For fairly some time there was a story that the personal sector should choose the capex baton from the Central authorities to take the financial system ahead. How prepared is it?

To get a perspective, we analysed listed shares within the core sectors. By contemplating the listed shares within the core phase — fertilizers, cement, crude oil and pure fuel, energy, refineries, metal and coal — we will, to an extent, gauge the power of the capex and productiveness development within the financial system. Aside from analysing the mixture numbers, which may clean over a number of outliers, we now have additionally picked the highest three firms in essentially the most seen sectors — energy, metal and cement — to evaluate how every firm is positioned on the expansion curve. Listed here are our key takeaways.

Key findings

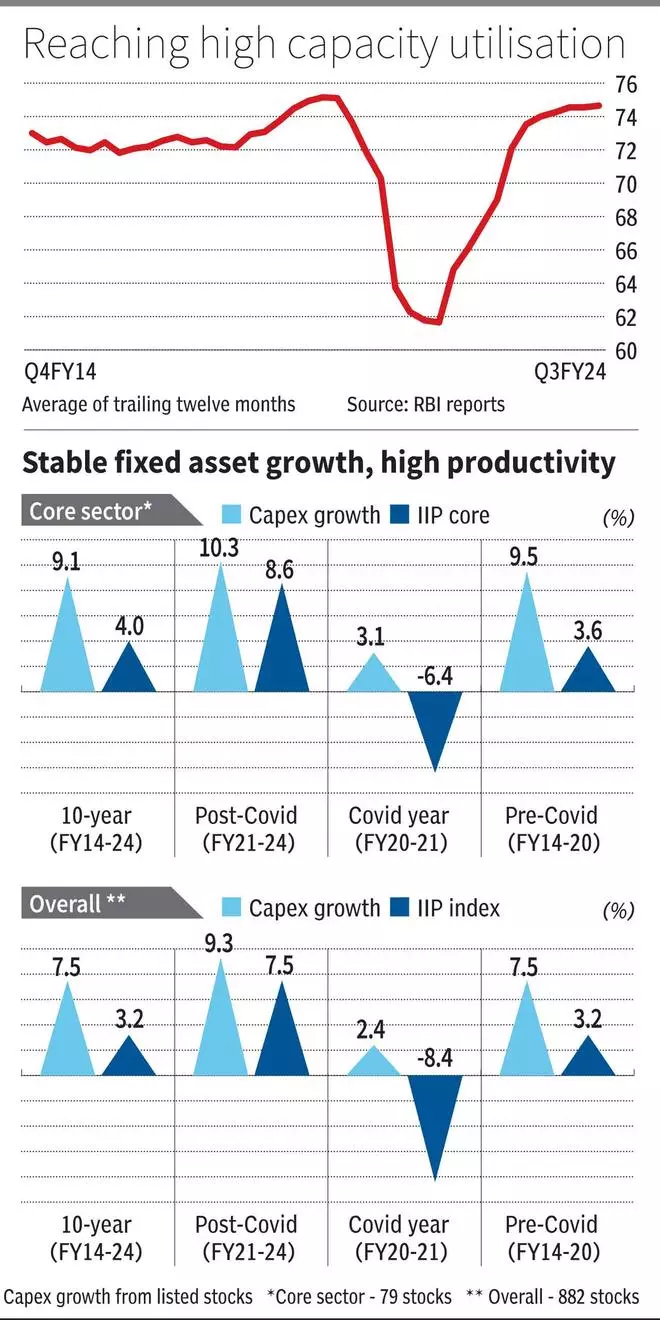

The combination numbers level to steady fastened belongings (together with CWIP) development and excessive IIP (Index of Industrial Manufacturing) development. The 79 core sector firms on our evaluation reported fastened asset development of 10.3 per cent CAGR publish Covid, marginally above the pre-Covid years. This charge of development has hovered above the expansion for general universe, each pre and publish Covid. However the hole is closing, regardless of the upper charge, implying higher development from non-core sectors as nicely.

The massive change publish Covid has come from the IIP index. In comparison with 3.6 per cent CAGR pre-Covid, the core sectors have reported double the expansion at 8.6 per cent CAGR publish Covid. The identical holds true for general shares as nicely. The trailing measure of the capability utilisation charge printed by RBI can be reaching the important 75 per cent ranges, which helps the excessive capital funding charge the core sector firms are getting ready for.

Analysing particular person firms, the excessive capital funding theme continues to ring true. Energy, cement and metal firms level to high-capacity addition by the 2030-32 timeframe.

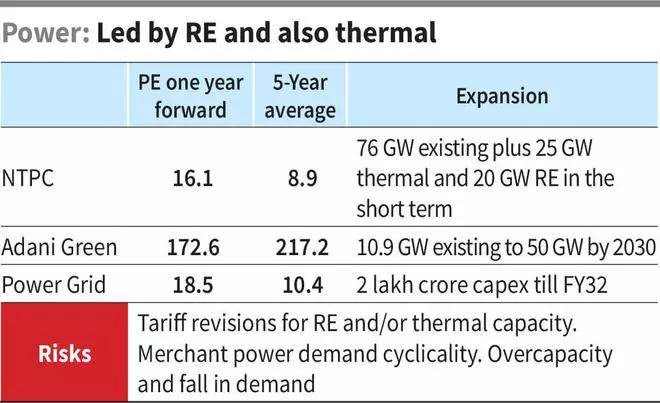

Energy: Double by 2030

The Central authorities has a transparent goal of doubling energy technology capability to 900 GW by 2030. It additionally envisages that half of that demand be met from Renewable Power (RE). With a transparent goal as such comes a beneficial coverage combine as nicely. This began with the ₹3 lakh crore energy bundle introduced in FY21 Finances to clear dues, good metering and financing of the venture to enhance credit score metrics at discoms and an excellent tariff visibility making certain 15.5 per cent RoE for normal and 17 per cent for hydro tasks.

The present run charge appears wholesome to safe the targets. The present RE capability stands at 44 per cent of the entire 442 GW, and, for the primary time, thermal share in put in capability dipped beneath 50 per cent in Might 2024. The incremental capability addition in FY24 was 76 per cent RE, which suggests a wholesome PPA signing and/or service provider demand. The highest three gamers by market capitalisation additionally point out the same momentum in capability addition.

NTPC accounts for 17 per cent complete put in capability in India at 76 GW and has plans so as to add 60 per cent extra capability within the medium time period. Consistent with the nationwide plan, RE will account for a big portion of the addition. The three.6 GW RE capability on floor will develop with the 8.4 GW in development and 11.2 GW beneath tendering course of in dedicated a part of the plan. Land financial institution to accommodate one other 11 GW addition has additionally been recognized.

General, NTPC plans on an RE put in capability of 60 GW by 2032 and should look to listing its RE subsidiary with a recent issue-based IPO and retaining its management. The thermal phase will proceed with 15.2 GW enlargement into account for tendering, along with 9.6 GW thermal capability already beneath development. The ₹3-lakh crore market capitalisation firm is seeking to spend 5-10 per cent of that yearly for the following three years in capex.

Adani Inexperienced, because the title implies, is turbo-charged on RE-based energy technology, together with photo voltaic, wind, and even pumped hydro storage. After including 25 per cent to its present capability, Adani Inexperienced exited FY24 with 10.9 GW capability. The corporate appears to be like so as to add 6 GW in FY25 and is focusing on 50 GW complete capability by 2030. This contains the 30 GW venture at present beneath manner at Khavda, the biggest single-location RE facility unfold throughout 538 sq km and anticipated to be commissioned by FY29.

With a 75 per cent working margin on ₹10,000 crore income (Q4FY24 exit charge), a robust group assist for elevating funds, Adani Inexperienced is assured of tying up funds and provide infrastructure and land financial institution for the venture. On the slower PPA tie-ups, the corporate expects that demand from service provider facet in view of decarbonisation regime ought to guarantee an above-average profitability.

With technology scaling, so would transmission. Energy Grid, which accounts for half of the nation’s energy transmission, has focused ₹2 lakh crore of capex until FY32. The corporate has present tasks value ₹86,700 crore in progress in March 2024 and expects to double capitalisation charge to ₹15,000 crore per yr from FY25.

Metal and Cement: Buoyed by GDP development

The tailwinds for cement and metal are secondary demand from the broad financial development in India. The Nationwide Infrastructure pipeline tasks of $1.2 trillion, 50,000 km of highways together with devoted freight corridors by 2030, four-lane highways and state highways, upgrading railways with high-speed service, authorities capex cycle (though tapering) and renewed give attention to reasonably priced housing are the broad macro tailwinds that include coverage assist.

Rising urbanisation and connectedness, vehicle demand, and growing disposable earnings are the fixed drivers, that are at an elevated state in final three years. Each metal and cement industries are cognizant of the low double digit development in anticipated demand within the subsequent decade. Whereas natural development plans are in place, consolidation primarily in cement has additionally been a continuing function.

Whereas demand is a key driver, commodity prices additionally affect these sectors. Power prices are mildly waning led by coking coal which ought to cushion earnings in FY25. Completed metal and cement costs are additionally low however can anticipate marginal enchancment with demand.

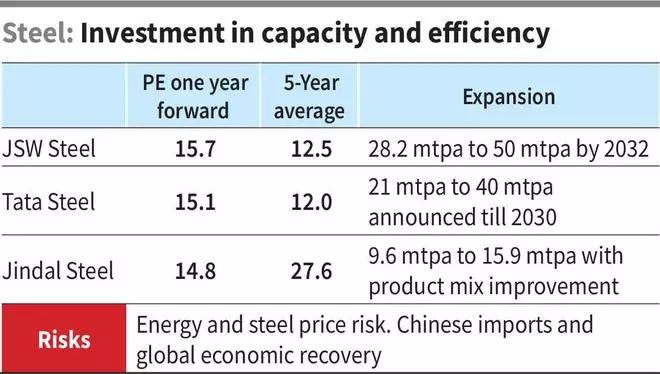

Substantial enhance in metal capability

Metal consumption in India grew 14 per cent YoY in FY24 to succeed in 136 mtpa and is predicted to drive trade gamers’ enlargement plans.

Jindal Metal and Energy expects to take a position ₹7,500-10,000 crore per yr over the following two-three years to extend its capability from 9.6 mtpa to fifteen.9 mtpa each year by 2030. It’s also targeted on bettering its product combine from semi-finished to completed merchandise throughout the identical enlargement plan and has secured 64 per cent of its income from such merchandise in FY24. The corporate, and broadly the trade, can be targeted on securing uncooked materials provide strains in coal mines, auctions and iron ore linkages.

Tata Metal has two broad divisions, Europe and India. Growth plans are squarely targeted on India, with consolidated capability anticipated to succeed in 40 mtpa by 2030 from 21 mtpa reported in FY24 finish. The European operations, that are loss making, are in for a makeover too. The corporate plans to take a position Euro 725mn €725 million together with the UK authorities’s €500 million contribution for the modernisation venture by shifting from coal furnace (slowly shutting down) to electrical arc furnace utilizing scrap metal.

JSW Metal will make investments the equal of 30 per cent of its present market cap or ₹65,000 crore within the subsequent three years to extend its capability to 50 mtpa by 2032, from 28.2 mtpa now. Since a big portion of the venture is brownfield enlargement, with coal and iron ore linkages, the headwinds to execution are decrease. The corporate has acquired a coal mine in Mozambique and extra iron ore mines in Karnataka, Odisha and Goa to complement its backward integration. It expects to enhance its output by 8 per cent in FY25 itself, having commercialised two enlargement tasks in FY25.

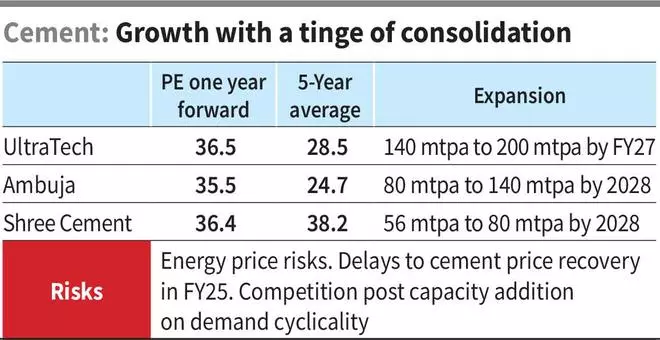

Cement: Race to consolidate and broaden

Consolidation of smaller entities has develop into a vital software for bigger firms of their quest to broaden operations. Classic vegetation, excessive competitors in South and West markets and strained liquidity positions to both broaden or service present demand are the headwinds to smaller operators. The elevated price of coal and suppressed cement costs have hit profitability of smaller operators with lower than 15 mtpa capability.

Scale is important to safe uncooked materials provide chains, and investing in logistical, manufacturing or advertising efficiencies. Penna and Sanghi Cement acquisition by Ambuja and Kesoram and India Cements (23 per cent non-controlling stake buy) by UltraTech Cement are current examples. The transaction vary at $80-100 per tonne signifies the competitors amongst acquirers greater than the profitability or scale of the sellers at present.

UltraTech Cement, the biggest operator, additionally has the biggest enlargement plan. From 146 mtpa capability, the corporate expects to succeed in near 200 mtpa by FY27. This contains current acquisition of Kesoram’s 11 mtpa, greenfield enlargement of 20 mtpa and brownfield enlargement of seven mtpa within the subsequent three years. The capex anticipated is at ₹10,000 crore for every of subsequent two years.

The Adani Group, through Ambuja Cements has introduced an enlargement plan of accelerating its capability to 140 mtpa by 2028 from the present 80 mtpa capability and reaching 100 mtpa by FY26 as a mid-term goal. The current Penna and Sanghi integration to play a component aside from natural enlargement. The corporate is web debt free and nicely positioned to fund the 65,000 crore capex until FY28. With group firms in energy technology, price financial savings from captive energy technology can be a part of its enlargement plans.

Shree Cement, reputed as a worthwhile operator, additionally plans for sturdy enlargement. The corporate will make investments ₹4,000 crore per yr for the following three years to extend its capability from 56 mtpa to 80 mtpa capability. The capex can be aimed toward inexperienced vitality, captive coal mining, and elevated rail freight combine to retain its low price operator standing together with the topline enlargement.

Conserving in thoughts capability expansions, a robust undercurrent of demand and coverage assist for capex push, bl.portfolio has been writing on shares on this house within the final 1-2 years. Now we have excellent ‘accumulate’ calls in Jindal Metal, NTPC and JSW Metal and ‘maintain’ calls on Tata Metal and Extremely Tech cement. Our ‘accumulate’ name on Energy Gird in January 2024 although was adopted up with a ‘partial e book revenue’ just lately. Whereas tailwinds are sturdy, valuation enlargement outpacing earnings development additionally must be watched.

#NTPC #Adani #Inexperienced #JSW #Metal #Tata #Metal #Ambuja #Cement #Ultratech #capex #plans #driving #Indias #core #sectors