As infrastructure and its many sub-segments took off sharply over the previous couple of years and proceed to thrive with heavy authorities investments and initiatives, many firms have benefitted from sensible execution of such initiatives.

On this regard, NCC is an organization that has been a key beneficiary of the deal with enchancment in infrastructure throughout the nation.

The agency operates in segments starting from constructing & housing, roads, water & surroundings, to irrigation, electrical works, mining and railways. These initiatives are executed for varied State and Central authorities entities.

A observe file of robust execution, diversified orderbook and a pipeline of profitable initiatives to be labored on over the following few years make the prospects for the inventory of NCC engaging.

The shares of NCC have doubled over the previous one 12 months, however are nonetheless fairly valued. At ₹166.70, the inventory trades at 18 occasions its trailing 12-months per share earnings and 14 occasions its doubtless per share earnings for FY24. Buyers with a 2-3-year perspective should buy the shares of NCC.

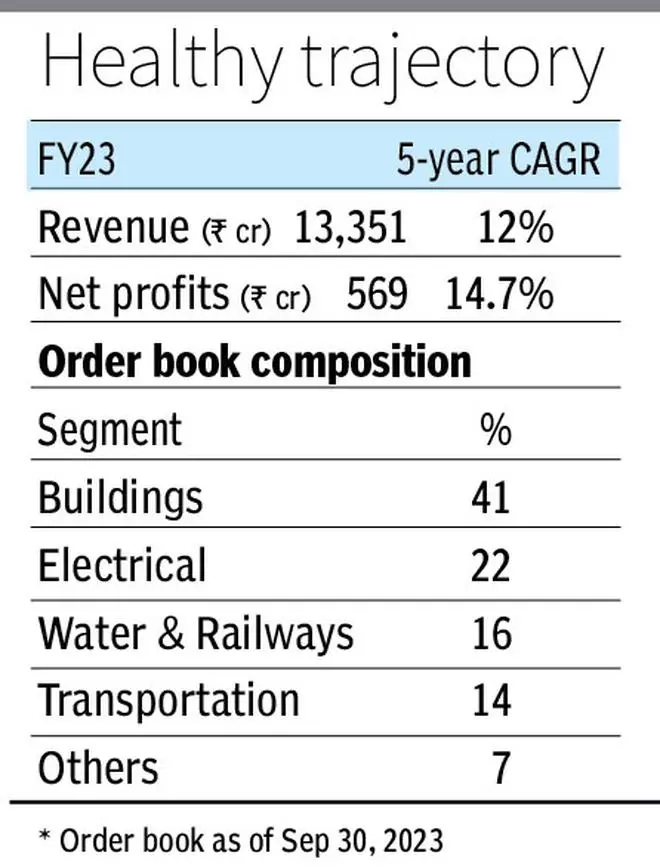

Within the final 5 monetary years (FY18-FY23), the corporate’s revenues have risen at a CAGR (compounded annual progress price) of 12 per cent to ₹13,351 crore in FY23, whereas internet earnings grew at 14.7 per cent over the identical interval to ₹569 crore.

Robust execution file

NCC operates in a number of segments of the infrastructure theme, as talked about earlier.

Industrial and industrial buildings, IT Parks, procuring malls, schools, hospitals, metros, highways, water therapy crops, underground drainages, electrification, transmission & distribution strains and sub-stations, dams, reservoirs, tunnels, track-laying, signalling and coal excavation are a few of its areas of experience.

A pattern of its initiatives executed contains, Nagpur Metro Rail, ESIC Hospital at Gulbarga, AIIMS Guwahati, Agra-Lucknow Expressway, SVAB, ISRO Sriharikota, Water Provide Mission in Odisha, Rubber Dam on Falgu River, Airport at Agartala and Nagpur-Mumbai Expressway, amongst many others.

NCC is at present executing or has received orders from North Bihar Energy Distribution Firm, Brihanmumbai Municipal Company, Maharashtra State Electrical energy Distribution Co., Navi Mumbai Worldwide Airport, Haryana Worldwide Horticulture Advertising and marketing Company and the like. The dimensions of those orders ranges from ₹1,144 crore to ₹5,755 crore, indicating deep consumer relationships. The UP Jal Jeevan Piped Water challenge is value ₹16,500 crore.

Massive, diversified order ebook

The corporate has witnessed a surge in its order ebook over the previous couple of years. Within the latest couple of quarters alone, it has received a complete of over ₹20,400 crore value of orders.

As of September 2023, NCC had an order ebook of a staggering ₹61,796 crore to be executed within the subsequent few years. The order ebook interprets to round 4 occasions its trailing 12-months’ revenues.

Being an EPC (Engineering, Procurement and Building) participant, the corporate is ready to bid well for its initiatives and has typically been in a position to keep an EBITDA (Earnings earlier than curiosity, taxes, depreciation, and amortisation) margin of 10 per cent or extra. This margin is wholesome given the dimensions at which it operates. NCC can also be more and more taking up initiatives that include escalation clauses to insulate the corporate from improve in enter costs.

The corporate has consistently been in a position to faucet into rising areas and develop experience to win orders. Sensible metering is one such space, given the main target that many State electrical energy boards put into it to cut back income leakages and tighten subsidies.

NCC’s present order ebook is sort of diversified with buildings (41 per cent), transportation (14 per cent), electrical (22 per cent), water & railways (16 per cent) and mining (7 per cent) being the principle constituents.

Given the variety of the order ebook, and the criticality of many initiatives that it’s executing, there may be appreciable visibility on earnings and margins for the following few years with none fears of cutbacks from governments.

Debt and one-offs

Regardless of rising at an affordable tempo and with a pretty big scale of operation, NCC has managed to maintain its debt degree beneath management. Gross debt has decreased from ₹1,985 crore as of September 2022 to ₹1,470 crore as of September 2023. The corporate has money and money equivalents of ₹215 crore as of September 2023.

Although NCC has indicated that debt could go up a tad over the following couple of quarters, the degrees of leverage are nonetheless comfy.

The web debt to fairness ratio is a bit of over 0.1, which is sort of a wholesome degree to function at.

Within the first half of FY24, NCC’s income rose 36.2 per cent over the identical interval in FY23 to ₹8,121.5 crore, whereas internet earnings declined 4.3 per cent to ₹2,31.3 crore. The explanation for the decline was a one-off arbitration challenge. In September 2023, NCC obtained an arbitration award of ₹198 crore after 5 years (from a consumer, Sembcorp), whereas the anticipated declare was ₹606 crore. On the identical time, the corporate additionally obtained a declare settlement of ₹152 crore from NHAI. These two claims collectively impacted income by ₹199 crore and internet earnings by ₹149 crore in Q2FY24 as impairment — no money outflows, although. In any other case, the primary half internet earnings would have soared sharply.

#NCC #purchase #key #infrastructure #participant