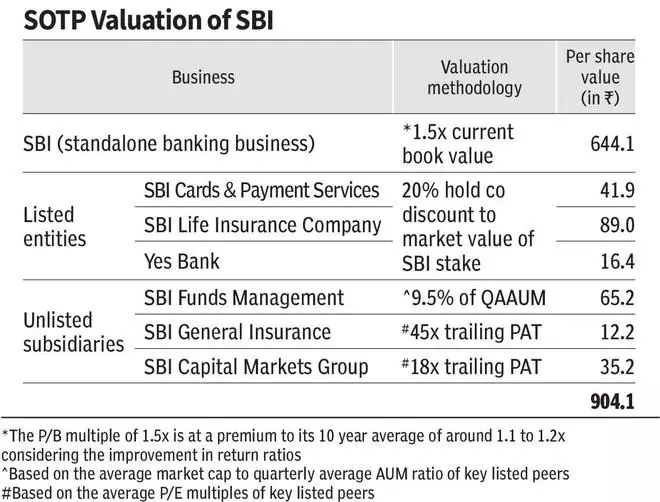

The financial institution has displayed exemplary efficiency within the final 5 years, recovering from the misery of the pandemic years. It has now advanced to exhibiting scale as a public sector financial institution would and effectivity as a personal financial institution would. The share value has captured it properly, rising over 5 occasions from the lows of Could 2020. Going by a conservative sum of the elements valuation, there’s room for an upside, that leaves traders with a chance to revenue when collected on dips.

Whereas a few of its friends wrestle with excessive credit-deposit ratios (CDRs), SBI enjoys an edge over them, with its CDR as little as 77.8 per cent (together with home and international operations). Because of this mortgage development for SBI shouldn’t be a trouble, relative to its friends. With the stake-sale of Sure Financial institution in superior phases and the opportunity of subsidiaries getting listed within the medium-to-long time period, there might be appreciable worth unlocking.

Nonetheless, traders have to be cautious of the opportunity of a NIM (Internet Curiosity Margin) compression, pushed by greater price of funds, as a result of borrowings trending up. The financial institution has raised ₹38,100 crore in FY24 and ₹10,000 crore in FY25 thus far, by way of concern of debt securities. This aside, the board has accepted the elevate of one other ₹25,000 crore. Consequently, the debt to belongings ratio (standalone) has trended as much as 9.5 per cent as of Q1 FY25 from 8 per cent as of FY20.

Turnaround

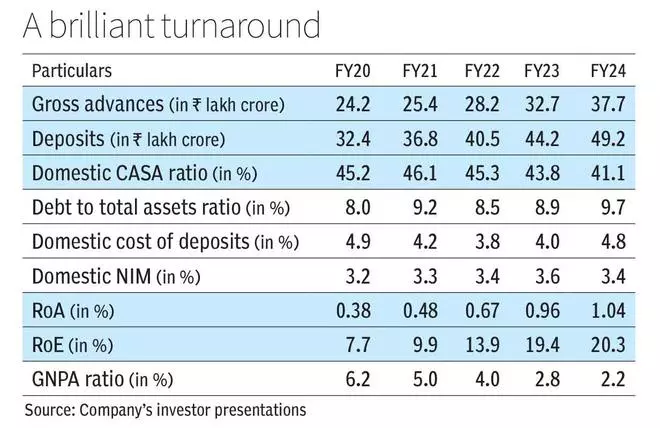

FY20 was a yr marked by a Gross NPA ratio of 6.2 per cent, credit score price (provisions and write-offs as a share of advances) at a whopping 1.9 per cent and a meek RoA (Return on Property) of 0.38 per cent. Since then, the financial institution has staged a superb turnaround, pushed by large enhancements in asset high quality.

GNPA ratio within the agri, SME and company portfolios have been introduced down from 16 per cent, 9.4 per cent and 9.7 per cent (FY20) to 9.6 per cent, 3.8 per cent and a couple of.5 per cent (FY24) respectively. Credit score price has declined from 1.9 per cent (FY20) to 0.3 per cent (FY24). The slippage ratio has improved considerably and the price to revenue ratio has trended downward to under 50 per cent in FY24 (excluding wage revision and one-time gadgets) from 52.5 per cent in FY20. Consequently, web revenue has grown over 4 occasions and RoA and RoE have risen from 0.4 per cent and seven.7 per cent to 1 per cent and 20.3 per cent respectively between FY20 and FY24.

These enhancements in effectivity have come not at the price of development although. Each credit score and deposit growths have are available at a CAGR of about 11 per cent between FY20 and FY24, that are at par with the expansion charges posted by all scheduled banks collectively.

All just isn’t rosy although. The NIM (home), which reached a peak of three.6 per cent in FY23, has been trending downward since. It is because, price of deposits (home) which bottomed out at 3.8 per cent in FY22, has risen to five per cent as of Q1 FY25. An examination of the deposit profile reveals that the expansion in deposits talked about above has been pushed largely by time period deposits. Time period deposits have grown at 12.9 per cent CAGR, whereas the low-cost CASA (Present Account, Financial savings Account) deposits have grown at 8.3 per cent CAGR between FY20 and FY24.

Takeaways from Q1 FY25

The financial institution posted a very good set of numbers in Q1 FY25. Credit score grew at 15.4 per cent yr on yr and deposits at 8.2 per cent. Nonetheless, home NIM tapered to three.35 per cent (3.22 for home + international) from 3.43 per cent (3.28 for home + international) as of This autumn FY24, owing to home price of deposits rising to five per cent (highest within the intervals analysed).

The administration is sanguine a few credit score development of 15 per cent in FY25, whereas maintaining the home CDR between 70 per cent and 72 per cent. Home CDR is at 69.3 per cent now (77.8 per cent together with international operations). Additionally they anticipate the NIM to remain at present ranges, with a ten bps variance. That is after contemplating the opportunity of price cuts.

A few elements can work in SBI’s favour right here. First, the financial institution has extra SLR (Statutory Liquidity Reserves) of ₹3.7 lakh crore (equal to 10 per cent of gross advances). Additionally, with the introduction of particular tenor deposits, the financial institution can comfortably develop the mortgage ebook, maintaining the CDR intact.

Second, a big proportion of the financial institution’s loans (36 per cent) is linked to MCLR (Marginal Value of Lending Charge) and MCLR-linked loans make the most important a part of the pie. What this implies is that, since MCLR pricing is predicated on the price of deposits, the financial institution can transmit the elevated price of deposits to debtors. The financial institution has additionally raised MCLR charges for varied tenors from 5 bps to 10 bps in July. This can assist defend the NIM, offered the price of current borrowings doesn’t play spoilsport.

Subsidiaries

The inventory of SBI derives substantial worth from its key subsidiaries, that are rising quickly (see accompanying desk). SBI Life Insurance coverage has delivered a 22 per cent CAGR in embedded worth and 19 per cent CAGR in gross written premiums between FY20 and FY24. SBI Playing cards & Fee Companies has grown its receivables by a CAGR of 20.5 per cent (FY20 to FY24) and web revenue at a CAGR of 18 per cent. SBI Mutual Fund hasn’t did not capitalise on the rising retail flows. Its QAAUM (Quarterly Common Property Underneath Administration) has exhibited a CAGR of 25 per cent (FY20 to FY24), and the corporate has saved its market management with a 17 per cent share. Its web revenue has showcased a CAGR of 36 per cent.

#SBI #Buyers