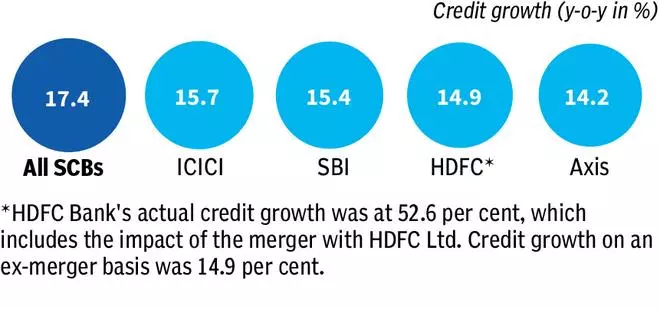

ICICI and SBI shine in credit score development

The credit score development for all Scheduled Business Banks (SCBs) mixed got here in at 17.4 per cent YoY in Q1 FY25. Whereas all 4 banks in contrast right here reported wholesome credit score development, it was ICICI and SBI that got here nearer.

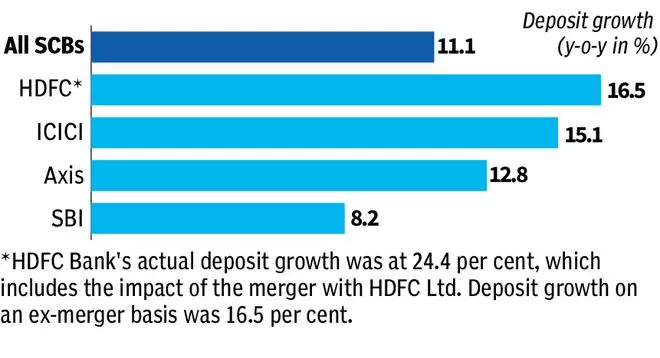

SBI lags in deposit development

HDFC, ICICI and Axis outperformed system degree deposit development, whereas SBI lagged behind.

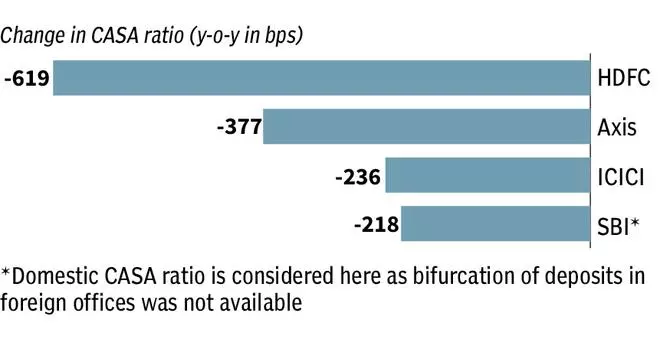

CASA ratios shrink

All 4 banks discovered it tough to mobilise the low-cost CASA deposits (Present Account Financial savings Account) this quarter.

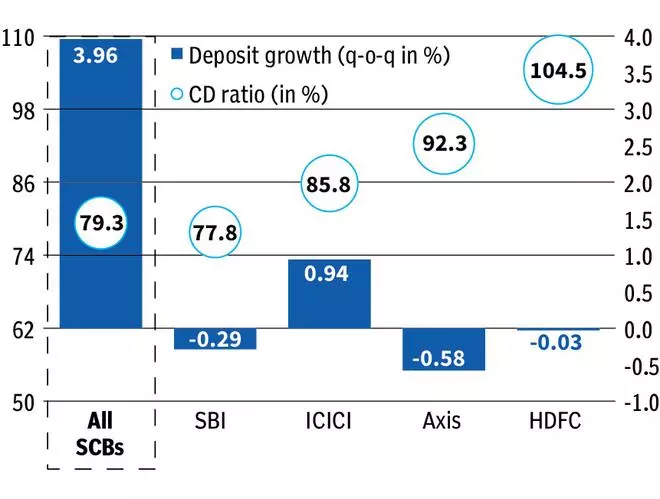

SBI’s CD ratio offers consolation

Whereas there’s demand for credit score, banks have had a tough time gleaning incremental deposits, with family financial savings more and more turning to capital markets. And it confirmed of their overheated CD ratios (Credit score Deposit ratio). Nevertheless, SBI stands out.

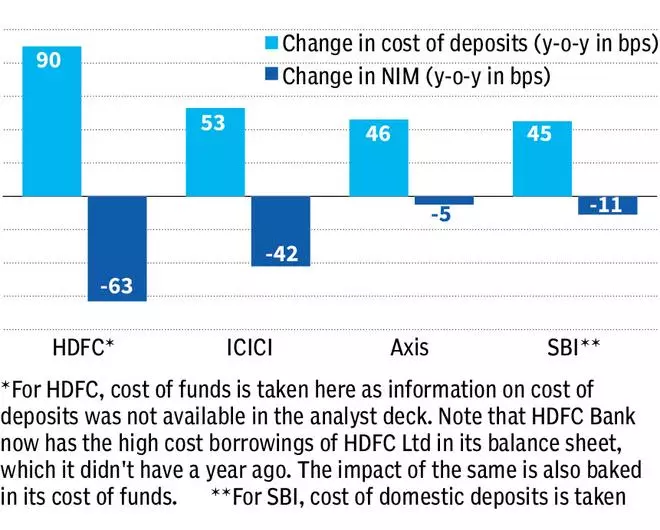

Deposits acquired costly

As deposits acquired scarce, banks ramped up deposit charges. Because of this, their NIMs (Web Curiosity Margin) bore the brunt. However, Axis and SBI have tackled the NIM compression neatly.

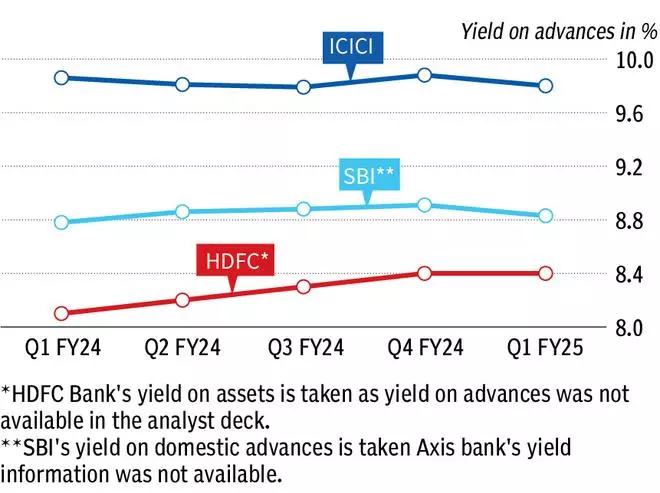

Yields tapering

One other issue that’s inflicting NIM compression is that the yields on advances are tapering from the peaks of This autumn FY24. HDFC’s has stayed flat although.

Notice: Mixed information of all SCBs taken from RBI DBIE

#Prime #Banks #Fared #Quarter