As buyers proceed to clamour for his or her pie of the Magnificent Seven shares, listed here are 5 issues to know earlier than you place your bets on them.

#1 Deep moats

enterprise is sort of a robust fortress with a deep moat round it. I need sharks within the moat to maintain away those that would encroach on the fortress – Warren Buffett

The Magnificent Seven shares’ market cap represented round 20 per cent of S&P 500 market cap when markets have been at their pre-Covid highs in January/February 2020. At this time, they signify 30 per cent of S&P 500 (and round 50 per cent of the Nasdaq), reflecting the very best stage of dominance of some know-how shares for the reason that dotcom bubble.

Out of the highest 7 corporations on the peak of the bubble then — Microsoft, Intel, Cisco, Qualcomm, Oracle, JDS Uniphase and Solar Microsystems — Microsoft managed to retain its dominance as a Huge Tech; In addition to, Intel managed to dominate the PC and later the datacentre computing panorama for a very long time until AMD turned the tide from round 2017. Equally, Qualcomm continued to stay market chief in cellular processors and in addition bought a royalty on just about each smartphone bought on this planet. Thus, their moats have been robust (besides within the case of JDS Uniphase and Solar Microsystems). Their dominance withered solely after a decade or extra, as competitors from SaaS corporations for Oracle, and commoditisation of merchandise, as within the case of Cisco’s routers, impacted their enterprise prospects.

At this time, the dominance is even mightier. The moats of the Magnificent Seven are very robust not solely within the respective companies they dominate but in addition in AI.

In terms of AI, knowledge is not only the brand new oil, however new lithium as effectively! Additional, coaching massive language fashions requires not simply huge quantities of information but in addition a number of monetary sources. The Huge Techs of the Magnificent Seven at the moment have unparalleled advantages of scale and troves of information acquired from thousands and thousands of consumers over a long time and have deep pockets too. This makes it troublesome for a brand new entrant to compete and counter with options within the present scheme of issues. A living proof is Open AI requiring investments from Microsoft to commercialise ChatGPT.

Microsoft, Google, Meta, Amazon, Tesla and Apple have large lead over the closest rivals right here. To be clear, the businesses at the moment declare to have constructed their massive language fashions solely utilizing publicly out there knowledge. However the boundary traces are obscure and it might be a only a matter of time when non-public consumer knowledge too is employed to make the AI fashions higher. For instance, whereas Tesla is a late entrant to this knowledge treasure area, thousands and thousands of Tesla vehicles world wide have, for years, been sending again vital automobile and consumer knowledge, together with all essential knowledge from the digicam suite. This non-public consumer knowledge is essential to develop full autonomous autos and robotaxis.

Whereas Nvidia might not have the information benefit the others within the pack have, it has created an enormous moat with its first-mover benefit and dominance of the massive language mannequin (LLM) coaching ecosystem. In response to varied estimates, Nvidia’s market share in AI chips is anyplace between 70 and 90 per cent, making it a close to monopoly as of now. Even when competing GPU chips, that are core to LLMs, hit the markets this 12 months, Nvidia’s dominance might maintain due to its first-mover benefit and software program API linked to its AI GPU chips. As LLM coaching fashions are developed on this, the cloud corporations who present the infrastructure additionally want to take a position solely in Nvidia chips to make sure compatibility. This creates a loop – as cloud corporations make investments closely in Nvidia primarily based infrastructure, new LLMs are additionally developed totally on this.

Backside line: The Magnificent Seven shares have robust moats pushed by a mixture of core competency in know-how, knowledge benefit and monetary muscle energy.

#2 Stable core companies

AI could possibly be the long run, however a bridge is required until a profitable transition to being AI corporations occurs for the Magnificent Seven. The very fact is that AI nonetheless largely stays an unprofitable cash-guzzling enterprise and will stay so for some time. Actually corporations dominating the cloud enterprise like Amazon, Microsoft and Google are largely subsidizing their AI choices for patrons. Nonetheless, the bridge to a profitable AI enterprise is their present profitable companies. Every of those corporations globally dominate companies from which they derive important income. The mixed income of the Magnificent Seven provides as much as a staggering $1.75 trillion, with working earnings totalling as much as a bit over $400 billion. Microsoft and Amazon dominate the worldwide cloud enterprise with a mixed market share over 50 per cent. Additional Microsoft and Amazon have for many years been the leaders in different segments as effectively from which they derive important income. Alphabet and Meta dominate the worldwide digital promoting market with an estimated 55-65 per cent market share. Not too long ago Apple displaced Samsung because the chief in world smartphone market, with its 20 per cent market share in that area. Whereas Tesla was not too long ago displaced by Chinese language rival BYD because the world’s largest vendor of EV autos when it comes to items bought, in the case of income and earnings Tesla stays the worldwide chief. A lot of the management of Magnificent Seven corporations is more likely to maintain for the foreseeable future which is able to hold them in buyers highlight even with out factoring AI.

# 3 Present competency in AI

The 12 months 2022 was brutal for Meta. The inventory crashed by 40 per cent within the first two months of the 12 months after Meta mentioned that Apple/iOS privateness modifications would influence its concentrating on promoting of Fb/Instagram customers on Apple gadgets. Then, by November 2022, the inventory had crashed a close to 80 per cent from peak as its relentless investments in AI and Metaverse crushed its working margins. Quick ahead to at the moment — the shares have rebounded a staggering 450 per cent in 14 months.

Amongst just a few essential components that drove this rebound have been its investments in AI paying off. These investments made it attainable to work across the iOS privateness modifications, increase its income and in addition enhance effectivity in its operations. This was mirrored in its working margins capturing as much as close to 50 per cent in 2023 from round 18 per cent in 2022.

Such AI capabilities is probably not unique to Meta, and it’s fairly seemingly every of the Huge Techs is already harvesting the advantages of AI of their inside operations.

This aside, their distinctive capabilities in massive language fashions — Alphabet-Gemini, Meta -Llama, Microsoft-OpenAI — are well-known. Amazon is engaged on an LLM known as Olympus. In the meantime, Tesla is investing closely in its Dojo supercomputers focussed on laptop imaginative and prescient video processing and recognition that may kind the bottom for its full self-driving vehicles and robotaxis.

Among the many Magnificent Seven, besides Apple, the remaining have given sufficient indications on their AI path. Technological developments aside, the monetisation path can be clear, like AI boosting cloud enterprise and subscription enterprise revenues for Microsoft, Amazon and Google; or utilizing AI to spice up consumer expertise and increase advert revenues within the case of Google and Meta.

Google, Amazon, Meta and Microsoft are additionally growing their very own AI chips to cut back dependency on Nvidia. Alternatively, Nvidia is foraying into cloud companies. Thus, the AI path is witnessing speedy development and modifications, and buyers can guess there can be many twists and turns alongside the way in which as every firm’s AI capabilities evolve and new monetisation alternatives might emerge.

Within the case of Apple, which has been tightlipped in the case of AI, buyers are giving the corporate the good thing about the doubt given its technological prowess. The one trace Apple has given on its AI plans is that it might have one thing to announce later this 12 months.

#4 Alternatives and dangers

The AI alternatives are immense and the journey is simply beginning. When Steve Jobs launched computer systems, he gave the analogy of the way it was a ‘bicycle to the thoughts.’ This was in reference to a analysis which confirmed that people have been amongst slowest species in the case of ‘effectivity of locomotion’. Nonetheless, when people developed a bicycle, they moved to primary spot. Thus if computer systems have been equal of bicycles to enhance productiveness, AI may signify a ‘Concorde to the thoughts’ in the case of prospects that people can obtain. This can most certainly lead to sharp jumps in productiveness and wealth creation.

Generative AI will influence the way in which the world capabilities in two methods as defined by Jensen Huang – the founder and CEO of Nvidia; one is when AI meets the digital world and different is when AI meets the bodily world. The likes of ChatGPT and Gemini/Bard signify AI within the digital world. Tesla’s Robotaxis idea is an instance of AI within the bodily world.

As themes develop, whereas present Magnificent Seven will proceed to prosper given their moats, new leaders may also emerge in new areas of AI, simply as Google and Amazon mushroomed throughout and after the dotcom bubble. In a future version, we will cowl rising alternatives and firms with potential within the AI area at bl.portfolio.

On the identical time, buyers additionally must be cognizant of dangers. To start with, already there’s debate whether or not the Magnificent Seven have to be rechristened to Spectacular Six or Fabulous 5 after Apple and Tesla have underwhelmed within the final one 12 months.

Additional, there’s additionally an rising danger that Huge Techs have gotten too dominant and AI will solely speed up that view. The clamour towards their clout and management can also rise sharply together with rise in AI. Therefore, there’s all the time the specter of regulatory motion that may create velocity bumps of their progress. Deepfakes and the way the labour markets can get impacted are just a few different examples of massive dangers. This and lots of different unknown dangers are lurking. To this extent the AI euphoria might have gotten forward of fundamentals at this time limit. Buyers have to issue these earlier than putting their bets.

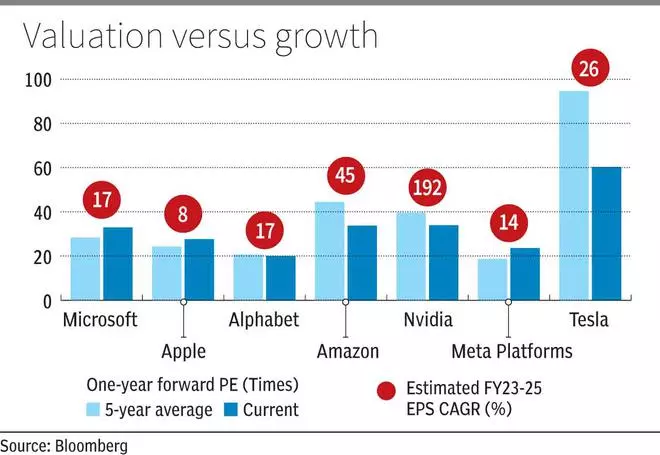

# 5 Valuation

As talked about above, 5 out of the seven high tech corporations on the peak of the dotcom bubble retained their moats and their enterprise continued to develop. However did it end up effectively for the buyers? By no means.

If buyers had guess on the ‘Magnificent Seven’ (seven high tech shares of Nasdaq 100) of the dotcom bubble in the course of the frenzy then, they’d have learnt exhausting classes over the past 20 years. Aside from Microsoft, no different firm within the group has crushed the S&P 500 and Nasdaq 100 CAGR from March 2000 (the month during which the dotcom bubble peaked) until now. A few of them turned out to be utter wealth destroyers.

Bottomline – enterprise development is essential, however valuation at which you purchase is essential as effectively.

On the identical time, whereas valuations will not be frothy now as in the course of the dotcom bubble, most of them will not be low-cost as effectively. However this additionally comes with a catch. The expansion too, aside from Nvdia, shouldn’t be as as nice because it was within the run as much as the height in 2000.

One other issue to bear in mind is that the valuation ranges for these corporations will differ, given their companies are totally different.

For instance, Meta and Alphabet are extra depending on advert revenues, which is extremely cyclical, whereas cloud and subscription dependent companies of Amazon and Microsoft are usually extra resilient throughout downturns.

Nonetheless, total, on a risk-reward foundation, at current Alphabet seems to supply the perfect play on AI at present valuations.

At bl.portfolio we had advisable a purchase on Meta Platforms in February 2022 and doubled down on our name to purchase the inventory when it hit all-time low in November 2022. Following multi-bagger returns since then, we can be reviewing our name shortly.

In case of different corporations, buyers can await cheaper entry factors. Over and above present fundamentals that may justify a sure worth, there’s the AI story that has added plenty of premium to the shares. What’s the proper premium, is left to every investor’s judgement.

#Magnificent #Craze