BFL will pare its stake for ₹3,000 crore and have a post-issue holding of 88.75 per cent. The recent challenge proceeds of ₹3,560 crore shall be utilised for augmenting the capital base of the corporate.

BHFL has displayed a stellar run in its seven years of mortgage operations, with an AUM (property below administration) CAGR of 29.3 per cent between FY20 and FY24.

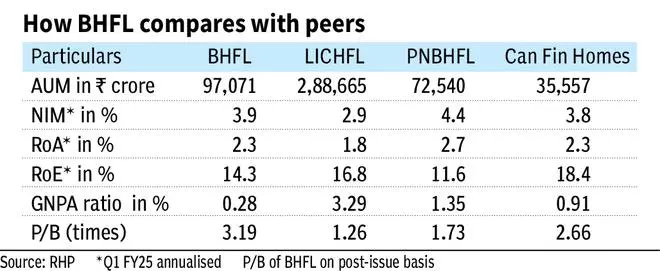

Its friends within the prime lending area equivalent to LIC Housing Finance, PNB Housing Finance and Can Fin Properties have CAGRs of between -3.9 per cent and 14 per cent for a similar interval (dwelling loans with ticket dimension of over ₹50 lakh are thought of prime. BHFL additionally has a smaller non-prime portfolio – inexpensive housing).

Surprisingly, such progress has not come at the price of asset high quality (see desk). Moreover, BHFL presents a diversified play vis-à-vis friends, who’ve little to no publicity to merchandise equivalent to LRD and DF.

As per the prospectus, the prime housing finance market accounts for 35 per cent of the general housing finance market, which is about ₹33 lakh crore. It (prime) grew at a CAGR of 20.1 per cent beating the general market (13.1 per cent) between FY19 and FY24. Its progress is anticipated to proceed at a CAGR of 21-23 per cent between FY24 and FY27 from ₹11.5 lakh crore to ₹20.9 lakh crore. With the robust ‘Bajaj’ model fairness, BHFL is properly poised to capitalise on this.

At 3.2 occasions P/B (worth to e-book) on a post-issue foundation, the difficulty is priced at a premium to friends (see desk). Nevertheless, its diversified play, increased mortgage progress over the previous couple of years and pristine asset high quality explains the premium.

- Additionally learn: SME IPO frenzy continues with 50 corporations submitting papers

That mentioned, BHFL continues to be a younger firm, faces stiff competitors from banks within the prime lending area, and is but to undergo cyclical downturns in a significant manner.

A attainable downturn within the bigger actual property market can adversely impression the worth of dwelling mortgage collaterals, decelerate offtake in developer loans in addition to hurt the LRD portfolio attributable to vacancies in industrial properties.

Additional, price cuts sooner or later may cause NIM (web curiosity margin) compression within the near-term. How BHFL navigates challenges equivalent to these, shall be one thing to be careful for. Traders with an urge for food for danger and long-term perspective can contemplate subscribing to the difficulty.

Enterprise and strengths

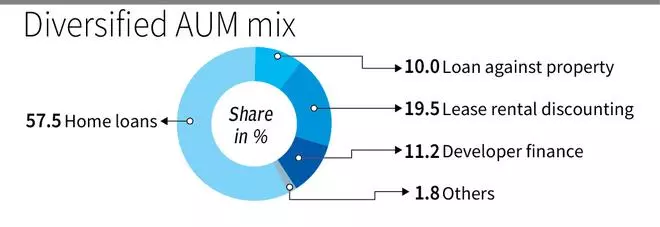

As seen within the ‘AUM combine’ chart, BHFL’s portfolio is diversified, not like friends. On the subject of enterprise, ‘secure and safe’ is the secret.

For example this, within the dwelling mortgage phase, 87 per cent of the debtors are salaried workers with a median annual wage of ₹14 lakh, and over 75 per cent of the debtors have a CIBIL rating of 750+.

Within the LAP phase, 71 per cent of the loans are secured by a self-occupied residential property and the LTV (Mortgage to Worth ratio) can also be low at 53 per cent. Within the LRD phase, the lessors are largely HNIs and international non-public fairness gamers letting out Grade-A industrial areas to outstanding Indian companies and MNCs.

This ends in the pristine asset high quality maintained by the corporate with its Gross NPA ratio properly under friends. To prime this, BHFL’s LRD portfolio has zero GNPAs.

A key power of BHFL is the symbiotic relationship it has with the actual property builders. When advancing loans to builders, it will get entry to the purchasers of such builders (dwelling consumers), and this makes for a big portion of direct sourcing of enterprise for the house mortgage product.

This aside, the financials are largely stable with a mixture of pace and stability. The online whole earnings (whole earnings minus finance value) and web revenue have clocked a CAGR of 35 per cent and 56 per cent between FY22 and FY24 respectively. AUM progress and asset high quality are as established earlier. BHFL additionally boasts of the best attainable credit standing (IND AAA/ secure, CRISIL AAA/ secure), leading to decrease value of funds.

BHFL has 215 branches throughout 23 States, although 90 per cent of the AUM is concentrated within the prime six States. The corporate additionally has a powerful digital presence. To call a couple of initiatives, it has a self-service DIY dwelling mortgage portal, a paper-free e-sanction letter system and a devoted cellular app for subject brokers. As of Q1 FY25, the corporate serves 3.2 lakh clients.

Factors to notice

Whereas nearly all loans superior by BHFL are floating price, solely 56 per cent of its borrowings are floating price, the remaining being mounted price.

This won’t favour the corporate, come price cuts. Additionally, given its borrower profile, BHFL has to compete with mainstream banks by way of pricing, to accumulate such clients (Banks have 86 per cent market share in prime housing finance). Which means a NIM compression could also be on the playing cards within the near-term attributable to yields coming below stress.

The administration (within the RHP) recognises this and aside from the pliability supplied by the diversified AUM, it has executed hedging methods with instruments equivalent to rate of interest swaps to cushion among the NIM compression. Whereas it has these measures in place, it additionally acknowledges the shortcoming to mitigate such rate of interest dangers, within the occasion of ineffectiveness of such measures.

- Additionally learn: Baazar Model Retail shares make flat market debut, ends day practically 3% increased

#Subscribe #Bajaj #Housing #Finance #IPO