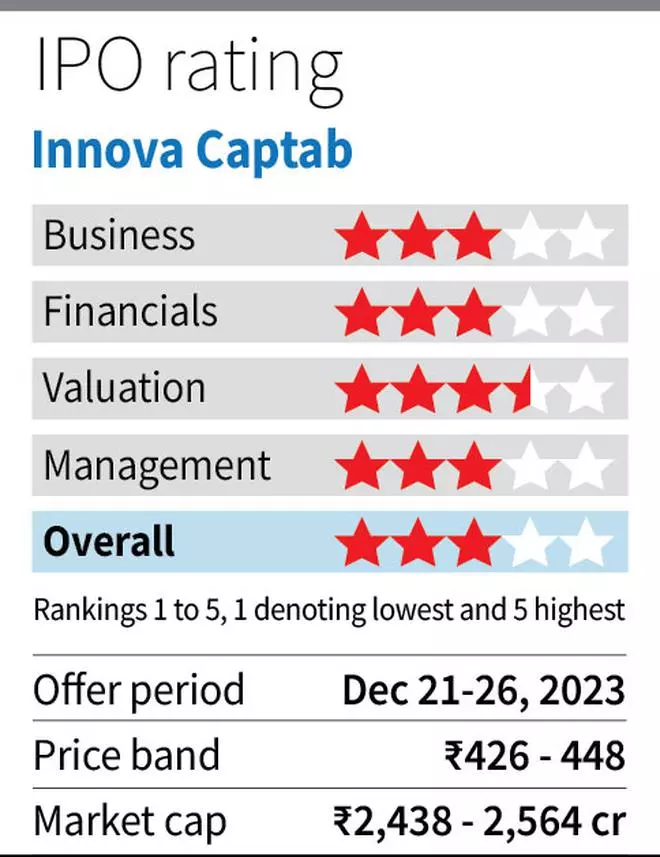

Innova Captab is a CDMO (contract growth and manufacturing organisation) operator that contract-manufactures generic formulations and provides to home pharmaceutical firms advertising them. The IPO (open until December 26) values the corporate at 25 instances FY23 earnings — on a pro-forma foundation, which incorporates earnings from an organization acquired in June ‘23 Given growth in Jammu and synergies from the acquisition, the valuation appears affordable and traders with a long-term outlook can subscribe to the problem.

The provide features a recent concern of ₹320 crore (₹168 crore in the direction of debt and ₹72 crore for working capital) and provide on the market of ₹250 crore. On the increased band of ₹448, the market capitalisation is at ₹2,500 crore.

Innova derived 60 per cent of FY23 revenues (pro-forma) from CDMO operations. The corporate granulates, compresses, coats and prepares the ultimate formulation from APIs bought from third events. Shut to fifteen per cent of revenues is from branded generics of its personal formulations and seven per cent is from exports of branded generics to nations led by Kenya, Afghanistan, and Sri Lanka. The latest Q1FY24 acquisition of Sharon would have contributed 18 per cent to FY23 revenues assuming it was consolidated.

The purchasers embrace the big home pharma firms with which Innova has an extended traction. In FY23, CDMO had 182 prospects and Prime 10 and the highest shopper accounted for 56 and 14 per cent in FY23, indicating a reasonable degree of shopper focus.

Growth of operations

Indian CDMO is a extremely aggressive discipline with Innova gaining a market share of just one per cent in India in FY23 regardless of working from 2006. Within the CDMO division, differentiation is predicated on vary of drug supply capabilities, costing, service points and regulatory and monetary stability.

The corporate’s drug supply capabilities embrace tablets, capsules, ointments, dry powder injectables, and liquid orals. The upcoming Jammu facility will lengthen the aptitude to penem injectables and dry powder inhalation formulations, that are increased up on complexity scale, aside from including to capability in present drug deliveries. The challenge, with an estimated price of ₹350 crore, ought to double the present capability of manufacturing in three years (present internet fastened asset base of ₹300 crore) — one yr for commercialisation and two extra for validation and ramping up of buyer base from new facility. As talked about, a wider basket of drug supply capabilities would differentiate Innova in CDMO markets aside from increased income potential.

Sharon acquisition

Innova acquired Sharon beneath the Insolvency and chapter Code in June 2023. The corporate infused ₹195 crore into the agency which, together with present FD of ₹60 crore, cleared Sharon’s money owed. The goal firm can be into contract manufacturing of formulations, which accounted for ₹120 crore of the ₹193 crore income in FY23. Exports accounted for 75 per cent of complete revenues of Sharon. The corporate manufactures APIs as effectively accounting for the remainder, which can complement Innova because it doesn’t have API capabilities.

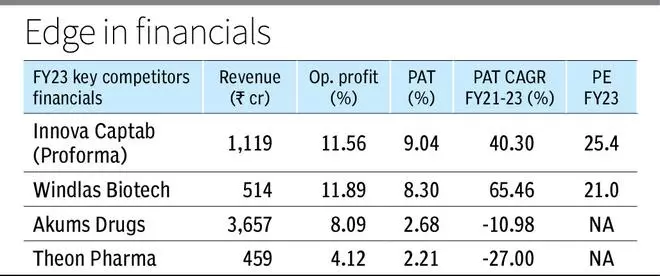

Innova might report increased progress in FY24 as Sharon’s operations normalise, however valuation of 25 instances captures the expansion. It’s the synergies from this acquisition which are the incremental worth addition which might take barely take longer to materialise because it progressively evolves out, from beneath IBC. The synergies will probably be from scale of operations and attainable enchancment in margins to company-wide degree (8 per cent EBITDA margins of Sharon in FY23 in comparison with 12 per cent for Innova). Sharon’s present utilisation at 50 per cent can also be improved to {industry} ranges of 60-70 per cent, including worth.

If the acquisition is built-in meaningfully, Sharon, acquired at near 1x worth to gross sales, ought to be value-accretive to Innova, which has a worth to gross sales of round 2 instances.

Financials and valuation

With Indian pharma itself anticipated to maintain 9-10 per cent annual progress within the subsequent decade, CDMO markets ought to witness the next progress as scope of contract manufacturing will increase. With concentrate on time to market, wider portfolio of merchandise, complicated generics in product portfolio and rising regulatory oversight, organised CDMO, together with Innova, can garner the next market share in comparison with unorganised gamers.

The corporate has industry-leading working margins of 12 per cent in FY23. With Jammu growth and Sharon-related synergies to play out, Innova can maintain increased progress. The corporate has a internet debt to EBITDA of two.9 instances as of June ‘23, which may come right down to 1.5 instances with reimbursement from recent concern proceeds, additional offering consolation to valuations.

#Innova #Captab #IPO #Subscribe