At this juncture, a monetary and non-controlling stake buy by a bigger and worthwhile operator has raised a number of questions. The inventory has gained 30 per cent within the final week and is buying and selling at a premium valuation of 15 instances FY26 EV/EBITDA, which is corresponding to giant cement operators. We suggest that traders maintain on to India Cements stake as monetary, administration and strategic outlook bears a constructive bias regardless of a non-definitive outlook.

Operational headwinds

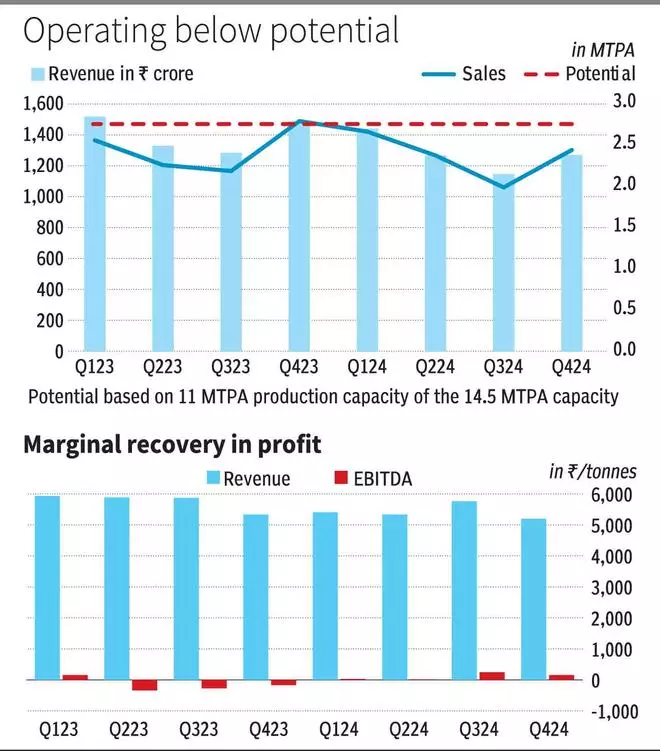

On a consolidated foundation, India Cements reported a blended EBITDA per tonne of ₹105 in FY24, recovering from the lack of ₹146 per tonne in FY23. Whereas this will likely appear constructive, the corporate often reported an EBITDA per tonne of ₹900-1000 per tonne as just lately as FY20-21. Decrease utilisation, greater value of manufacturing in comparison with realisations have been cited as the primary causes for the decline.

The capability utilisation recovered from 53 per cent in Q3FY24 to 61 per cent in Q4FY24, which can also be decrease than the 75 per cent India Cements operated earlier in FY20-21. In comparison with 11 mtpa each year potential manufacturing that may be anticipated, the corporate delivered solely 9.5 mtpa in FY24. The lack of working leverage in a commoditised sector has impacted the margin efficiency for India Cements.

The corporate has been constrained by restricted working capital credit score strains proscribing it to decrease volumes. Older vegetation with a better energy requirement, stretched collectors, lack of market share and excessive debt burden have impacted the corporate’s means to lift further working capital.

Path to restoration

The corporate is disposing non-core property to shore up working capital. It just lately bought a grinding unit with low margins for ₹315 crore and has finished smaller land gross sales to fund working capital and likewise elevate capital for upcoming capex.

It has earmarked ₹500 crore for efficiency-building capex. This features a a waste warmth restoration system at one plant, 1 mtpa fly ash extension at Sankari plant and plans for Raasi plant group. The corporate expects to generate value financial savings of ₹150-175 per tonne with the plans by FY26 and extra gross sales quantity.

On the commodity value entrance, energy and logistics prices have come off their highs in FY24 by 22 per cent and 9 per cent YoY. At the same time as realisations might face headwinds in southern markets from overcapacity, post-election and post-monsoon pricing might creep upwards. The corporate can look to a interval of higher realisations and decrease value of manufacturing in FY25, if coal and transportation prices maintain on the present stage.

Greater utilisation supported by greater working capital availability, effectivity programme and beneficial commodity costs ought to level to enchancment from the present low margin efficiency for India Cements.

UltraTech funding

The 23 per cent stake buy won’t set off an open supply as per SEBI’s acquisition guidelines. Even UltraTech Cement has referred to as it a non-controlling monetary funding. The acquisition value comes out to $90 per tonne for the 14.5 mtpa capability, which is corresponding to mid-size offers finished within the current previous. UltraTech acquired Kesoram Cements at $80 per tonne (10.8 mtpa capability primarily based in South and Western markets. Ambuja Cements most just lately acquired a South primarily based participant, Penna Cements, with 14 mtpa capability at $89 per tonne.

India Cements is essentially centered on South India — 5 mtpa in Telangana, 6 mtpa in Tamil Nadu, 2.1 mtpa in AP, and 1.5 mtpa in Rajasthan. This could complement UltraTech Cement, which at current solely has 15 per cent publicity to the southern area, if it will probably strike a take care of India Cements promoters.

Investor consideration, which drove the outsized features of 30 per cent this week, can also be focussed on the shareholding sample of India Cements.

India Cements has a major public shareholding and is but to put up robust earnings within the final two years. The promoters maintain 28.42 per cent of which 46.2 per cent is pledged. Aside from UltraTech Cement, different public shareholders maintain 48 per cent of shareholding. Even with a monetary funding which is non-controlling, Ultratech Cement’s vital stake will drive speculative curiosity, which might help the inventory value above its intrinsic worth within the medium time period. Given scope for strategic developments, traders can proceed to carry the shares.

#India #CementsWhat #traders #put up #Ultratech #stake #purchase