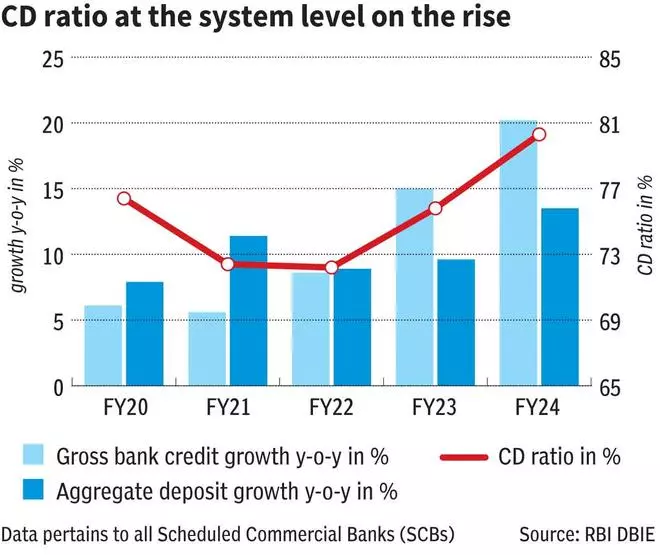

This comes on the again of deposit progress (on a YoY foundation) of all of the Scheduled Industrial Banks (SCBs) put collectively coming in at charges considerably decrease than that of charges of credit score progress for the previous two FYs. And it confirmed within the CD ratio (Credit score as share of Deposits) steadily rising to cross 80 per cent as of FY24 finish.

The implications

CD ratio shouldn’t be a statutory ratio to be maintained at prescribed ranges by banks. The perfect CD ratio can range from case to case. However normally, banks may be higher off sustaining a CD ratio between 70 and 80 per cent ranges, after accounting for CRR (Money Reserve Ratio) at 4.5 per cent, SLR (Statutory Liquidity Ratio) at 18 per cent and for LCR (Liquidity Protection Ratio) necessities.

With respect to particular person banks, these with CD ratios at elevated ranges will face twin challenges. For one, their credit score progress might be curtailed, until they’re able to mobilise deposits. It may be understood from the convention calls of banks that there’s sturdy demand for wholesale loans and the aggressive depth is excessive in that house. Banks with overheated CD ratios could have their arms tied, unable to capitalise on the chance. This may ultimately imply lack of market share and potential revenue.

Second, banks could also be pressured to lift rates of interest on deposits to mobilise deposits. Or in any other case, pressured to borrow available in the market, within the occasion of deposits not flowing by way of. Usually, the price of such borrowings is greater than the price of deposits. This may trigger a compression of their NIMs (Internet Curiosity Margins), within the occasion of not with the ability to cross on the upper value to debtors. Consequently, NIMs might come beneath strain, going ahead.

How are high banks positioned?

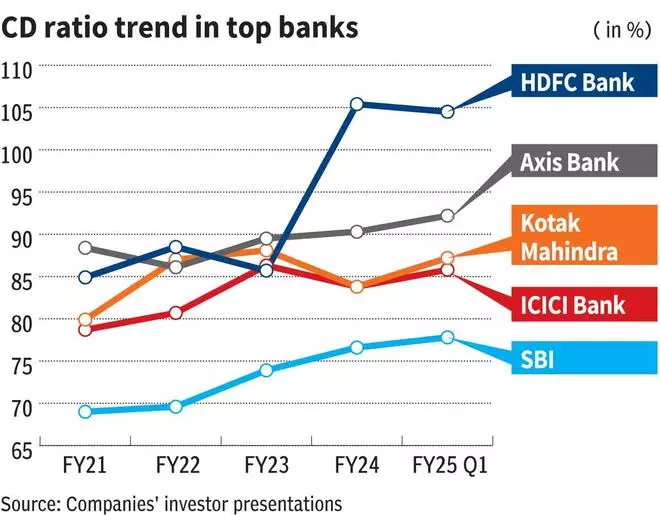

As seen within the chart, the CD ratios of the highest 5 banks (by way of market cap) have been on an increase proper from FY21. A few of these banks have witnessed CD ratios just like present ranges previous to FY20. Nevertheless, given the ratios’ growing development lately might ‘probably expose the banking system to structural liquidity points’, the Governor has flagged issues.

Of the lot, HDFC Financial institution has the best CD ratio. The financial institution has had a CD ratio of over 105 per cent ever because it inherited the loans of erstwhile HDFC Ltd, because of the merger between them. Axis Financial institution is the following to comply with. SBI appears to the one that’s comfortably positioned of the lot.

Throughout the quarter passed by, all of the 4 personal lenders registered wholesome mid-teen YoY progress in deposits (deposit progress on an ex-merger foundation is taken into account for HDFC Financial institution), beating the system-level progress price of 11 per cent. SBI lagged with an 8 per cent progress price. Regardless of the wholesome exhibition of deposit progress, the CD ratios stay elevated, because of the additionally wholesome credit score progress.

An evaluation of the administration commentaries of those banks signifies a few frequent tendencies — optimism round deposit progress with out a rise in rates of interest and warning in credit score progress, going ahead. This aside, RBI had launched draft tips on elevated LCR from April 1, 2025, primarily based on the proportion of deposit accounts with entry to web or cellular banking. With the opportunity of this materialising and the upcoming price cuts, it stays to be seen if banks can showcase progress whereas additionally holding on to their NIMs. This might be one of many key monitorables for banking shares over the following few months.

#SBI #HDFC #Financial institution #ICICI #Financial institution #Axis #Financial institution #Kotak #Financial institution #Key #Monitorable #Banking #Shares