With a commanding market share of over 95%, it operates as a close to monopoly in commodity buying and selling quantity. Working by way of its wholly owned subsidiary, the Multi Commodity Trade Clearing Company Restricted (MCXCCL), the corporate moreover affords settlement and clearing companies.

The corporate had been dealing with points with respect to Commodity Derivatives Platform (CDP) as there was delay in migration to new platform. The difficulty is now behind and the upper prices due to the platform will normalise from the fourth quarter of this fiscal.

For the reason that announcement of Q3 outcomes on February 10, the inventory of MCX fell initially however has recouped all losses by closing at ₹3,832.75 final week. Because it has rallied sharply since July final 12 months the valuation has turned costly. The one-year ahead P/E (Worth/Incomes) stands at 47 instances versus the five-year common of 32.

We had prompt that buyers accumulate MCX in June final 12 months when the share value was buying and selling at round ₹1,563. Given the current developments, what ought to buyers do? Beneath is our take.

Platform value

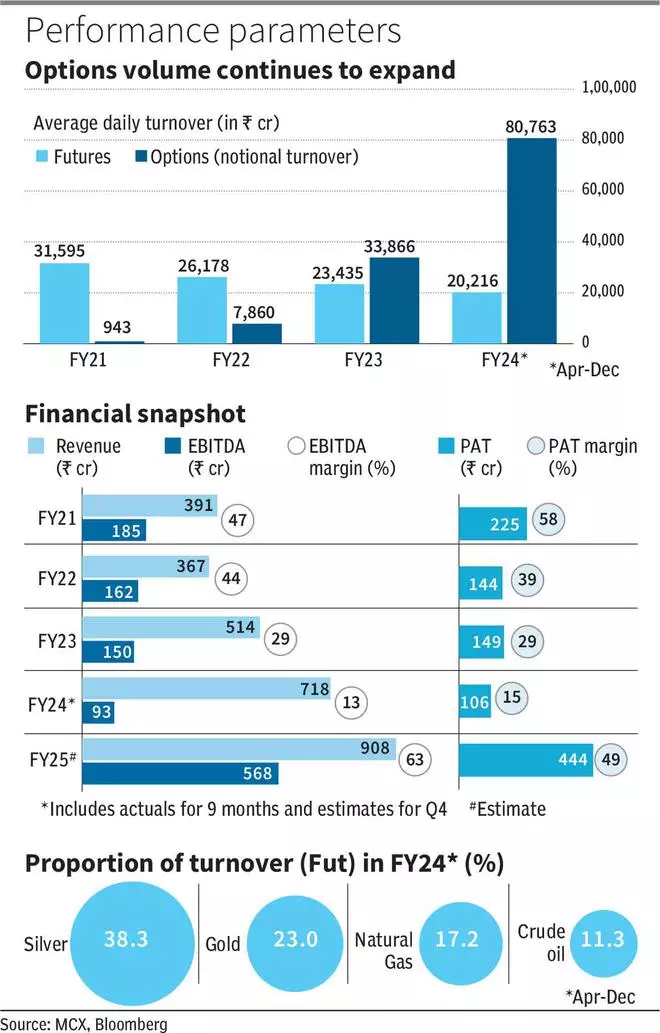

Within the quarter ended December 2023, powered by possibility buying and selling quantity, the corporate’s whole income jumped 28 per cent year-on-year (yoy) to ₹209.3 crore. Working income was up 33 per cent to ₹191.5 crore.

Nonetheless, MCX ended up making a loss regardless of wholesome prime line progress. EBITDA loss stood at practically ₹2 crore in Q3FY24 in comparison with a revenue of ₹52.8 crore in Q3FY23. PAT was a unfavourable ₹5.4 crore for the quarter as towards a revenue of ₹38.8 crore in the identical quarter final 12 months.

The loss was primarily because of greater software program help costs. This was due to the delay in migration to a brand new Commodity Derivatives Platform (CDP) developed by Tata Consultancy Companies (TCS). Because the transition was delayed, MCX needed to prolong the licence for the previous platform, supplied by 63 Moons Applied sciences, at a big value.

The corporate needed to spend ₹81 crore per quarter between January and June 2023 and ₹125 crore per quarter between July and December 2023. For comparability, this value was ₹15 crore 1 / 4, traditionally. Additional, there was an SGF (settlement Assure Fund) contribution of ₹13.1 crore in Q3FY24.

That mentioned, MCX transitioned to the brand new CDP in October final 12 months. So, the prices associated to the platform are anticipated to normalise from the fourth quarter of this 12 months.

The entire value of ₹237 crore of the brand new CDP shall be amortised over the following 5-10 years. MCX pays no annual upkeep costs for TCS until October 2024. It’s anticipated to kick in publish that. At this level, this value just isn’t declared by the corporate.

Since MCX is not going to incur the one-off prices like within the earlier quarters, it’s anticipated to publish a powerful backside line from Q4FY24 onwards, which can mirror totally within the subsequent fiscal 12 months. For FY25, present Bloomberg consensus estimates venture EBITDA to develop by 510 per cent Y-o-Y to ₹568 crore and EPS to extend by 338 per cent to ₹87.31.

Hovering choices quantity

The Common Day by day Turnover (ADT) of futures and choices mixed grew 83 per cent yoy to ₹1.15 lakh crore in Q3FY24. However dissecting this may present that it was the choices’ ADT that ballooned whereas ADT in futures declined. Consequently, of the ₹156 crore earnings earned by way of transaction costs, practically two-thirds i.e., ₹101 crore, is from choices.

ADT in choices stood at ₹95,989 crore within the third quarter of this monetary 12 months, a rise of 144 per cent in comparison with ₹39,402 crore in the identical quarter of the earlier 12 months — whereas ADT in futures shrank to ₹20,796 crore for the quarter versus ₹24,265 crore in the identical interval of the final fiscal.

Power commodities is the dominant quantity contributor in choices phase with an ADT of ₹86,224 crore. Curiously, its share has come all the way down to 90 per cent of the overall choices quantity in Q3FY24, from practically 94 per cent in Q3FY23. For the corresponding interval, the ADT of Bullion choices elevated practically fourfold to ₹8,237 crore. A pick-up in gold and silver choices quantity is optimistic for the corporate as extra buying and selling can fetch extra earnings for MCX by the use of transaction costs.

MCX plans to launch choices on crude oil mini futures and pure fuel mini futures quickly, which is prone to additional enhance choices buying and selling.

Within the futures phase, solely Bullion noticed a rise in quantity. ADT in bullion futures improved 13 per cent yoy for the quarter to ₹13,059 crore. Nonetheless, ADT in power futures and base metals futures declined 31 and 58 per cent yoy to ₹5,655 crore and ₹1,719 crore, respectively.

Larger curiosity in bullion futures may very well be due to the decrease margin requirement. As an example, the margin for gold futures is about 8 per cent however for crude oil futures and pure fuel futures, it’s round 34 and 20 per cent, respectively.

Silver dominated the futures phase with a 38 per cent share, adopted by gold (23 per cent), pure fuel (17 per cent), and crude oil (11 per cent).

Total, rising curiosity in commodity choices buying and selling fuels MCX turnover and that is anticipated to persist in upcoming quarters.

What ought to buyers do?

Though the scrip has significantly appreciated, we advise that buyers who’ve 3–5-year perspective proceed to carry the inventory.

It’s because, after posting losses for 2 quarters in a row, the corporate is lastly anticipated to reap the advantages of shifting to its personal platform, going forward.

Part of that is factored within the value however we predict there’s extra potential. MCX, which garners wholesome volumes within the choices phase, could be boosted additional by the launch of recent contracts. Furthermore, the corporate has a close to monopoly in commodity derivatives area within the nation and there’s no risk to this within the foreseeable future. As an example, MCX holds a market share of 96 per cent in commodity futures in India.

The above elements can help the upper valuation. .

#MCX #Set #Woods