In relation to consuming out, Indians have lapped up Western QSR (Fast Service Restaurant) manufacturers that target pizza, burgers, chicken-based meals in a giant approach.

McDonald’s, KFC, Burger King, Domino’s, Pizza Hut, Subway, and so forth., are credible manufacturers on this area, on condition that a few of them entered India within the late Nineteen Nineties (Domino’s, McDonald’s and Pizza Hut) and early 2000s (Subway and KFC).

Communicate to any administration, and they’re going to cite secular developments of younger inhabitants, rising urbanisation, rising affluence, accelerated shifts in the direction of digitalisation and change in favour of the organised sector for why you need to be bullish.

Nevertheless, for those who transcend these beaten-to-a-pulp phrases, investing in QSR shares isn’t a straightforward meal. Valuations, for one, are costly. Put collectively, the 5 fundamental QSR shares have a market worth of ₹90,000 crore for churning out a meagre ₹650 crore earnings on the again of ₹14,900 odd crore gross sales.

Undoubtedly, the final two-three years have witnessed a surge in curiosity round QSR shares, with the latest pandemic-induced on-line ordering and supply pattern offering a lift. However divergent developments will be seen within the QSR inventory universe in India.

Restaurant Manufacturers Asia, previously Burger King India, is up 113 per cent since its IPO in 2020. The inventory of Devyani Worldwide (a franchisee of KFC and Pizza Hut) surged 135 per cent since IPO in 2021, however positive aspects in Sapphire Meals (one other franchisee of KFC and Pizza Hut) are decrease at 25 per cent since its IPO in the identical 12 months. Amongst Indian QSR firms with lengthy itemizing file, shares of Jubilant FoodWorks (grasp franchisee of Domino’s) are up 13 per cent on a 3-year foundation, whereas Westlife Foodworld (owner-operator of McDonald’s eating places) is up a whopping 2.5 instances in the identical interval.To make higher sense of this area, that you must perceive the important thing dynamics at play for QSR shares. Right here they’re:

Retailer-sales conundrum

Brick-and-mortar eating places depend on bodily shops to rake in income. The 5 main QSR firms collectively function 4,600+ shops. Increasing QSR market alternative and penetration past metros have pushed QSR majors in India to undertake retailer enlargement. For this text, we’re focussing primarily on the India enterprise for prime QSRs as worldwide segments are a lot smaller.

After the Covid-19 disruption, QSR chains continued their retailer additions at a brisk tempo. However establishing shops requires cash. Capex for every retailer ranges between ₹1.3 crore and ₹3.5 crore primarily based on retailer dimension and site. Retailer hire as a share of gross sales ranges 8-15 per cent. Nevertheless, common order worth throughout manufacturers is ₹450-600. Retailer gross sales don’t instantly begin firing on all cylinders from day one. If a retailer doesn’t work, it’s both rationalised or decommissioned (23 by Jubilant and 12 by Sapphire in FY22, as an example).

Retailer depend development doesn’t equal income development for varied causes. Jubilant Foodworks, essentially the most mature QSR play in India, grew retailer depend by 10.3 per cent CAGR in FY20-23 interval, however topline development lagged at 9.2 per cent in the identical interval. Equally, Devyani’s retailer depend grew by 35.4 per cent CAGR whereas income grew by 25.4 per cent CAGR. Nevertheless, some, like Westlife Foodworld, seem to have hit the precise formulation with managed enlargement. Whereas Westlife grew retailer depend by 4 per cent CAGR, gross sales superior by 13.8 per cent CAGR.

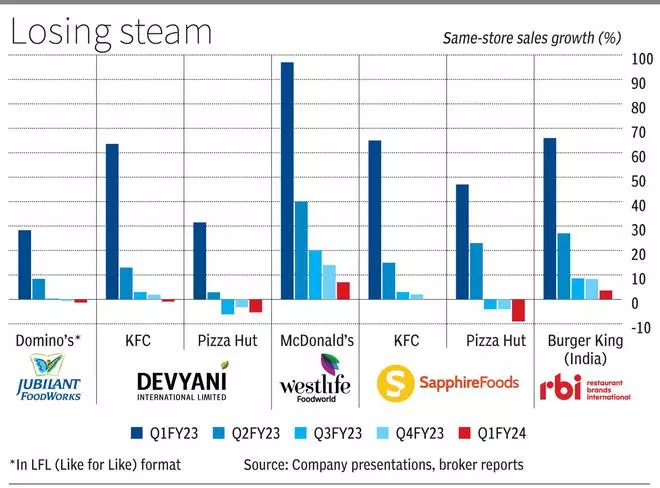

Buyers must also observe {that a} comfortable demand atmosphere can affect retailer gross sales. In Q1 of FY24, same-store gross sales development (SSSG) for many QSR majors has been adverse, deteriorating from already poor charges in This fall of FY23. Buyers exhibit a choice for substantial development in same-store gross sales. When a good portion of an organization’s income development is attributable to the enlargement of recent shops, it might counsel that demand for the corporate’s merchandise is plateauing. This, in flip, implies that minimal future income development ought to be anticipated as soon as the corporate attains saturation by way of whole variety of areas.

Risky margins

Regardless of the passion surrounding the high-growth Western QSR class, the valuation of firms working inside this area may very well hinge upon their margin technique. Gross margins in QSR shares ranges at 65-75 per cent whereas EBITDA margins at 11-23 per cent. Retailer margins are nearer to EBITDA margins. Web revenue margins are decrease (5 to 10 per cent), besides loss-making Restaurant Manufacturers Asia (FY23). Margin enlargement typically is led by working leverage, however what complicates the matter are the risky margins.

The swing in margins could possibly be as a consequence of many causes, comparable to sticky enter price inflation. Price-saving initiatives and pricing actions can solely accomplish that a lot. In truth, typically, QSR chains have to soak up inflation. In FY23, as an example, Jubilant Foodworks’ efficiency was a story of two halves. Submit the competition season, there was sudden deceleration in demand as rampant inflation began exerting strain on discretionary consumption. In a single 12 months, cheese worth elevated 40 per cent, flour worth 28 per cent, hen and paper field costs 30 per cent. In consequence, Jubilant’s working revenue margins — after being at 24 per cent for H1 of FY23 — slipped to 21.5 per cent in Q3 and additional to 19.6 per cent in This fall.

Equally, different QSRs noticed inflation affect. For instance, Devyani’s working revenue margin fell by 100 bps in FY23. In KFC, the primary components are hen, oil, flour and packing materials. Some stabilisation has been seen in them in addition to in greens in Q1 of FY24, serving to working margin discover base round 20 per cent. In case of Sapphire Meals, quarterly working margins slid from 20 per cent plus to 17.5 per cent from Q1 to This fall of FY23. In a latest convention name, Sapphire administration reckoned that demand is anticipated to stay sluggish for a minimum of a 12 months earlier than stabilising, as inflation moderates.

Dietary preferences additionally change, which impacts sure QSRs greater than others. As an illustration, Q2 usually is seasonally the bottom quarter for chicken-based objects. Usually, Shravan/Sawan interval falls on this quarter, the place lots of Hindus flip vegetarian. Additionally, as firms compete in comparable merchandise (burgers and fried hen), the rising share of value-for-money merchandise does pose a threat for margins. Greater salience of low-ticket-value/low-margin merchandise (for e.g. beneath ₹100 price ticket) might carry volumes, however delay retailer payback intervals. Total inflationary developments, not simply enter costs, additionally power shoppers to down-trade from premium-end burgers and pizzas. A altering combine impacts margins. So, investing in QSR shares primarily based on historic margin developments could also be difficult.

E-ating out

Whereas QSRs speak about omni-channel (dine-in, apps, on-line supply, drive-thru, on-the-go) methods, some key adjustments are occurring. On-premise consumption is, after all, returning, however there may be rising proof of incremental events and habit-build in favour of off-premise consuming. For Pizza Hut in India, off-premise gross sales accounted for 56 per cent of the entire gross sales combine in FY23. For Westlife, general contribution of the off-premise enterprise to the topline is 40 per cent (Q1FY24).

The Y-o-Y development of Indian on-line meals supply market within the final three years is 100 per cent. Statistics present the general share of on-line gross sales in meals service business has reached double digits (10.7 per cent) in 2021 vs low single-digit (1.9 per cent) in 2016, in response to Euromonitor. Pre-Covid, this was 4.3 per cent. Customers are actually accustomed to ‘delivery-across-town’ classification, helped by the ever-expanding attain of the supply ecosystem in Tier II/III/IV. As a result of latest pandemic, standalone shops with a robust emphasis on dine-in companies have been disproportionately affected. This might point out a possible shift available in the market in the direction of delivery-centric enterprise fashions, which has a bearing on how QSR firms carry out in future. So, store-led development methods might must be re-calibrated. Near half eating places pay in extra of 20 per cent of every order as fee (gross take fee). Notice premium eating places pay decrease median take charges.

As an illustration, Devyani (KFC and Pizza Hut) has elevated give attention to smaller-sized, delivery-focussed shops vis-à-vis bigger dining-oriented shops in India. To serve on-line deliveries, QSRs will actively put money into cutting-edge know-how to boost digital capabilities, enhance supply effectivity and optimise general operations. Equally, omni-channel technique enabled a discount within the dimension of eating places by 45 per cent for Sapphire (one other operator of KFC and Pizza Hut shops).

The acceleration of the expansion of on-line by way of supply apps has led to prominence for ‘cloud kitchens’ the place meals is ready as ‘made to order’ suiting client style and choice, however costs are nonetheless reasonably priced. Whereas cloud kitchens began to achieve traction approach again in 2015, due to Covid ‘cloud solely’ meals service manufacturers and companies acquired a lift in reputation. The concurrent rise of meals aggregators additionally supported this development.

Whereas cloud kitchens within the on-line playground are robust opponents, lack of bodily model join with the client, low entry obstacles resulting in a crowded ecosystem with excessive mortality fee, and lack of attain outdoors of Tier-I cities are their disadvantages. But when Zomato and Swiggy aggregator ecosystems thrive, buyer join, coupled with subsidised supply prices and reductions/promotions, can pose a risk for QSRs. Insurgent Meals is the biggest cloud kitchen which has displayed profitable scale-up in latest instances. Oblique competitors from aggregators on non-public label meals manufacturers also can enhance rivalry in QSR on-line gross sales section.

Valuations and development expectations

Provided that QSRs are linked to consumption, QSR shares are undoubtedly expensive. In comparison with Nifty 50’s 1-year ahead worth to earnings of twenty-two instances, the ahead PE of QSR shares ranges at 70-100 instances Given the capital-intensive nature of QSRs, even on the EV/EBITDA valuation a number of these shares commerce at 19-34 instances for FY24 and 15-28 instances for FY25, which is dear.

Regardless of muted demand and lower-than-expected new-store openings in Q1 of FY23, firms have retained annual store-opening projection for FY24 (Jubilant: 200-225, Devyani: 275-300, Westlife: 40-45, Sapphire: 130-160 and Restaurant Manufacturers: 50 (India)). These could possibly be in danger.

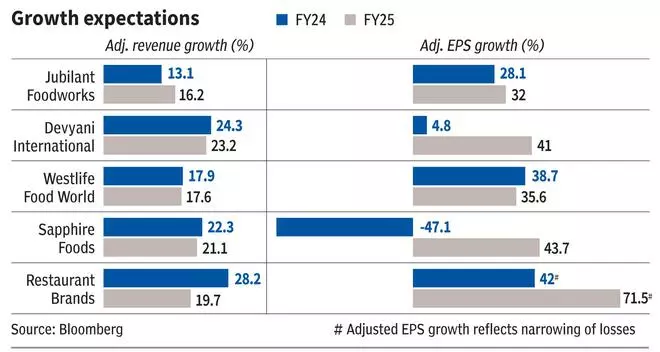

Regardless of Bloomberg consensus estimate cuts to FY24 and FY25 earnings (in comparison with January-2023 projections), QSR shares, viz. (Jubilant & Sapphire, up 19 per cent, Restaurant Manufacturers, 26 per cent, Devyani, 44 per cent and Westlife 46 per cent) have participated within the broader market rally since March 2023 lows.

At the very least within the quick time period, pizza gamers comparable to Jubilant are anticipated to grapple with weak demand, incremental competitors, and rising inflation in dairy. These have pushed analysts to anticipate modest development of their toplines. For pizza and chicken-food gamers (Devyani and Sapphire), these challenges maintain true, together with rise in hen costs, however small worth hikes are anticipated to assist them defend margins whereas rising gross sales. Burger participant Westlife Foodworld has been an outlier of kinds in latest instances, given its sturdy SSSG (same-store gross sales development) when friends have struggled. Fee of maiden dividend by the corporate has additionally been taken as a sign of administration’s confidence about development prospects.

#Investing #Indias #QSR #Shares #Complicated #Recipe