rates of interest on FRBs. FRB 2033 has seen its coupon reset from 4.6 per cent in March 2022, to eight.51 per cent now. FRB 2028 has seen its price reset from 4.3 per cent to 7.01 per cent in a yr. To money in on the FRB alternative, you should monitor GOI’s occasional auctions of FRBs and confirm the unfold provided on the tranche you’re shopping for. Earlier tranches of 10-year FRBs provided a 122-basis level unfold over the 182-day t-bills, current tranches provided 98 foundation factors.

For floating charges, retail buyers may also purchase GOI floating price financial savings bonds 2020 from main banks. The rate of interest on this 7-year bond is about at a 35-basis level unfold over the prevailing rate of interest on the Nationwide Financial savings Certificates or NSC. Although the NSC is meant to be pegged to g-sec yields, it had not matched market yields in current occasions. This has been corrected for the April -June 2023 interval, with NSC now providing 7.7 per cent. Consequently, the curiosity on these floating price bonds shall be 8.05 per cent from July 1, making them a pretty choice.

Effectively-timed FDs

Fastened deposits from banks and NBFCs usually earn a foul identify for failing to beat inflation. However pursuing an lively technique with FDs can get you to constructive actual returns too, in case you time your investments to the speed cycle highs. You might lock into cumulative FDs for 3-years-plus when charges exceed 8 per cent and maintain to very quick tenures once they drop under 6 per cent. At the moment, with a scramble for deposits, some small finance banks and NBFCs (Shriram Finance, Jana SFB, Equitas SFB) are providing 8-8.5 per cent returns on FDs of two to 3-year tenures. Control the Protected Investing web page in Portfolio to trace charges.

Excessive yield bonds and debt funds

Within the bond markets, greater than within the inventory market, a excessive return at all times goes hand in hand with excessive danger to your principal. However excessive rate of interest phases generally provide the alternative to earn engaging yields with out taking up outsized credit score dangers.

With 5 g-secs as we speak providing 7.4 per cent, extremely rated company bonds can get you to a near-8 per cent yield. At the moment, as per GoldenPi, AAA-rated Indiagrid Belief NCDs maturing in Could 2031 supply 7.9 per cent, HDFC Credila bonds maturing in June 2024 supply 7.76 per cent and Bajaj Finance September 2024 NCDs fetch you 7.66 per cent. With many retail bond platforms up and operating, accessing such bonds is not tough. Listed NCDs take pleasure in barely higher tax remedy than different choices, with curiosity taxed at slab charges, however capital positive aspects having fun with 10 per cent tax after a yr. However for direct buyers, juggling tenure, yield and credit score danger is usually a problem. With many bonds privately positioned, the minimal ticket measurement of ₹10 lakh is usually a deterrent.

Company bond, credit score danger and medium length mutual funds let you personal a diversified portfolio of bonds chosen by an expert. Aside from their present portfolio Yield-to-maturity (YTM), you should choose such funds based mostly on their asset measurement, portfolio composition, low focus and aggressive expense ratio. Within the company bond section, Kotak and Aditya Birla Company Bond Fund with newest declared YTMs at 8 per cent and within the credit score danger section, ICICI Pru and HDFC Credit score Danger with YTMs at 8.7 and 9 per cent seem good decisions.

#make investments #debt #choices #excessive #inflation