Nonetheless, if you take a look at the inventory on a three-year foundation, RIL with 11 per cent CAGR returns (together with the worth of demerged Jio Monetary Companies), has underperformed Nifty 50 which has delivered CAGR returns of slightly over 14 per cent in the identical time interval. This nevertheless is nothing to stress about. The inventory of RIL has sometimes tended to underperform at any time when the corporate has been in a heavy funding part, one thing that it has launched into in its inexperienced power ventures.

With the inventory nonetheless leaving some cash on the desk at present ranges, long-term traders can accumulate it on dips for 4 causes — one, cheap valuations; two, being at pole place in India’s high-growth digital and retail enterprise; three, potential for large-scale worth creation, just like its digital and retail forays, within the renewable power area (not mirrored in present valuations); 4, secure O2C enterprise.

Progress engines

The launch of Jio’s knowledge providers in 2016, maturation of the retail enterprise and subsequent stake gross sales in FY21 had been the important thing catalysts that drove the inventory’s outperformance within the final six years. Though there has already been a big re-rating in valuation the markets have assigned to each companies, scope for additional outperformance from these companies stays, given the chance forward.

Reliance Jio: For one, with Reliance Jio rising as the biggest telecom providers firm in what is basically a duopolistic market (given survival points at Vodafone Concept) in India, the expansion potential stays sturdy as 5G will drive advances over the subsequent few years and new 5G enabled use circumstances will create guzzling development in knowledge consumption, offering scope for greater ARPUs. Reliance Jio has choices throughout the spectrum of wi-fi, wireline/broadband, enterprise/cloud providers and allied retail/enterprise digital choices that make its providers sticky for patrons.

In such a situation, its dominant place in telecom together with second participant Bharti Airtel is probably going nicely entrenched for the foreseeable future in India’s digital ecosystem. These components place it advantageously to maintain or enhance its working margins in a rising trade.

Reliance Retail Ventures: From a modest 1,691 shops in FY14, the retail enterprise has grown to 18,040 shops (and over 66 million sq. ft of retail area) by FY23. Reliance Retail is the biggest participant within the nation within the organised retail section, working brick-and-mortar, e-commerce, money and carry, B2C, and B2B codecs throughout the retail provide chain. With a low 3 per cent share of the market, there may be scope for large enlargement from the mix of market share positive aspects and/in a high-growth market the place the consumption theme is selecting steam, pushed by development in per capita earnings.

For instance, within the US, organised retail big Walmart immediately has slightly over 10 per cent share of the retail trade. Whereas how precisely issues will pan out within the Indian retail trade is out within the open, this will present a perspective on the potential development for Reliance Retail.

In recent times, Reliance Retail enterprise has witnessed stable development with FY21-23 income and EBITDA CAGR of 38 and 50 per cent respectively fuelled by a mix of retailer additions, acquisitions (totalling to $1.2 billion) and its phygital mannequin with acquisitions akin to Netmeds, Clovia being digital manufacturers. Apart from attire, grocery and electronics, the corporate, by way of acquisitions, has gained foothold in newer segments akin to pharmacy (Netmeds), style (Zivame, Clovia) and D2C (City ladder), which is able to drive development within the medium time period.

With dominance in digital and retail ecosystem and scope to boost synergies throughout these, Reliance is strategically positioned to garner a superb share of the patron spending which is able to occur over the subsequent a long time with its client dealing with companies.

O2C & E&P

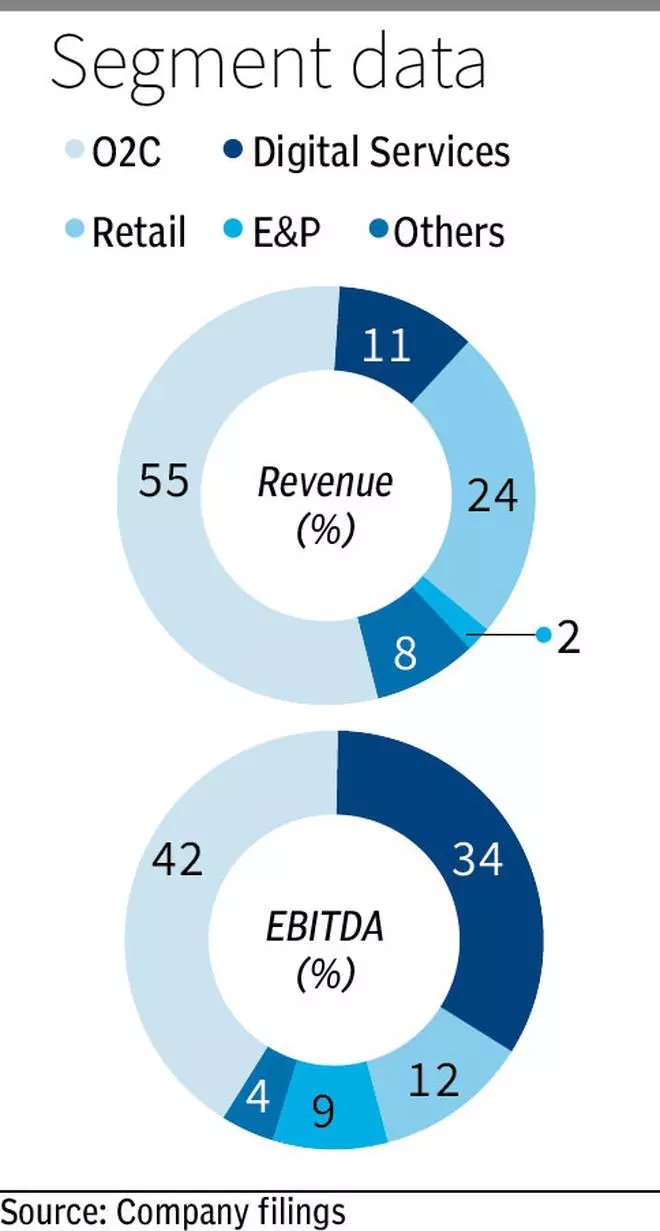

RIL’s conventional companies — O2C and exploration (E&P) — nonetheless account for 45-50 per cent of RIL’s consolidated EBITDA.

Spanning expansive refining and petrochemicals enterprise, the O2C enterprise efficiency might be unstable relying on developments in crude oil costs and refining margins. In occasions of excessive crude oil costs, greater refining and petchem margins have helped the general profitability. Equally, there have been occasions when, as a consequence of falling crude costs, refining and petchem cracker have been on a falling spree, thereby including to the stress on the general revenue efficiency. Reliance’s O2C enterprise has best-in-class margins and might not be similar to Indian refiners, given the size of operations, efficiencies and export focus.

Total, whereas it stays a big a part of the corporate’s enterprise, it won’t get the identical excessive valuation like RIL’s client dealing with companies. In reality, based mostly on worth assigned to this section by analysts, its total contribution to RIL’s valuation has not modified a lot from across the $75 billion it was estimated to be valued at when stake sale talks with Saudi Aramco had been ongoing in 2019. Scope for enhance in worth within the medium time period can come up from the corporate’s enlargement within the petrochemicals enterprise.

The E&P enterprise is small relative to total dimension of Reliance. Analyst estimates for its worth accounts for lower than 10 per cent of total RIL worth.

Subsequent huge factor

Traditionally any enterprise that RIL has put its weight behind has ended up being one of many largest gamers within the discipline and in addition managed to create loads of shareholder wealth.

On these strains, RIL has recognized inexperienced power as its subsequent development alternative. Because the world strikes away from standard fossil-based power sources, in direction of cleaner and sustainable power sources, the corporate is seeking to capitalise on the massive demand potential for renewable energy anticipated over the subsequent few a long time.

The corporate has dedicated a whopping ₹75,000 crore funding into constructing a complete inexperienced power and inexperienced materials ecosystem. At Jamnagar, it’s constructing a inexperienced power advanced unfold over 5,000 acres of land which, in line with the corporate, shall be among the many largest built-in renewable power manufacturing amenities globally. This can price it ₹60,000 crore, whereas the steadiness ₹15,000 crore is being invested in partnerships, constructing future applied sciences, worth chain to have the ability to construct an built-in renewable power ecosystem. The corporate has already made a number of investments in corporations which are engaged on inexperienced power applied sciences — akin to battery applied sciences, photo voltaic cells/panels, clear mobility options, software program instruments for photo voltaic power, and so on.

Whereas it’s up within the air as as to if inexperienced power investments will reap identical dividends as RIL’s telecom and retail forays, the nice factor for traders is that market is hardly assigning any worth to this enterprise at present ranges. Therefore, there may be scope for vital the wrong way up the years from this enterprise if the corporate repeats the success it has had in its different companies.

Valuation

Reliance Industries presently trades at 24 occasions its trailing twelve-month earnings. Whereas that is above RIL’s pre-Covid three-year common valuation of round 20 occasions, given development delivered by telecom and retail companies put up Covid, there may be scope for additional re-rating.

SOTP: Reliance Retail Ventures, which is the flagship firm, is presently valued at about $100 billion (₹8.3 lakh crore), based mostly on current transactions. RIL has an 83 per cent stake in it.

Reliance Jio, which is the opposite vital section of Reliance’s enterprise, was valued at $63 billion again in 2020. Market assigned worth is $80–90 billion vary – 10 to 11x one-year ahead EBITDA, which isn’t costly. RIL has 67 per cent stake in it.

Including the worth of RIL’s stake within the above companies and round $75 billion (conservative and assumes no change in worth in final 5 years) for its O2C enterprise, the enterprise worth for Reliance works out to round $214 billion. This excludes worth of its E&P enterprise and its media companies and a few worth in its monetisable actual property. This additionally assigns zero worth for its inexperienced power enterprise. RIL has web debt of round $15 billion. Adjusted for debt, its valuation is round $200 billion, which matches its present market cap. Including worth of E&P, and excessive potential for large-scale worth creation from inexperienced power enterprise, there may be some cash left on the desk for long-term traders who can accumulate the inventory on dips.

At a time when small and mid-cap inventory valuations are buying and selling at dizzying valuations, giant caps like RIL could also be safer bets for the long run.

Why

Potential worth of inexperienced power enterprise not mirrored

#Reliance #Industries #Inventory #Underperformed #Nifty #Years #Time #Purchase