Issue investing is an funding strategy that includes focusing on particular drivers of return for an asset reminiscent of equities. Globally, funding managers — quantitative traders, particularly — have employed ‘components’ through the years to construct and improve their portfolios. As of March 31, 2022, issue ETFs managed about $1.6-trillion belongings globally, a 24.6 per cent CAGR in contrast with the $178 billion 10 years in the past, based on S&P Dow Jones Indices.

Issue investing has among the options of passive investing, reminiscent of being low price. It additionally has among the options of energetic administration by aiming to generate returns above the market-cap weighted index.

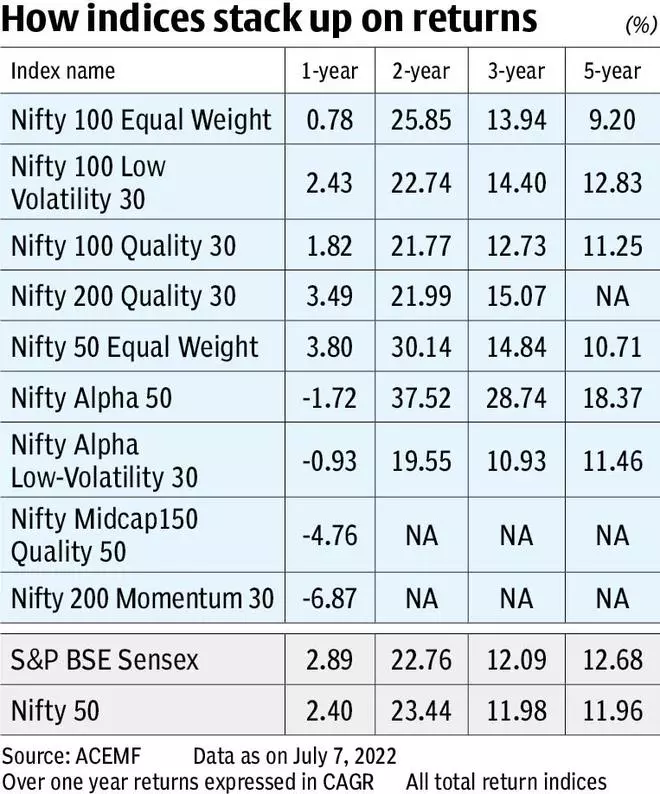

Ultimately rely in India, there have been a complete of two dozen index funds, trade traded funds and fund of funds that use some ‘issue’. Here’s a lowdown on these factor-based funding choices and their suitability.

Key ‘components’ utilized in investing

Right now, among the frequent components which were properly documented in educational literature and adopted by the funding business embrace low volatility, momentum, high quality and worth.

Thoughts you, the factor-investing panorama is evolving in India, with solely a dozen merchandise having a minimum of a one-year monitor document.

Worth issue

One of many oldest types of fairness investing, the worth strategy harks again to the times of Benjamin Graham. Worth investing focusses on corporations with excessive intrinsic worth, the place the inventory is promoting at a market value under the honest/true worth. The premise of all worth investing is that shares with decrease valuations are likely to generate increased anticipated returns relative to corporations with increased valuations. The present passively-managed mutual fund merchandise that use ‘worth’ issue embrace Kotak NV 20 ETF, ICICI Pru NV20 ETF and Nippon India Nifty 50 Worth 20 Index Fund, with monitor information of one-six years. Do observe the Nifty Worth 20 index displays the efficiency of a diversified portfolio of 20 worth shares forming a part of Nifty 50 index. These shares are chosen on the idea of Return on Capital Employed (ROCE), Value-Earnings (PE), Value to E book Worth (PB) and Dividend yield (DY).

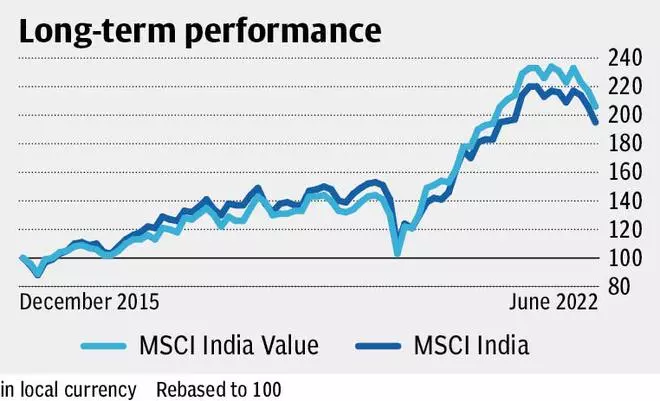

Our view: Although value-oriented portfolios can underperform the marketplace for prolonged intervals, worth investing supposedly works properly throughout corrections and within the early stage of rebound. Evaluating the MSCI India Worth index with MSCI India index, we are able to see that through the worst months reminiscent of March 2020, the worth index (down 20.6 per cent) has outperformed the usual index (down 23.4 per cent). In October 2008 when markets fell, MSCI India Worth (down 20.17 per cent) outshone MSCI India (down 25.43 per cent) by 500 foundation factors. Worth additionally does properly throughout early levels of a rebound as we’ve seen in cases reminiscent of December 2008 and April 2020, with 75- and 400-basis level outperformance respectively. Nevertheless, do observe, over longer intervals of time, worth is but to show its edge should you examine absolute returns of MSCI India Worth (up 177 per cent) versus MSCI India (up 223 per cent) — the time knowledge collection is out there from Could 2008. As a substitute of an outright 100 per cent allocation to worth, traders ought to mix development and worth in a combination that fits their threat urge for food.

Momentum issue

The momentum issue was first documented in a 1993 analysis paper ‘Returns to Shopping for Winners and Promoting Losers: Implications for Inventory Market Effectivity’. The momentum issue refers back to the tendency of profitable shares, normally in six-month and 12-month intervals, to proceed performing properly within the close to time period. At present in India, there are three passively-managed momentum-based MF merchandise — Motilal Oswal Nifty 200 Momentum 30 ETF, Motilal Oswal Nifty 200 Momentum 30 Index Fund and UTI Nifty200 Momentum 30 Index Fund. The Nifty200 Momentum 30 index tracks the efficiency of 30 high-momentum shares throughout large- and mid-cap shares. The Momentum Rating for every inventory relies on current six-month and 12-month value return, adjusted for volatility.

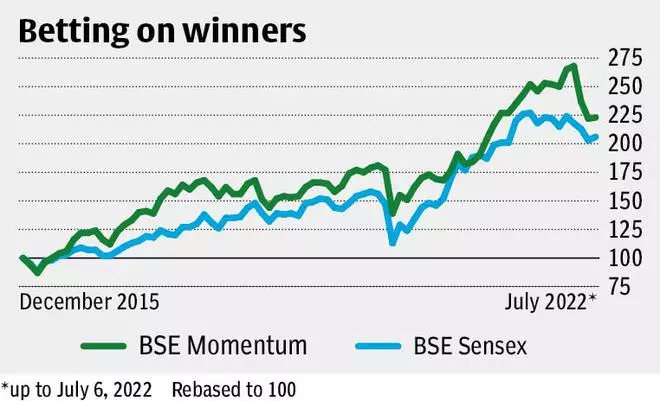

Given the momentum bias, the shares, and by extension the sectors picked up will principally be those that market favours at that cut-off date. The momentum indices sometimes have proven the flexibility to steadily outperform broader indices reminiscent of Nifty 50, particularly throughout market rallies. As an example, in 2017 when the Sensex gained practically 28 per cent, the BSE Momentum index jumped by about 49 per cent. Equally in 2021 when the Sensex galloped by 22 per cent, the momentum index (up 32.6 per cent) outperformed by 10 proportion factors. Nevertheless, do observe the efficiency takes successful throughout corrections, instance might be to date in 2022, or in flattish phases reminiscent of 2018. That is the problem with momentum technique, as it’s not a draw back containment strategy.

Our view: Any momentum-based index fund or ETF isn’t appropriate in your holding. At greatest, it may be utilized in mixture with different funds in your portfolio. The churn in momentum-based funds is mostly very excessive in comparison with broad-based index funds/ETFs. It’s because not like different components reminiscent of high quality, worth and low volatility, the outperformance from the momentum issue tends to be short-lived. Thus, the technique might require a relentless rebalancing to take care of the momentum publicity, resulting in further turnover price. Additionally, momentum as an funding technique is a high-risk one because it exposes the portfolio to sharper and longer draw-downs.

Low volatility issue

Standard knowledge would recommend that increased threat would indicate increased anticipated return. Nevertheless, some researchers discovered that lower-risk belongings are likely to outperform higher-risk belongings over time within the fairness market. And, that is referred to as the low volatility issue. It gained reputation after the 2008 World Monetary Disaster.

In India, at the moment there are half-a-dozen low volatility issue primarily based passive funds reminiscent of Kotak Nifty 100 Low Vol 30 ETF, Motilal Oswal S&P BSE Low Volatility ETF, Motilal Oswal S&P BSE Low Volatility Index Fund, UTI S&P BSE Low Volatility Index Fund, ICICI Pru Nifty Alpha Low Vol 30 ETF and ICICI Pru Nifty Alpha Low Vol 30 ETF FoF. Nevertheless, most of them have lower than two years of monitor document. Low volatility indices, be it the Nifty 100 Low Volatility 30 index or the S&P BSE Low Volatility index, monitor the efficiency of the 30 corporations from the underlying basket (Nifty 100 or S&P BSE LargeMidCap) with the bottom volatilities as measured by commonplace deviation of inventory returns.

The low-volatility funding strategy seeks to construct a portfolio of corporations with steady enterprise fashions which can be typically much less inclined to recessions and different macroeconomic occasions. Volatility of a inventory is measured by its commonplace deviation (SD).

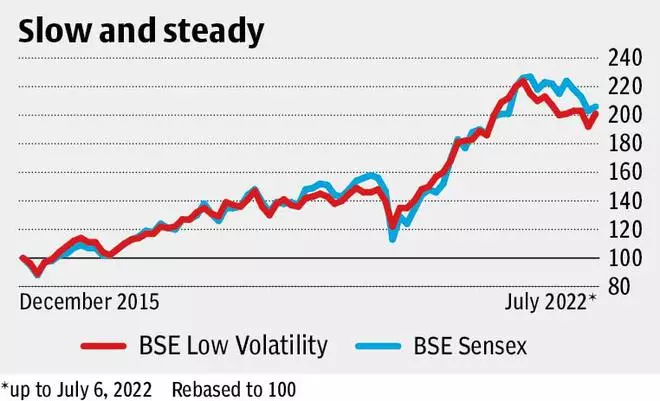

Our view: This technique tends to carry out properly in bear markets, due to its defensive nature. As an example, within the ongoing correction of 2022, the BSE Low Volatility index has fallen 6 per cent in comparison with practically 8 per cent dip within the Sensex. In 2018 when markets have been broadly flat, the low volatility issue eked out 100-basis level price outperformance over the Sensex. This pattern additionally performs out for shorter-period corrections. Nevertheless, the low volatility strategy understandably lags throughout bull markets. It is a trade-off that traders utilizing the issue have to just accept.

High quality issue

Curiosity within the high quality issue elevated within the aftermath of auditing scandals such because the Enron affair in 2001. The standard issue sometimes considers three important components of an organization: administration effectivity, monetary energy and earnings profile stability. However not like low volatility and momentum, there’s a lack of consensus on the definition of the standard issue.

The concept of the standard issue is to establish corporations with excessive profitability, a robust steadiness sheet and low monetary leverage. These corporations that exhibit the standard attribute are understood to handle capital successfully, whereas nonetheless having the ability to generate strong money stream in the long term. That is most likely why traders are likely to pay premium costs for such ‘high-quality’ corporations.

At present, there are a number of passively-managed high quality issue primarily based funds reminiscent of Edelweiss Nifty 100 High quality 30 Index Fund, SBI Nifty 200 High quality 30 ETF, DSP Nifty Midcap 150 High quality 50 ETF and UTI Nifty Midcap 150 High quality 50 Index Fund, accessible for Indian traders. The present factor-based funds are constructed on Nifty 100 High quality 30, Nifty 200 High quality 30 or Nifty Midcap 150 High quality 50 indices. The indices use the mum or dad index (Nifty 100, Nifty 200 or Nifty Midcap 150) because the universe after which monitor the efficiency of the highest 30/50 shares chosen primarily based on their ‘high quality’ scores, which is decided primarily based on return on fairness (ROE), monetary leverage (Debt/Fairness Ratio) and incomes (EPS) development variability analysed through the earlier 5 years.

In current instances, the renewed curiosity within the high quality issue is the opportunity of reaching higher diversification on condition that inventory markets witnessed slim/concentrated rallies.

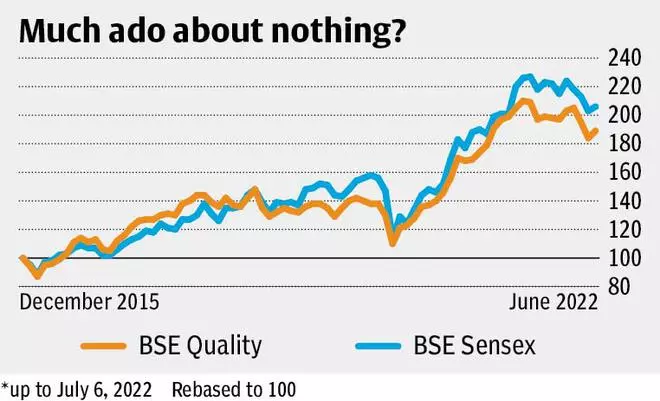

Our view: Do observe that many traders have a wholesome diploma of scepticism with regard to high quality’s standing as a standalone issue. When mixed with worth, high quality can improve good points as a result of one can be betting on clear, good and low cost shares.

The standard issue is alleged to come back in after a bull market is properly established. Assessing efficiency proves to be troublesome in such eventualities as a result of whether or not a bull market is properly established or not is simply precisely potential in hindsight.

Decoding components

Worth: Cheaper however good shares are likely to beat costly ones over time

Momentum: Shares which can be profitable are likely to preserve profitable, and vice versa

High quality: Shares which can be increased high quality are increased returning

Low volatility: Shares with decrease volatility normally outperform ones with increased threat over time

Equal weight good beta

An equal-weighted index is the place an equal sum of money is invested within the inventory of every firm that makes up the index. The basket is rebalanced at common intervals so that every inventory allocation goes again to equal weight. That is in stark distinction to any market-cap weighted index the place the larger the market-cap of a inventory, the upper its weight turns into.

At present, there are 5 MFs utilizing the equal weight good beta. These are DSP NIFTY 50 Equal Weight ETF, Sundaram Nifty 100 Equal Weight Fund, HDFC NIFTY 100 Equal Weight Index Fund, ABSL Nifty 50 Equal Weight Index Fund and HDFC NIFTY50 Equal Weight Index Fund. Over the long run, say 10 years or extra, the CAGR returns of the equal weight indices is best by small margin over market-cap weight indices. However, the story modifications within the three- and five-year intervals.

Our view: Extra weight to the historic winner shares exposes a portfolio to increased dangers as a result of shares/sectors commonly undergo rotation and when the biggest market-cap shares in a portfolio underperform, they’ve an out-sized influence on the general efficiency. In distinction, good beta merchandise primarily based on equal weight indices supply an anti-momentum, compelled buy-low-sell-high mode of investing that clearly comes with decrease inventory and sector focus dangers. Thus, a market-cap-weight primarily based index outperforms in periods of polarisation. However when all shares have equal weights, such a basket doesn’t have momentum bias and is basically a guess on imply reversion.

#Combine #match #components #beat #markets