All good issues have to return to an finish. Nicely, that’s exactly what dwelling mortgage debtors should be experiencing over the previous 18 months. After having fun with record-low charges from early 2020 by way of until late 2021 and early 2022, when curiosity on dwelling loans was at a 15-year backside, issues have modified course.

As a response to staggeringly excessive inflation, the Reserve Financial institution of India (RBI) hiked rates of interest by 250 foundation factors from June 2022, over the following yr or so.

Dwelling mortgage rates of interest soared — from a low of 6.7 per cent to 9.5-10 per cent — leading to large will increase in EMIs (Equated Month-to-month Instalments) for debtors.

On condition that inflation has been on a downtrend, and with international tightening additionally coming to an finish, rates of interest might be nearing their peak in India. The RBI itself has been in pause mode for the previous few financial insurance policies. Nonetheless, a fee lower should still be many quarters away.

As many of the banks and non-banking finance firms (NBFCs) would have transmitted a lot of the speed hikes to clients, it could be a very good time to assessment for those who can ease your EMI burden.

For one, for those who discover your financial institution charging you greater than another establishment, you need to take into account alternate options resembling a stability switch to that establishment. However earlier than you shift your mortgage elsewhere by way of stability switch, it could be a good suggestion to get a very good grip on the method, fees concerned and the cost-benefit payoffs earlier than making the transfer. It’s also vital to grasp how charges are set within the floating fee regime so that you can take a nuanced name. Right here’s extra on the when and the way of stability switch.

Fee regimes

We’ve mounted and floating rates of interest accessible on loans. Mounted rates of interest on dwelling loans can value 150-200 foundation factors (generally even larger) greater than floating fee ones.

Nonetheless, most dwelling loans at the moment are on a floating fee regime.

The RBI launched the MCLR (Marginal Value of Funds Primarily based Lending Fee) in 2016, which changed the bottom fee system that prevailed until then.

Now, this MCLR system continues to be accessible.. Because the identify suggests, the MCLR will depend on the marginal value of funds of the financial institution or NBFC. Moreover, it’s depending on components such because the financial institution’s value construction, G-Sec yields, liquidity within the banking system, working prices, money reserve ratio necessities, and so forth. It’s an inside benchmark set by the lending establishment itself.

A margin is added to this MCLR and charged to the house mortgage borrower. At any time when rates of interest modified, MCLR additionally modified. However the transmission often takes six months and even one yr at occasions, as there are components aside from the repo itself that decide the speed.

Moreover, MCLR isn’t very clear as arriving on the closing fee will not be a simple train, and retail debtors is probably not ready perceive it readily.

To beat these shortcomings, the RBI got here up with an exterior benchmark regime to find out rates of interest. The RLLR (Repo Linked Lending Fee) was launched in 2019 and linked on to the repo fee. Banks then added a margin (credit score danger premium and so forth) to the repo fee. So, it grew to become simpler for debtors to get a way of the rates of interest charged.

And provided that charges needed to be reset rapidly after a financial coverage resolution on growing or lowering rates of interest, the reset occurs nearly each quarter.

After all, RLLR cuts each methods — when rates of interest fall, debtors get to take pleasure in the advantages inside the subsequent quarter, however rising charges would imply paying larger EMIs from the reset interval.

Usually, bankers cost the repo fee plus one other 250-350 foundation factors, relying on the mortgage dimension, tenor, credit score rating of the borrower, amongst different components.

So, at the moment repo fee of 6.5 per cent, banks cost 9-10 per cent. Some banks and NBFCs go as much as 10.25-10.5 per cent.

Retail debtors could be higher off with RLLR-based loans for essentially the most half, if they don’t thoughts the occasional volatility in charges.

Easing EMIs by way of stability switch

When charges are elevated, usually, banks improve the tenor of the mortgage in order that your EMI stays the identical. It’s essential to negotiate together with your current financial institution or NBFC to see if you may get a greater deal. If the establishment is unrelenting, you’ll be able to take into account switching.

Earlier than switching out, it’s essential to fulfill some primary eligibility standards for a stability switch. Some banks and NBFCs insist in your having serviced not less than 12-24 months of EMI together with your earlier lending establishment. Then, most want financing solely ready-to-move-in homes or properties the place possession is taken in case of a stability switch.

These are other than the wage eligibility, credit score rating and different necessities.

After you make up your thoughts on stability switch, it’s essential to perceive the maths of how a lot you’re prone to save by switching lenders, to take an knowledgeable name.

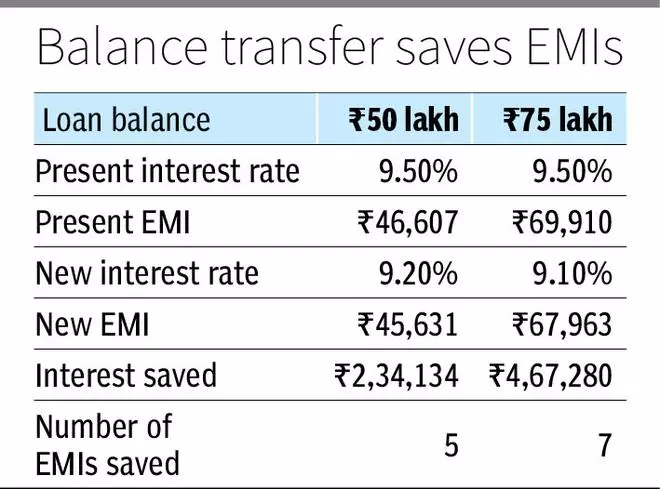

For instance, if in case you have a mortgage stability of ₹75 lakh and a remaining tenor of 20 years, your EMI at 9.5 per cent could be ₹69,910. However for those who go for a stability switch and your new lender chooses to provide you a horny provide of 9.1 per cent, you’ll save some huge cash. Your new lender might provide higher phrases attributable to your improved credit score rating or higher earnings capability and robust reimbursement file or simply as a way to draw new enterprise.

Within the above case, your new EMI will likely be ₹67,963. Over a 20-year interval, you’ll save ₹4,67,280, which interprets to round 7 EMIs. So, you’ll repay your mortgage seven months sooner than for those who had stayed together with your earlier lender.

Larger the discount in rate of interest, the higher your financial savings. Many lenders, resembling ICICI Financial institution and State Financial institution of India are providing decrease charges with smaller mark-ups over the repo until December 31 of this yr.

It will make sense so that you can change loans while you get 25 to 50 foundation factors decrease rates of interest. If charges do begin to decline over center or late 2024, you’ll profit from further fall in curiosity.

Being aware of fees

If you’re on a set curiosity regime, switching to a brand new lender can certainly be fairly costly. Your current lender can cost 2-4 per cent of the excellent mortgage quantity for prepayment.

However when you’re on a floating fee regime, you’ll be able to change to a different lender with none prepayment fees as RBI expressly prohibits levy of prepayment fees on floating fee loans.

Nonetheless, there are lots of different fees that you’ll have to incur whereas making a stability switch.

The primary is the processing payment charged by all banks and NBFCs. Most non-public banks cost about 0.5 per cent as processing payment. Some public sector banks cost nothing, whereas others have zero payment for ready-to-move-in homes and stability transfers. New-age banks and a few NBFCs may cost as much as 3 per cent as processing payment.

Nonetheless, these are acknowledged numbers on their web sites. You possibly can go to these banks or NBFCs and work out a significantly better deal. Primarily based in your negotiation, you’ll be able to cut back and even eliminate processing fees.

Authorized and technical evaluation fees come subsequent and will vary from ₹5,000 to ₹20,000. However, right here once more, some banks embody these within the processing payment, and so you’ll be able to negotiate more durable as there would have been a authorized opinion taken even whereas making use of to your present lender.

Then there’s the memorandum of deposit of title deed (MODT). It signifies that you’ve handed over the property’s paperwork to the brand new lender. This deed must be registered. MODT fees additionally vary at 0.1-0.2 per cent of the mortgage quantity and will not be negotiable. They fluctuate from State to State. Some States have a flat payment or proportion of mortgage quantity in the identical vary talked about earlier for mortgage of title deed (the equal of MODT).

Franking fees are additionally incurred. The property sale doc and the mortgage settlement need to stamped or franked on the sub-registrar’s workplace. These fees are levied by the respective State governments. The costs usually vary at 0.1-0.2 per cent of your mortgage quantity and are paid whereas altering lenders. Franking fees are non-negotiable.

For a ₹75-lakh mortgage stability switch, you can find yourself paying ₹62,500 as fees beneath numerous heads. By negotiating exhausting on course of and authorized charges, you’ll be able to deliver it down considerably.

Regardless of these fees, you’ll nonetheless be saving a tidy sum after the stability switch. (see tables)

All these stability switch gives are for regular dwelling loans that debtors avail. But when they want to transfer their mortgage balances to a different lender with overdraft options, then the rates of interest relevant could be larger to the tune of 0.3-0.5 per cent.

#Scale back #Dwelling #Mortgage #Burden