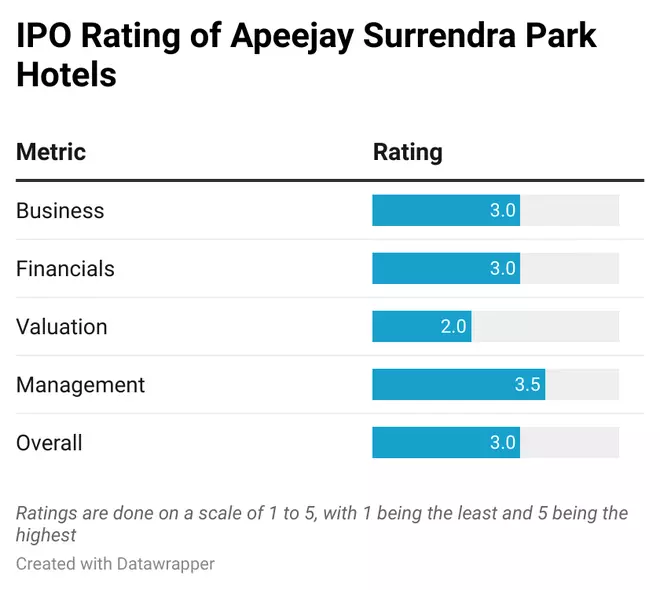

On this regard, the operator of a fairly well-known hospitality model, The Park chain of inns and different properties, Apeejay Surrendra Park Accommodations, has come out with an preliminary public providing of shares that closes on Wednesday (February 7). The corporate hopes to lift ₹920 crore from the IPO on the higher finish of the worth band (₹ 147-155), with ₹600 crore coming from recent problem of shares and ₹320 crore being supply on the market from present shareholders.

At ₹155, the supply trades at 63 instances the corporate’s trailing twelve months’ earnings per share on the post-offer fairness base. The worth to ebook on a TTM foundation is 2.8 instances for Apeejay Surrendra.

Listed firms within the resort’s house that cater to various clients at various value factors commerce at 75-100 instances their trailing 12-months’ per-share earnings and 4-10 instances on a price-to-book foundation..

Though the IPO appears priced cheaper than friends, absolutely the valuations aren’t cheap. Nevertheless, given the cyclical nature of the resort enterprise and the misery ranges from which they’re popping out post-COVID, the market has re-rated such shares strongly. Given the upswing within the economic system and rising spending on tourism, the sector appears set for a multi-year bull run; traders can subscribe to the IPO with a 2-3-year perspective.

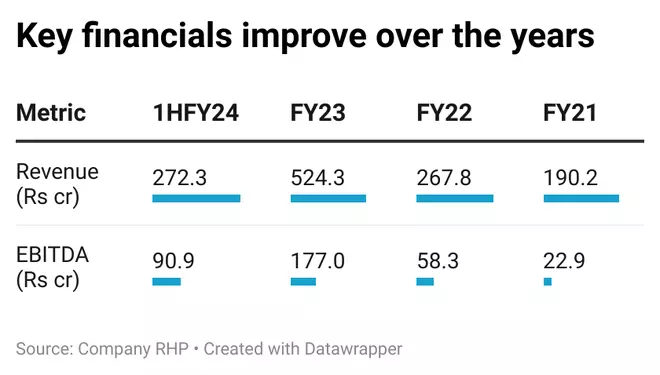

Between FY21 and FY23, the corporate’s income rose over 2.8 instances to ₹506.1 crore, whereas on the underside line, Apeejay Surrendra moved from internet losses to internet revenue of ₹48.1 crore in FY23. Within the first half of FY24, the corporate recorded revenues of ₹264.4 crore (up 16.8 per cent YoY) and internet revenue of about ₹23 crore (up 22.4 per cent YoY).

The corporate’s EBITDA margin of over 33 per cent in FY23 and 1HFY24 is kind of wholesome.

A enterprise mannequin that blends owned, leased and managed working modes for its inns, sturdy efficiency in key metrics – occupancy, common room price (ARR) and income per out there room (Rev PAR) – and wholesome traction within the meals & drinks section are positives for the corporate.

At an business stage, the return to ‘work from workplace’ mode for IT firms and huge corporates would spur enterprise journey. Home and inbound worldwide tourism-related journey additionally matches pre-COVID ranges and is predicted to develop quickly, whereas conferences, exhibitions, incentives associated to firms, and marriages resume their common course.

A lot of the difficulty proceeds (from the recent problem half) are set to go in the direction of repaying a bulk of its loans, additional strengthening the steadiness sheet for Apeejay Surrendra.

Profitable properties, sound metrics

Apeejay Surrendra runs The Park Accommodations with upscale luxurious choices; The Park Assortment supplies small luxurious at just a few journey locations; Zone and Zone Join supply higher mid-scale pricing; and STOP, the economic system motel.

The corporate has 30 inns in 20 cities with 2298 rooms. The income mainstay is the set of seven inns that it owns. Three inns are leased – from authorities authorities or non-public events. Then 20 inns are run through administration and operational contracts – managed mannequin.

This blended working mannequin permits the corporate the flexibility to be versatile in its method whereas sustaining model and high quality management and balancing the associated fee optimisation half.

Apeejay Surrendra’s inns have seen occupancies soar within the final 2-3 years. From 67.3 per cent ranges in FY21, occupancy rose to 91.77 per cent in FY23. Within the first half of FY24, the occupancy ranges are at practically 93.3 per cent, among the many finest within the business. Its properties in Kolkata, Navi Mumbai and Chennai have greater than 95 per cent occupancy, whereas the inns at Bangalore and New Delhi have over 93 per cent occupancy as of 1HFY24.

Common room charges have risen sharply, too, because the business took steep hikes to recuperate from the distressed ranges of 2020-22. From ₹3,250, the ARR has elevated to ₹6,059 for 1HFY24. RevPAR, too has adopted a equally sharp trajectory from ₹2,187 in FY21 to ₹5,652 as of 1HFY24.

The room charges are aggressive in comparison with others within the business ,although not among the many highest.

Apeejay Surrendra has additionally seen the meals & drinks contribution to revenues improve from 36 per cent in FY21 to 39 per cent in FY23, which is reportedly larger than the typical figures for just a few others within the business, in accordance with a Horwath HTL report cited within the RHP.

The corporate’s bakery and confectionary outlet, Flurys, which competes with CCD, Barista, and Theobroma, amongst others, has reported cheap EBITDA margins.

Mortgage reimbursement

Apeejay Surrendra has whole borrowings of about ₹597 crore as of September 2023. The web debt-to-equity ratio is round 1 . Nevertheless, with Rs 550 crore of the IPO proceeds set for use for repaying debt, the mortgage stage could be insignificant and so would the debt-equity ratio on an expanded base.

Based on a Horwath HTL report, international demand for inns in India would contact 100 per cent of pre-COVID ranges by FY25 and 130 per cent by FY27. Within the case of home demand, FY24 itself has seen a bounce of 12 per cent over pre-COVID ranges. Because the provide of rooms (8 per cent CAGR over FY24-27) would fall wanting anticipated demand (10.6 per cent CAGR over FY24-27), the pricing energy is about to stay agency for the resort business.

Thus, the business dynamics appear beneficial. The corporate is seeking to execute greenfield initiatives in Pune, Kolkata and Jaipur and dealing on increasing capability in Visakhapatnam and Navi Mumbai. Any inordinate delay in execution is usually a capability addition danger.

#examine #Apeejay #Surrendra #Park #Accommodations #IPO