Nonetheless, some have discovered it powerful to get again into profitability on the web stage even within the post-Covid restoration interval, although many operational metrics are trying up.

For example, we have now Juniper Resorts — a partnership between the Saraf and Hyatt teams — that’s the largest proprietor of the Hyatt-affiliated lodges in India. Juniper Resorts is popping out with an preliminary public providing of shares that’s open from February 21 to 23.

The corporate hopes to lift ₹1,800 crore from the IPO on the higher finish of the worth band (₹342-360) totally through recent challenge of shares.

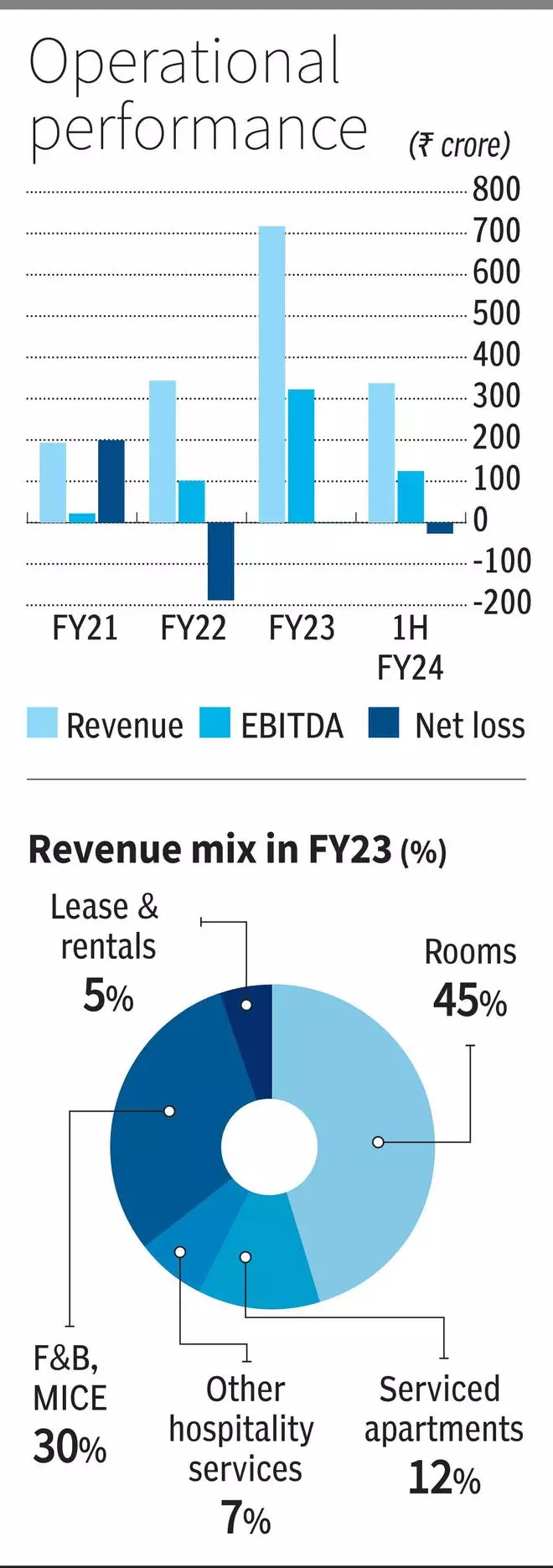

Juniper Resorts recorded losses in FY21, FY22, FY23 and 1HFY24. One of many key causes cited is the excessive debt incurred and the resultant curiosity price it has needed to pay in recent times.

At ₹360, the provide trades at an EV to EBITDA (1HFY24 annualised) a number of of 34 instances on a post-offer foundation, which is way larger than many friends’ — not strictly comparable, as they serve totally different buyer segments and luxurious ranges. The vary of EV/EBITDA multiples is extensive, with some in single digits and others getting as much as 37-38 instances. Suffice it to say that the provide asks for costly valuations.

The corporate’s revenues and EBITDA, although, have risen sharply over the previous 2-3 years because the post-Covid restoration took form throughout the hospitality trade. Between FY21 and FY23, Juniper Resorts’ revenues rose at a CAGR of 92.8 per cent to ₹717.3 crore, whereas EBITDA zoomed at 281 per cent over the identical two-year interval to ₹322.4 crore. The EBITDA margin for FY23 was 45 per cent and the corporate hopes to enhance on the determine in FY24; 1HFY24 margin was 37 per cent, although the determine in itself is pretty wholesome.

Losses narrowed to ₹1.5 crore in FY23 from ₹188 crore in FY22. In 1HFY24, losses as soon as once more expanded to ₹26.5 crore.

Listed corporations within the lodges area that cater to assorted clients at assorted worth factors commerce at 75-100 instances their trailing 12-months’ per share earnings, factoring in a reasonably sturdy state of affairs for the lodge trade within the subsequent few years.

Buyers can wait out this IPO and purchase within the secondary markets a bit later when an excellent a part of Juniper Resorts’ debt reimbursement is finished and the return to profitability (on the web stage) turns into clearer, particularly given the pretty elevated valuation that the provide calls for. This suggestion doesn’t assume any itemizing pop which may be potential in exuberant markets.

Hyatt is a well known premium model. Income combine contains lodge rooms, serviced residences, meals & drinks, lease/leases and different hospitality providers, sturdy metrics – occupancy, common room charge (ARR) and income per obtainable room (Rev PAR) – are positives. However as indicated earlier, within the absence of profitability, it could be dangerous to construct in excessive multiples.

At an trade stage, as corporations insist on staff returning to workplace, particularly within the IT area, there’s more likely to be a spurt in enterprise journey. Home and inbound worldwide tourism-related journey can be matching pre-Covid ranges and is anticipated to develop quickly, whereas conferences, exhibitions, incentives associated to corporations, marriages, resume their common course.

Sound operational efficiency

The corporate runs seven lodges and 6 serviced residences in six cities with 1,836 rooms. Amongst these, the properties in Delhi and Mumbai account for 80 per cent of the overall revenues, together with meals and drinks.

Juniper Resorts caters to the luxurious and upscale segments of shoppers through its choices.

Its general income combine is sort of wholesome. Rooms account for 45 per cent of revenues, whereas serviced residences for (12 per cent), meals & drinks (30 per cent), lease leases (5 per cent) and different hospitality providers (7 per cent).

Juniper Resorts has seen occupancies improve within the final 2-3 years. From 34 per cent ranges in FY21, occupancy rose to 76 per cent in FY23. Within the first half of FY24, the occupancy ranges are at 75 per cent, which is according to the typical trade requirements.

Common room charges have risen sharply, too, because the trade took steep hikes to get well from the distressed ranges of 2020-22. From ₹5,657 in FY21, the ARR has elevated to a sturdy ₹10140 for 1HFY24. RevPAR, has taken a sharper upward trajectory from 1,936 in FY21 to 7,588 as of 1HFY24.

The room charges are comparatively excessive, although not among the many highest and the corporate is seeking to additional improve charges within the coming quarters.

Meals & drinks contribution to revenues has elevated from 25 per cent in FY21 to 32 per cent in 1HFY24, which is sort of wholesome for margins if the development sustains.

The corporate’s meals and drinks retailers embody Annamaya, Celini, China Home and Fifty 5 East, amongst a couple of others.

Lowering debt burden

Juniper Resorts has whole borrowings of about ₹2,267 crore as of September 2023. Debt to fairness ratio is round 2.9 instances pre-IPO. The corporate is seeking to repay about ₹1,500 crore of this mortgage quantity from the provide proceeds. After reimbursement, finance prices of ₹266 crore in FY23 and ₹132 crore in 1HFY24 would come finished considerably, giving scope for a return to profitability on the web stage if different operational components play out.

In line with a Horwath HTL report, international demand for lodges in India would contact 100 per cent of pre-Covid ranges by FY25 and 130 per cent by FY27. Within the case of home demand, FY24 itself has seen a bounce of 12 per cent over pre-Covid ranges. Because the provide of rooms (8 per cent CAGR over FY24-27) would fall in need of anticipated demand (10.6 per cent CAGR over FY24-27), the pricing energy is about to stay agency for the lodges trade.

#Juniper #Resorts #IPO #Subscribe