Paytm inventory was among the many worst performers on the bourses this week, due to its administration saying plans to scale down postpaid loans of ticket measurement lower than ₹50,000. The choice is a pre-emptive measure, in line with Paytm, after session with its lending companions, given the current market circumstances and regulatory modifications.

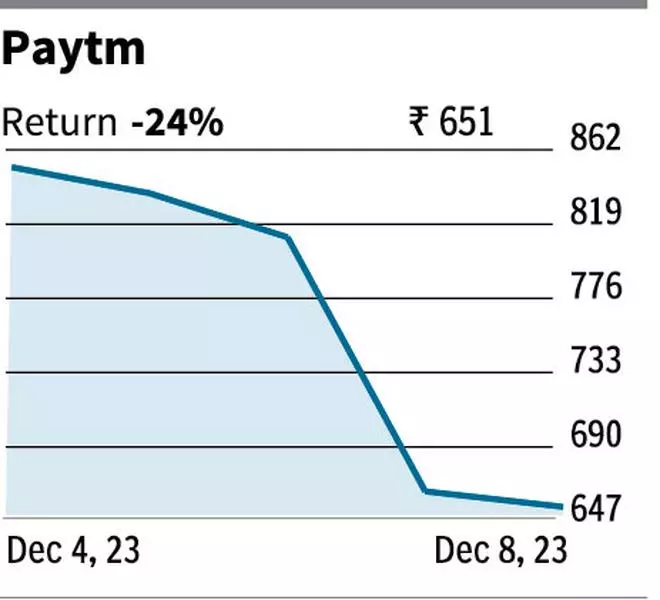

At ₹651.90 a share, the inventory has had some unpredictable swings this yr, particularly after touching a 52-week excessive of ₹998.30 a little bit over a month again. This week’s improvement has not simply elevated the volatility within the inventory worth however has additionally put it in a spot the place traders must carefully watch for a way its mortgage distribution enterprise shapes up.

Small difficulty

A number of weeks again, when the Reserve Financial institution of India jacked up the danger weighted property for unsecured loans, it was anticipated that the section catering to low-ticket unsecured loans will be the most hit. Paytm, which is the most well-liked on this class, might probably be taking the most important hit amongst digital lenders catering to the retail lending house. To make sure, 70–73 per cent of the fintech’s complete mortgage distributed originates within the lower than ₹50,000 loans, or the entry-level private mortgage class.

This section was additionally within the information for steep delinquency ratios (over 5 per cent). At a systemic stage, the RBI has continuously been flagging revolutionary strategies getting used to masks the true image of mortgage high quality on this section. Curiously, for Paytm, the sub ₹50,000 loans is likely one of the greatest segments with least asset high quality points; its NPA on this section was lower than a per cent as per the fintech’s September quarter outcomes.

The postpaid section, as Paytm calls the house, can be the quickest rising bulge for the corporate, accounting for over 55 per cent of complete worth of loans originated. Clearly, it’s the most promising mortgage acquisition engine for the corporate and the quickest rising class, on condition that in September quarter, the postpaid section posted 122 per cent year-on-year progress, means above the higher-ticket-size private loans.

Dangerous timing

The choice to go gradual on small-ticket loans comes simply when the bullishness on Paytm is enhancing. Whereas the corporate nonetheless incurs losses at an EBIDTA (earnings earlier than curiosity, depreciation, and amortisation) stage, EBIDTA adjusted for worker inventory possibility prices has turned constructive since June FY24. Whereas that is barely an correct benchmark to charge one’s monetary efficiency, because it’s in adherence to the projections, it’s working to Paytm benefit. Often, small-ticket loans don’t earn excessive payment revenue and the administration plans to off-set decrease progress on this section by promoting extra of upper bulged private loans and service provider loans.

However since submit paid loans account for a big quantity of loans distributed, their influence on income can’t be dominated out. March FY24 quarter will precisely reveal the hit on revenues.

In the meantime, Paytm Fee Financial institution, an affiliate entity of Paytm, has additionally run into regulatory points. It hasn’t been in a position to onboard new clients for over a yr and, going by information stories, it’s solely by March 2024 that the strictures on the corporate could also be lifted. With a couple of course correction to make, at this level, the draw back dangers outweigh the constructive and Paytm inventory should still be a really dangerous wager to take for many traders.

#Paytm #Caught #Rock #Arduous #Place