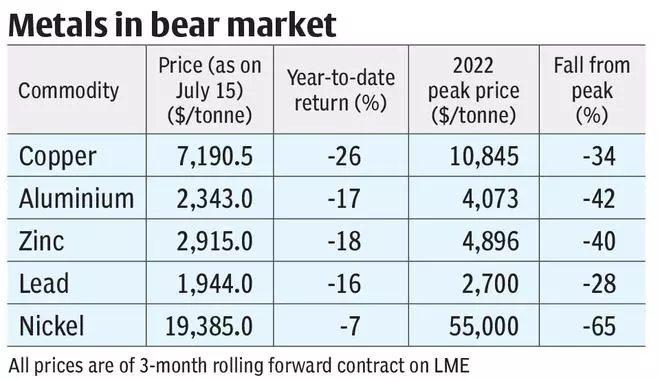

In our yearly outlook printed in early-January when all metallic costs had been persevering with their bull run, we projected that the costs may high out within the first quarter and will see a drop for the remainder of the 12 months. Whereas the value moved according to our expectations, the autumn was so sharp that each one metals have now dropped to the degrees we anticipated them to succeed in solely by the top of 2022.

What saved the bulls going early this 12 months? What led to the sudden change in pattern and the following droop in costs? Will the bears punch extra?

Listed below are our solutions.

Portfolio Podcast | What’s the purpose behind the bottom metals sell-off in current occasions

Struggle-led rally

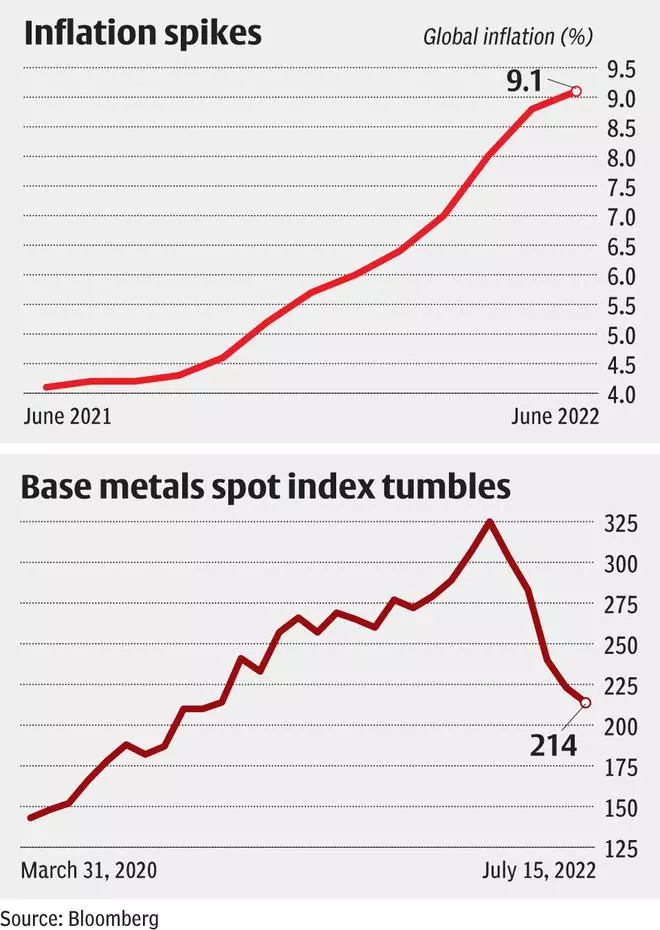

The 12 months 2021 was an ideal one for metals. The costs rallied considerably on the again of provide disruptions attributable to the pandemic, central financial institution liquidity and the financial restoration following easing of lockdowns. The Bloomberg Base Metallic Spot Worth Index was up practically 33 per cent for the 12 months.

In early 2022, expectations of the central banks — particularly the US Fed, embarking on a charge hike cycle after which pulling the plug on liquidity, had been gaining traction. One would anticipate such steps to weigh on asset costs together with metals.

However then, the Russia-Ukraine battle gave the bulls one final push, as provide considerations propped up once more. Metals went on to hit additional highs. At its peak, on March 7, the Bloomberg Base Metallic Spot Worth Index was up 27 per cent year-to-date. Nevertheless, the rally didn’t maintain as a number of headwinds got here to the fore.

Inflation, the Fed, and the greenback

Amongst all, inflation turned a serious level of debate because it began spiking above the higher restrict of central banks. What was regarded as transitory at first, proved in any other case throughout geographies.

International inflation continued to rise in 2022 and hit 9.1 per cent in June, based on Bloomberg information. The US inflation, too, was in an upswing and, notably, hit a four-decade-high 9.1 per cent in June. Equally, Euro space inflation shot as much as 8.6 per cent in June.

So, considerations of inflation staying at elevated ranges nudged central banks, particularly the US Fed, to show hawkish. The coverage modifications within the US are vital for the worldwide financial system and the saying, “When the US sneezes, the world catches chilly,” stays true until date.

Sooner charge hikes had been carried out and the Fed raised the coverage charge from 0.25 per cent in January to 1.75 per cent in June. Consequently, treasury yields shot up from 1.5 per cent by the top of final 12 months to three per cent in June. For the reason that tightening has been faster than anticipated, fears that the Fed would possibly tighten far too rapidly pushing the financial system right into a recession, and hampering demand for commodities, pulled metallic costs down.

On the similar time, investor sentiments weakened, and so they turned to security. The US greenback, being a protected haven, surged, and rising US treasury yields resulted in greater demand for the greenback. The greenback index, now at round 108, has gained practically 13 per cent thus far in 2022. This too hit metallic costs as they’re quoted in {dollars} within the worldwide market.

Recessionary considerations have additionally shifted the narrative for metals to ‘weaker consumption’ somewhat than ‘tight provide’ which dominated within the first quarter of this calendar 12 months.

No development push

The Worldwide Financial Fund (IMF) expects the worldwide development to sluggish considerably in 2022 to three.6 per cent from 6.1 per cent in 2021 as a consequence of the Russia-Ukraine battle.

The IMF expects the financial development charge in China, the world’s greatest producer and shopper of commodities, to be at a a lot decrease 4.4 per cent this 12 months in comparison with 8.1 per cent in 2021. Even when China recovers and the consumption of metallic improves from right here, it might not counterbalance the potential demand drop from the US and Europe as they undergo financial tightening.

Development within the US and Euro space is predicted to drop to three.7 per cent and a couple of.8 per cent in 2022 as in opposition to 5.7 per cent and 5.3 per cent, respectively in 2021, based on the IMF.

Slowdown in main economies like China, the US and Europe means weak demand for base metals and thus, consumption for key commodities is predicted to lag provide in 2022.

The Worldwide Copper Examine Group (ICSG) initiatives the worldwide refined copper steadiness to be at a surplus of 1.42 lakh tonnes in 2022 and the Worldwide Nickel Examine Group (INSG) estimates that the worldwide nickel steadiness might be at a surplus of 67,000 tonnes this 12 months.

Equally, the Worldwide Lead and Zinc Examine Group (ILZSG) expects the demand for result in fall in need of provide by 17,000 tonnes by the top of 2022. Zinc provide is anticipated to be at a deficit of two.92 lakh tonnes. But, zinc was not spared of the commodity market onslaught as they fell together with different non-ferrous metals, probably, on considerations about international development.

Weak financial development is not going to solely impression the demand for base metals, however it could possibly additionally lead to suppressed demand for crude oil, one other key commodity.

Crude uncertainty

As international oil consumption outpaced provide since mid-2020, the costs of crude oil soared. Larger demand led to inventories lowering by a mean 1.4 million barrels per day (MMbpd) between the third quarter of 2020 and first quarter of 2022, based on the Power Data Administration (EIA). However they forecast the inventories to extend by 1.2 MMbpd within the second half of this 12 months as a result of enhance in oil manufacturing and slowing development in consumption. So, EIA expects the typical worth of crude oil, which was at $123 in June, to drop to $97 within the last quarter of 2022.

Nevertheless, there are plenty of uncertainties comparable to how a lot Russian oil will attain the worldwide market within the coming months and the way effectively can the OPEC Plus international locations meet their manufacturing targets.

However, at this juncture, it seems that crude oil may regularly decline within the coming months, as demand is predicted to weaken due to slowing development. A fall in crude oil costs may be good in a manner, as it could possibly assist settle down the inflation.

Outlook

Though the present sell-off in metallic costs may decelerate, the dearth of demand and powerful greenback will proceed to place downward strain. If this occurs, customers of metals as inputs might get some breather from the margin pressures that they’ve been going through. Nevertheless, whereas metallic producers have been making the most of rising commodity costs within the final couple of years, they could see a dent in efficiency within the upcoming quarters.

Chance of a draw back in crude oil costs could be a supportive issue for metallic costs due to the financial savings in power prices which go into the manufacturing of metals.

#selloff #base #metals