We analyse the highest 4 PSU segments based mostly on inventory returns within the final 12 months and attempt to map them to the adjustments in coverage, the present demand setting, and the monetary strengths.

Aerospace defence and shipbuilding

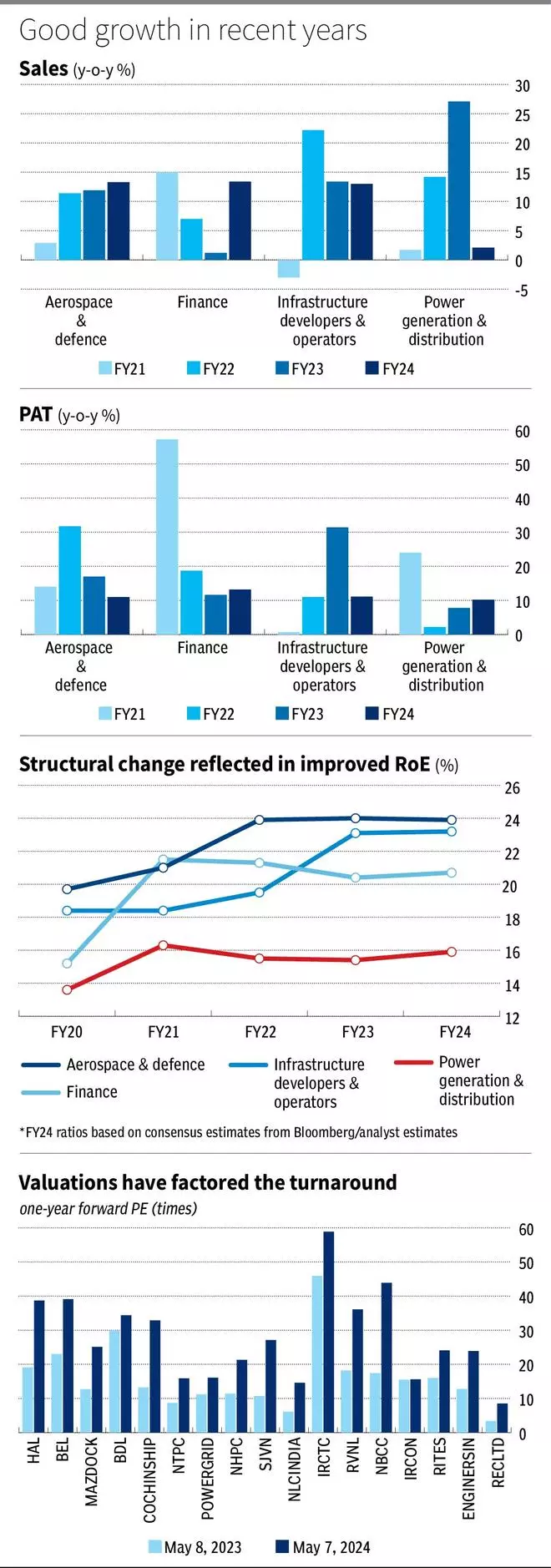

Below the aegis of Atmanirbhar Bharat (self-reliant India) and Make In India, there’s an effort to encourage indigenous design, growth and manufacture of defence tools. Not solely has the Defence procurement price range elevated 20 per cent YoY in FY24 to ₹1.72 lakh crore, but additionally beneficial insurance policies have allowed home PSUs the next share within the defence procurement pie.

So as of precedence, availability, and due concerns, the procurement shall want indigenously designed and developed merchandise with least preferance for globally developed merchandise.

There’s additionally a Optimistic Indigenisation Lists which embargos imports of 209 Providers and a pair of,851 objects. The federal government has additionally deliberate for 2 Defence Industrial Corridors, one every in Uttar Pradesh and Tamil Nadu, to enhance the defence manufacturing ecosystem.

The PSUs that stand to achieve essentially the most from the adjustments are those with distinctive capabilities within the home house, together with navy plane (Hindustan Aeronautics), submarines and destroyers (Mazagon Dock), and Drone (Bharat Dynamics), and radars and sensors (Bharat Electronics).

The businesses have an enviable order ebook as properly. Hindustan Aeronautics has 3x order ebook (3 instances trailing revenues), which incorporates 83 Mild Fight Plane-Mk1A or Tejas Mark-1A within the medium time period and creating Superior Medium Fight Plane (AMCA) and helicopters in the long term. BEL has 4x order ebook, which is diversified amongst Digital Warfare, Communications, Weapon System, and Radars. Mazagon Dock delivered 5 submarines in 2017-22 and its order ebook is at 4.5 instances. The corporate can be engaged on P76 class of submarines after P75 laying the bottom for future order ebook.

A big momentum so as influx and supply might be anticipated post-election. Cochin Shipyard, as an illustration, can anticipate additional readability on IAC 2 (air craft service), a repeat order of INS Vikrant, after elections, which is a ₹5,000 crore per 12 months contract for 10 years.

The phase is predicted to report 13 per cent progress in FY24 regardless of provide points from Israel and Russia. The phase continues with a excessive RoE of 24-23 per cent owing to improved asset utilisation of 4.3 instances for FY24 from 3.3 instances in FY20.

The phase valuations have doubled over the previous 12 months, reflecting the structural adjustments. However the premium valuations are usually not factoring threat of challenge execution on the present phases. Buyers might accumulate the shares working in high-end applied sciences, that are in a progress trajectory, however at cheap valuations that issue for dangers.

Energy technology and distribution

The central coverage on energy has set targets on total capability, renewable vitality share and limiting losses and enhancing effectivity. India peak demand grew from 119 GW in 2009 to 221 GW in 2023-24 at a CAGR of 4.5 per cent. However the Energy Ministry expects progress at 7 per cent CAGR progress for the subsequent decade as peak demand is predicted to develop to 366 GW by 2031-32 (Electrical energy survey).

The established capability has to go as much as 900 GW, from about 417 GW at this time, greater than doubling its capability, which is round 10 per cent CAGR progress. At the moment, fossil-based energy technology capability accounts for 57 per cent, primarily pushed by Coal (50 per cent). Renewable vitality (RE) accounts for 41 per cent of the put in capability, together with solar energy (16 per cent), Hydro (11 per cent), and wind (10.3 per cent).

The federal government has additionally mandated that fifty per cent of the cumulative electrical energy put in capability ought to be from non-fossil fuel-based vitality sources by 2030. This suggests that the longer term energy technology might be closely tilted in direction of RE-based technology. Whole put in thermal energy capability is predicted to be 283 GW and non-fossil-fuel-based capability to be 500 GW by 2031-32, in line with Energy ministry.

On the tariff aspect, there’s coverage continuity. Reimbursement is predicated on cost-plus mannequin with a goal of 15.5 per cent RoE for thermal tasks and 17 per cent for hydro, which was lately revised upwards to incentivise manufacturing.

On the manufacturing aspect, NTPC accounts for 17 per cent of the full put in capability with 73 GW in FY24, which it plans to extend to 120 GW by 2030-31, of which 60 GW might be from RE. It is a 7.3 CAGR progress visibility in capability. NTPC might be commercialising 16 GW within the subsequent 3-4 years and on the RE entrance, NTPC has 3.3 GW current RE capability, 7.8 GW below building and 11.9 GW in pipeline.

NHPC accounts for 15 per cent share of put in Hydro capability within the nation. However owing to greater RE focus, the capability addition for NHPC is at a quicker tempo. In comparison with 7 GW of put in capability, NHPC has 10 GW below building and seven GW below clearance stage. This could triple its capability on commercialisation within the subsequent 10 years with a capex outlay of ₹10,000 crore per 12 months.

Energy Grid, which has a 67 per cent market share in transmissions, is equally invested in growth. The corporate is ₹1.9 lakh crore capex outlay until 2032 of which a big half is interstate (₹1.2 lakh crore). The following three years capex outlay is at near ₹50,000 crore, implying a powerful head begin.

The sector is predicted to ship income progress of two per cent in FY24, however that’s on a excessive base of final two years when revenues expanded by 22 per cent per 12 months. Regardless of this, the phase reported a ten per cent PAT progress owing to decrease leverage prices as Web debt to EBITDA decreased from 4.1 in FY20 to three.7 instances now and improved asset utilisation, which improved 31 per cent from FY20. The RoE of the sector, at 15.9 per cent, is inching up through the years. The three shares are buying and selling at a mean 18 instances ahead earnings (1.7 instances final 12 months valuation), the sector shouldn’t be at a premium to personal gamers. The robust scope of growth doesn’t share the identical threat of execution as defence corporations however solely timing threat.

Energy Finance

Energy Finance Company and Rural Electrification Company are two main financiers to energy corporations. The give attention to greater share of RE energy technology whereas sustaining thermal energy implies the next financing want. The big capex outlay to push the RE energy implies a capex outlay of greater than ₹2 lakh crore, of which a 3rd or extra have to be supported by credit score.

The financiers have strengthened lending norms, which is mirrored within the NPA ratio contracting to round 1 per cent for each corporations beginning, from greater than 3 per cent in FY20. All of the whereas the businesses have maintained a wholesome yield (NIM) of greater than 3.5 per cent.

The wholesome metrics are partly pushed by Late Cost Surcharge (LPS) and Revamped Distribution Sector Scheme (RDSS). RDSS, launched in July 2021, goals to enhance credit score requirements at Discoms in evaluating their prospects with assistance from sensible meters. The LPS permits for concrete motion on late funds from discoms. Together with well timed subsidies and receipts from the state governments and the above laws, the monetary well being of energy provide chain has boosted progress and profitability metrics for financiers.

The phase has reported 13.4/13.2 per cent YoY income and PAT progress in FY24 and the RoE has improved to 21 per cent for the sector. With a valuation of 1.6-2.3 instances value to ebook worth, the shares are usually not priced at a premium. The credit score progress visibility, a powerful management on credit score prices and engaging yields at a decrease valuation suggest that Financier PSUs ought to curiosity traders.

Infrastructure and Railways

Railways budgetary allocation and coverage assist have been on a excessive, though briefly on maintain in view of the elections. After a big 48 per cent enhance in FY23 (albeit on a decrease base), the railway price range elevated by 6 per cent in FY24 as properly and is now at ₹2.6 lakh crore. Allocation to rolling inventory and new traces has equally saved tempo.

Whereas the sooner Devoted Freight Hall (DFC) is nearing monetary completion (90 per cent as of December ‘23), a number of different tasks totalling 3,500 km are below numerous phases of challenge planning as an extension of the DFC. The Centre will implement three main financial railway hall programmes focusing on vitality, minerals and cement corridors the main points of which ought to crystallise within the post-election Funds session.

The Nationwide Rail Plan continues to be on observe to extend share of rail visitors in freight to 45 per cent by 2030, from the present 21 per cent, by enhancing common velocity to 50 kmph from the present 37 kmph.

Additional, on the passenger aspect, with the preliminary success from Vande Bharat, different bogies can’t be behind. Over the subsequent 5 years, the Railways Ministry is planning to overtake 40,000 prepare bogies to offer a greater passenger expertise just like that of the Vande Bharat trains. All the train is predicted to price ₹15,200 crore.

RVNL, RITES and IRCON have gained considerably owing to coverage emphasis and investor pleasure round authorities initiatives. RVNL order ebook is at 3x income and, extra importantly, the order wins in 9MFY24 are a diversified mixture of rail — 20 per cent, metros — 26 per cent, irrigation — 14 per cent and energy —30 per cent. Vande Bharat and metropolis metro tasks will proceed to drive revenues for RVNL as connecting seven extra cities is below execution. Worldwide tasks in Uzbekistan, Kyrgyzstan and UAE-Saudi Arabia (below a JV) will add geographic diversification as properly.

IRCON is anticipating to double revenues within the subsequent fiveyears with mixture of Rails/ Roads & Highways (HAM) tasks in execution. Order ebook confronted sluggish progress in FY24 and is predicted to be at 2x FY24 revenues as geopolitical tensions and delay as a consequence of elections have impacted order ebook progress. However over long term IRCON is excessive velocity prepare corridors which resonates with the Nationwide Rail Plan.

The phase financials present an identical enchancment in return metrics. The valuations have equally doubled for the sector except for IRCON, which continues to commerce at 16 instances ahead earnings . Whereas the phase might be in focus post-election with a renewed price range and proposals getting clearance, the excessive valuations particularly within the case of RVNL may hinder any additional appreciation for now.

#RVNL #IRCON #HAL #PFC #REC #Powergrid #NTPC #NHPC #PSU #rally #structural #momentum