The OTA house in India is ready for a good development path for the long run for 2 causes — one, the consumption theme in India, of which journey and tourism is a component, is ready to develop nicely as requirements of residing enhance; two, digitisation and use of OTA apps continues to increase into each nook and nook of the nation, leading to OTA gamers rising quicker than the general journey business.

On the flip aspect, the Indian OTA house is a bit crowded, with extra gamers than what one would see in developed economies. ixigo could be the fourth listed participant on this house, if one consists of MakeMyTrip, which is the business chief in India and is listed within the US. There are a number of unlisted gamers as nicely. Given competitors and corporations investing in development, margins are additionally low. Thus there are pluses in addition to minuses.

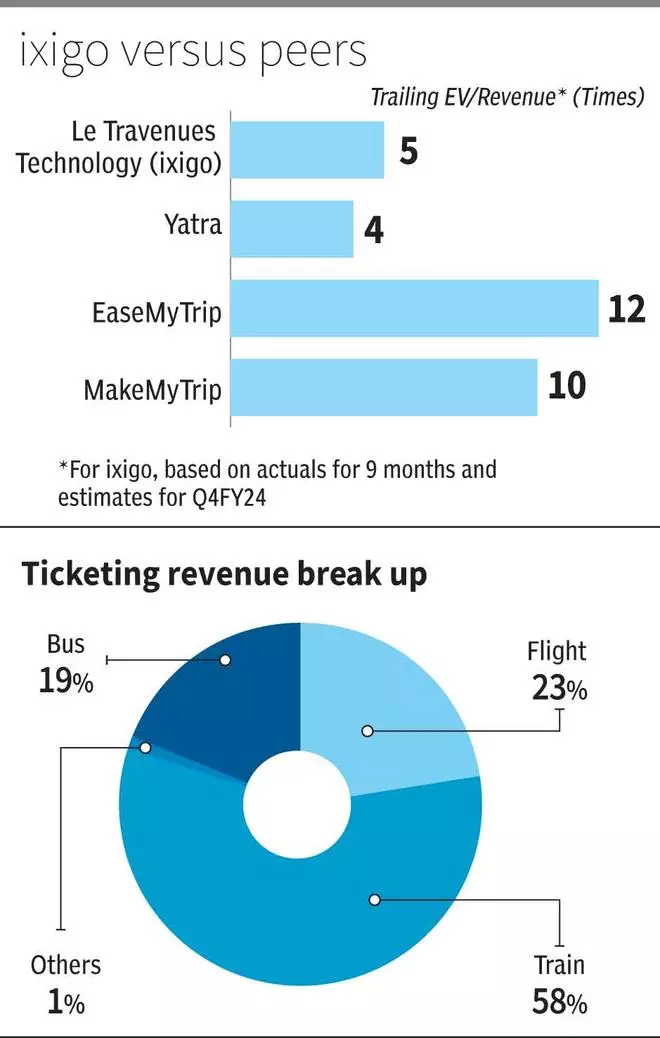

On this backdrop, ixigo IPO hits the road at a valuation of 5 occasions EV/Income. The income right here is estimated FY24 income based mostly on actuals for 9 months and 4Q estimates adjusted for seasonality. The valuation, whereas not low cost, just isn’t extreme both. Contemplating the expansion prospects and good scope for margins to enhance, traders with a long-term perspective of 4-5 years can subscribe to the problem, however in small portions, given the uncertainties associated to how the aggressive setting will pan out over the subsequent few years.

Worth creation is contingent on margins increasing. ixigo following a differentiated technique by having increased share in rail tickets reserving, deal with Tier II/III metropolis travellers and different worth added providers may fit to its benefit in the long term.

Enterprise

ixigo, which initially launched as meta search web sites for flights in 2007, is right this moment a full-fledged main OTA in India providing shoppers reserving amenities throughout trains, buses, flights, inns and cabs. It follows a multi-app technique below the ‘Home of Manufacturers’ method below which its completely different apps — ixigo flights, ixigo trains, Affirm Tkt and Abhibus — provide a spectrum of journey choices, every uniquely catering to focus on teams for these respective apps. It additionally gives valued added providers for additional charge, which embrace providers like 100 per cent refund for dangerous high quality of service for buses, free change of date for flights/cancellation.

ixigo has adopted natural in addition to acquisition-led method to development. In the present day, it’s the market chief amongst personal OTAs with regards to practice ticket bookings, with a market share of 52.64 per cent for the 9M FY24 interval. It had a 12.99 per cent share within the bus ticket reserving house and 5.3 per cent in flight ticket reserving house. Its foray into inns reserving is in early phases, with the corporate’s personal platform having been launched solely in December 2023 (earlier it used to redirect lodge bookings to Reserving.com).

ixigo is making an attempt to distinguish and place itself because the main OTA for the subsequent billion customers with a deal with localised content material and app options that purpose at fixing issues of Tier II/III with 94.39 per cent of its transactions in FY23 pushed by smaller cities and cities (both as supply or vacation spot). As per firm filings, ixigo is the biggest personal OTA by way of cumulative app downloads as of September 2023 at 288.4 million, with subsequent largest personal OTA at 249.2 million and third largest personal OTA at 19 million. It scores nicely on month-to-month lively customers (MAU) — the most recent information given in its filings for the month of September 2023 exhibits ixigo had MAU of 83 million, versus the subsequent OTA at 81.5 million, with the third participant a lot decrease at 4.4 million.

Thus it’s clear ixigo scores very nicely by way of person engagement. Nevertheless, it additionally must be clearly famous that its common transaction values are a lot decrease versus friends, given deal with practice and bus bookings. So, to grasp this, traders should keep in mind that the income differential between ixigo and the third participant within the business with a lot decrease app downloads and MAU just isn’t important. However the benefit right here for ixigo is that it has enormous potential to maintain mining its enormous buyer base as they transfer up the spending curve. Its long-term success, to an excellent extent, will rely on this.

At a broader sectoral stage, the net journey market in India is estimated at ₹2,079 billion in fiscal 2023 and is anticipated to develop quicker than the general journey market at 13 per cent CAGR for the forecast interval of fiscal 2023 to fiscal 2028 and attain ₹3,895 billion by fiscal 2028. Inside this, the OTA business’s reserving worth is anticipated to develop at a CAGR of 18 per cent. That is as per information in IPO filings of ixigo. A competitor’s IPO submitting a number of months again estimated the OTA business web income development for a similar interval at round 15 per cent. So, traders must issue for such variations.

Ixigo market share of the reserving quantity of OTA market was at 6.52 per cent for 9MFY23.

Financials

ixigo has reported good development over the past yr with income for the 9MFY24 at ₹491 crore, up by 34 per cent versus 9MFY23. EBITDA was at ₹34.3 crore, up 15 per cent Y-o-Y. EBITDA margins declined from 8.19 per cent to six.99 per cent as the corporate spent extra on promoting and promotion in present fiscal. Take charge (ticketing income/gross transaction worth) was at 7.7 per cent. It has ranged at 7-8 per cent in recent times.

It’s worthwhile at backside line as nicely, however solely marginally, with web revenue for the interval at ₹65 crore boosted by distinctive objects and tax credit.

#ixigo #IPO #Subscribe