Right here, we construct on the argument and assess the market valuations assigned to US enterprise vis-à-vis their pipelines to establish over- or undervalued alternatives.

How we valued the elements

Valuation assigned to India, the US and rising markets, primarily based on respective progress alternatives, are summed as much as arrive on the honest worth within the SOTP methodology of valuation. Inversely, by stripping worth assigned to India and Rising Markets (EMs) (by means of peer multiples), one can decide the worth being bestowed on the remaining US enterprise.

Corporations centered solely on Indian markets (Mankind, Eris, Abbott India and Sanofi India) are at the moment buying and selling at a variety of 18-36 instances EV/EBITDA (trailing) with a mean of 24 instances. This valuation is on account of ‘branded’ nature of the Indian market with pricing energy, until interrupted by NLEM (Nationwide Checklist of Important Medicines). .

We have now assigned 20-22 instances EV/EBITDA to Indian companies (a 10-20 per cent low cost to common). The a number of is then utilized to Indian phase’s EBITDA contribution. We have now assumed Indian EBITDA margin to be 100 bps greater than firm EBITDA margin. These assumptions are directional and will range inside firms.

The opposite two companies consisting of rising pharma markets gross sales and API enterprise is valued at 12 instances and 10 instances respectively and EBITDA margin to be decrease than firm common by 100 bps contemplating volatility and non-core operations. Stripping out India and EM Enterprise worth (EV) from consolidated EV, the EV assigned to US phase and therefore the EV/EBITDA of the phase could be implied.

The resultant US enterprise metric, EV/EBITDA, is then in comparison with US friends — both generics or innovators — primarily based on the pipeline product mixture of the businesses. Corporations working primarily in US generics (Aurobindo from India, Teva, Perrigo, Viatris and Hikma) commerce at a variety of 7-15 instances EV/EBITDA (trailing) with a mean of 10 instances. The fixed value erosion of US generics is properly mirrored within the valuation vary.

On the different finish of the spectrum are Innovator firms that commerce at 10-30 instances EV/EBITDA, which relies on the patent cliff timeline, portfolio in ramping stage and pipeline expectations. Novo Nordisk (29 instances EV/EBITDA) and AstraZeneca (22 instances) are buying and selling at a premium, in comparison with Merck or Roche (12-15 instances vary). Pfizer and Sanofi (the MNC) with weakly perceived pipeline changing patent losses are buying and selling at 6-9 instances EV/EBITDA.

Primarily based on the above assumptions, here’s what our evaluation of the valuation of the US enterprise of 5 Indian pharma firms reveals:

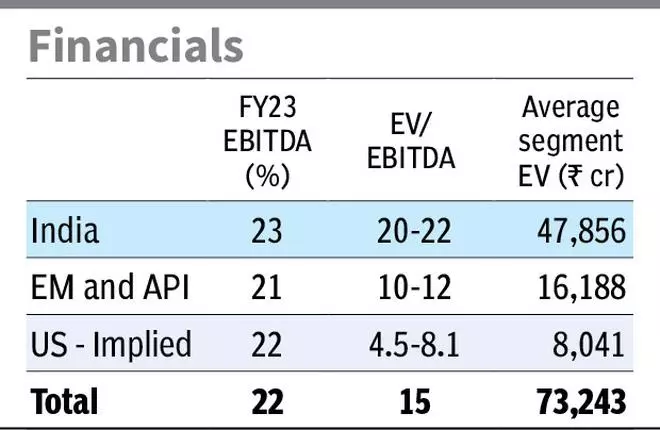

Cipla: Undervalued, however overhang from plant points

Cipla’s implied valuation for US enterprise could also be within the vary of 4.5-8.1 instances EV/EBITDA, which is under the benchmark. US enterprise delivered 17 per cent CAGR progress in previous 5 years in comparison with India’s 11 per cent CAGR progress at Cipla. Even ignoring the sturdy progress (ascribed to one-time gRevlimid bump-up in FY23), the sturdy pipeline makes the case for valuing Cipla’s US enterprise greater, with plant standing because the spoiler.

Together with two respiratory product launches, two peptide launches and gRevlimid launch have boosted US efficiency. The pipeline consists of 5 respiratory property of which three have been filed, one complicated generic and 4 peptide injectables. The respiratory pipeline consists of gAdvair with finish market gross sales of above $700 million, regardless of three generic launches up to now. The general pipeline falls on the upper finish of complexity spectrum, which means a decrease than ‘plain generics’ degree of abrasion and better margins. This could assist Cipla’s US phase valuation within the 10-12 instances EV/EBITDA vary that speciality generic producers command, together with Perrigo.

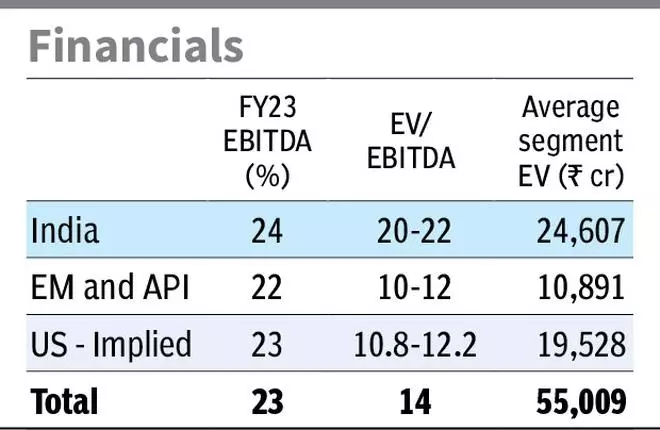

Dr Reddy’s and Zydus Lifesciences: Pretty valued

Dr Reddy’s

Dr Reddy’s has been a US-centric enterprise together with honest contribution from EMs, primarily Russia and CIS nations. Implied US enterprise valuations vary 7.5-8.4 instances EV/EBITDA which, in our view, is honest, contemplating the pipeline.

Dr Reddy’s 180-day exclusivity window, in an already profitable gRevlimid alternative, might shut in Q4FY23. However post-exclusivity it ought to nonetheless generate enough money flows in FY24. The corporate goals to launch 25 merchandise in FY24 (launched 25 in FY23). The launch quantity is barely enough to offset the anticipated annual erosion of 8 per cent within the base portfolio, which is now round $1.2 billion per yr. If the corporate manages to reinforce worth added merchandise (just like gNexavar, gVasopressin final yr) in launch-mix, it could possess a good likelihood of reporting progress within the US.

Dr Reddy’s has a powerful OTC presence even within the US, which it intends to increase from 4 to fifteen within the subsequent few years. Cross-leveraging its biosimilar base, at the moment marketed in EM primarily, is below manner. One partnered product is about to launch within the US and yet another is anticipated to be filed A number of extra biosimilars are within the pipeline.

The well-rounded US generics technique of Dr.Reddy’s — numbers to offset erosion and sophisticated merchandise to safe progress — matches its implied valuation (8 instances EV/EBITDA). This has advanced after the corporate wrote off its proprietary growth plan for US markets and selected the safer method.

Zydus Lifesciences

Zydus’ US enterprise trades at 11-12 instances EV/EBITDA. By the way, the phase outlook can be just like Dr.Reddy’s: an entire lot of easy generic launches together with a number of complicated launches. However the firm has a background in unveiling complicated restricted competitors merchandise repeatedly, which explains the slight premium to Dr.Reddy’s. Present combine consists of Asacol HD, gRevlimid and Topiramate, which could be labeled as complicated just like the 5 launched in earlier years. However within the present plan, Zydus appears intent on delivering excessive variety of launches (deliberate 30-35 launches per yr) together with complicated merchandise, which ought to comfortably offset the single-digit erosion within the base of $926 million in FY23.

Zydus’ present combine, together with filings for 5 extra complicated launches in subsequent few years, ought to maintain mid-single digit progress in US phase regardless of erosion in base portfolio. With current clearance for its Moraiya facility, the corporate can unlock its complicated product pipeline, together with transdermal merchandise alongside a brand new strong dosages facility to assist the excessive launch plan

Zydus additionally bears a powerful New Chemical Entity (NCE) optionality, regardless that not included in valuation. The corporate’s in-house product, Saroglitazar, is below Section II(b)/III medical trials within the US for PBC (main biliary cholangitis). Saroglitazar is a number one driver in India, accepted for NAFLD and NASH — indications associated to infected liver situations.

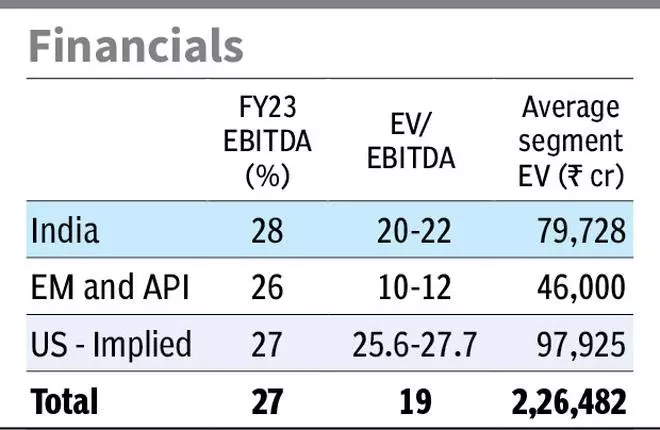

Solar Pharma: US Valuations akin to innovator enterprise

:

Assuming India valuation vary of 20-22 instances EV/EBITDA, Solar Pharma’s US phase’s implied valuation ranges 26-28 instances EV/EBITDA. Even assigning 25 per cent premium to multiples in India, EM and different enterprise, on account of market chief standing, the implied EV/EBITDA vary of US descends solely to 20-22 instances EV/EBITDA.

This valuation vary of 20-30 instances is utilized to innovator firms of their up-cycle stage. World speciality revenues (largely from the US) of Solar Pharma account for a mean of 75 per cent of US gross sales, excluding Taro in FY23, and are rising at 26 per cent YoY. That is double the US income progress price in FY23. This means that the valuation vary and the income contribution are in line and pointing in the direction of a excessive speciality combine, which justifies the valuation vary

Even inside the ‘innovator’ bracket, the higher finish of the valuation vary could be attributed to the ramping stage of the portfolio and powerful alternative worth within the pipeline. The present speciality portfolio is led by Ilumya (accepted for Psoriasis), Cequa (dry eye illness), Winlevi (pimples) together with Odomzo, Levulan, and Absorica. The most important Ilumya is anticipated to achieve peak gross sales of $500-700 million within the subsequent two years.

The pipeline, then again, is led by deuruxolitinib, a best-in-class asset for alopecia remedy, which has cleared Section III stage and purchased as a part of Live performance Pharma for $576 million. The asset although has confronted SAE (critical hostile occasion) in additional trials not too long ago however is just not anticipated to be a serious obstacle. Ilumya can be present process Section 3 trials for Psoriatic arthritis. The opposite pipeline consists of property for Atopic dermatitis (Section 2), ache (Section 2), and even a GLP asset for diabetes (Section 1) which is most profitable pathway in diabetes at the moment.

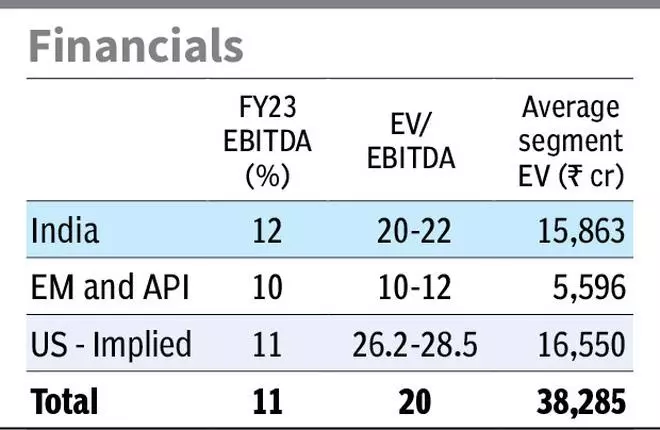

Lupin: Robust expectations drive overvaluation

Lupin’s US enterprise bears implied valuation vary of 26-28 instances EV/EBITDA, which is within the overvalued vary for the complicated generics pipeline of Lupin.

On the present juncture after reporting lowest gross sales progress amongst friends in final 5 years and lowest EBITDA margins sturdy restoration is anticipated. gSpiriva, a respiratory asset with finish market gross sales at $700 million and a three-player market, is anticipated in H1FY24 (after a number of rounds of delay).

Additionally, gDiazepam gel, gNascobar spray, gDarunavir and gBromfenac, anticipated in FY24, ought to assist rebound flagging gross sales within the US. Equally the pipeline additional down can veer in the direction of excessive worth injectables and inhalation property with R&D focussed on such property. A biosimilar approval and launch can be anticipated for Lupin in FY24-25.

Exterior of pipeline assumptions, restoration of margins additionally appears to be constructed into the present overvaluation. Lupin’s administration expects near 300 bps enchancment in EBITDA margins by FY24 to fifteen per cent and additional enchancment to 18 per cent in FY25, in comparison with 12 per cent at the moment in FY23. The sturdy launch plan and ongoing value financial savings plan do assist assumption of margin restoration, however the valuation expectation primarily based on the identical could be stretched.

What traders ought to be careful for

Given the over/below valuation, traders want a calibrated method to place oneself within the shares. In case of Cipla, the way in which crops regulatory standing unravels could have a bearing on the inventory. In the meantime, de-risking launch schedule by transferring merchandise or further competitors in gAdvair will assist or harm the valuations respectively. Dr Reddy’s and Zydus Lifesciences, although pretty valued at the moment are heading in the direction of a glass ceiling of types.

Because the portfolio dimension will increase to $1.5 – 2 billion a yr, assuming $3-4 million per plain generic launch, the 2 would want 40 launches each year simply to report flat earnings progress in US. This might indicate a excessive regulatory oversight and execution dangers, simply as Aurobindo confronted within the final two years.

Lupin’s overvaluation is driving on sturdy launch schedule to revive earnings progress and in addition to scale-up margins. The pipeline ought to ship on anticipated strains, timing and market share good points smart, to assist the valuations. Delay in product approval, any new plant points or announcement of recent competitors can influence the precarious valuations.

Solar Pharma’s present set of merchandise bought within the US and the pipeline below growth assist the innovator-level valuations for the enterprise. As defined, innovator valuations can swing from single digit to 30 instances as pipeline is exhausted or replenished. Means of Solar to persistently replenish the portfolio pipeline with out straining its financials (in type of outsized acquisitions) is essential to assist the valuations.

#Indian #Pharma #firms #pipelines #justify #valuation #assigned #enterprise