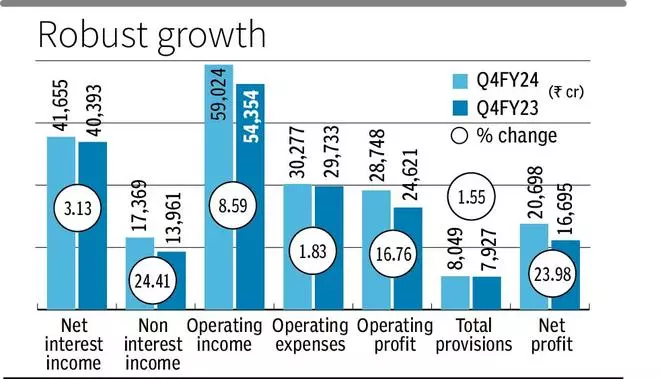

India’s largest financial institution had reported a internet revenue of ₹16,695 crore within the year-ago quarter. Internet revenue within the reporting quarter is up about 24 per cent year-on-year (y-o-y) and about 126 per cent sequentially.

The financial institution’s central board, at its assembly on Thursday, declared a dividend of ₹13.70 per fairness share of ₹1 every totally paid up for FY24.

Internet curiosity earnings/NII (distinction between curiosity earned and curiosity expended) was up 3.13 per cent y-o-y at ₹41,655 crore (₹40,393 crore).

Whole non-interest earnings, comprising charge earnings (mortgage processing expenses, miscellaneous charge earnings, and so on), foreign exchange earnings, revenue or loss on sale/revaluation of investments, and so on, rose about 24 per cent at ₹17,369 crore (₹13,961 crore).

Working earnings (NII plus non-interest earnings) development of 8.59 per cent y-o-y (₹59,024 crore), outpaced working bills (worker price and different working expense) development of 1.83 per cent y-o-y (₹30,277 crore), ensuing within the working revenue going up 17 per cent to ₹28,747 crore.

Mortgage development and NPAs

SBI Chairman Dinesh Kumar Khara expects FY24’s mortgage development to be sustained in FY25 and internet curiosity margin maintained on the present degree. In FY25, the lender expects 14-16 per cent development in loans (15.24 per cent in FY24) and 12-13 per cent in deposits (11.13 per cent).

He noticed that the financial institution has a sanctions pipeline of ₹4-lakh crore, with non-public sector entities accounting for 75 per cent of those sanctions and public sector accounting for the remainder. Surplus holding of statutory liquidity ratio securities stood at ₹3.5-lakh crore.

Whereas the present capital adequacy ratio (14.28 per cent as at March-end 2024) is ample to assist as much as ₹7-lakh crore of steadiness sheet development, the financial institution is open to lift fairness capital, Khara mentioned.

Internet curiosity margin (entire financial institution) declined to three.28 per cent within the reporting quarter from 3.37 per cent a yr in the past.

Provisions for workers declined about 28 per cent y-o-y within the reporting quarter to ₹5,225 crore.

Whereas mortgage loss provisions shot up 156 per cent to ₹3,294 crore, the financial institution obtained write-back from commonplace belongings provisions (₹370 crore) in addition to from different provisions (₹1,306 crore).

Asset high quality improved, with gross non-performing belongings (NPAs) declining to 2.24 per cent of gross advances as at March-end 2024 towards 2.42 per cent as at December-end 2023. NNPAs nudged decrease to 0.57 per cent of internet advances from 0.64 per cent.

As on March-end 2024, gross advances elevated by 15.24 per cent y-o-y to ₹37,67,535 crore, with sturdy development throughout all segments. RAM (retail, agriculture and MSME) and company advances crossed ₹20-lakh crore and ₹11-lakh crore, respectively.

Whole deposits rose 11.13 per cent to ₹49,16,077 crore. Low price present account, financial savings account (CASA) deposits declined to 41.11 per cent of home deposits towards 43.80 per cent.

#SBI #posts #report #revenue #rise #earnings #leash #spend