The IPO measurement is ₹537 crore, out of which the contemporary problem a part of the pie is ₹200 crore. Of that, the corporate has earmarked ₹130 crore for capex, together with for organising 24 new COCO (Firm Owned Firm Operated) shops over the subsequent two years. That is other than an equal variety of FOFO (Franchisee Owned Franchisee Operated) shops anticipated to come back up, as per the administration. (Observe: The corporate doesn’t incur capex on any of its FOFO shops and it’s left to the franchisee). The promoters will maintain round 56.8 per cent stake publish problem (67.4 per cent pre-issue)

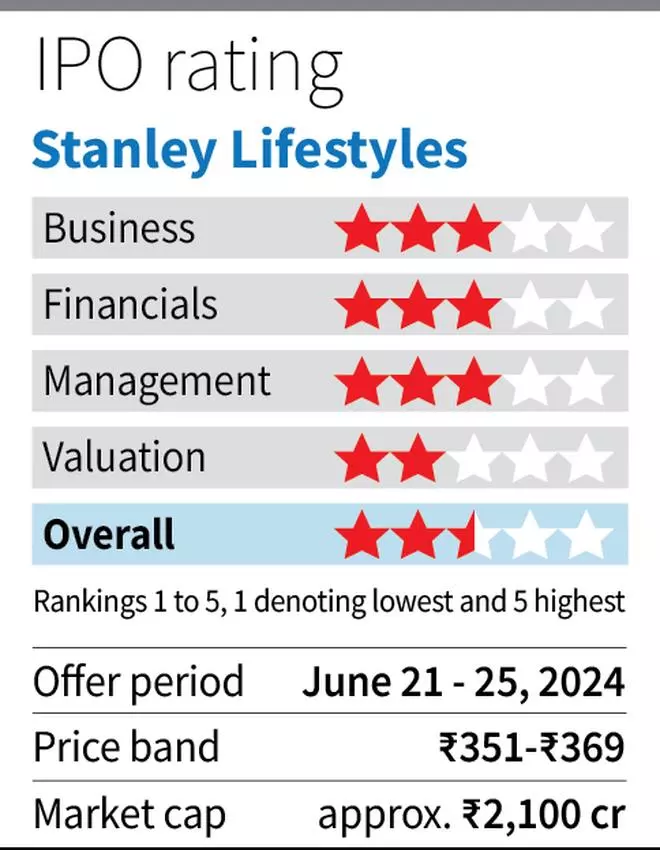

SLL has an excellent observe file in its enterprise and operates in a distinct segment area. Nevertheless, the IPO valuation at a trailing PE of 84 occasions (9M FY24 earnings annualised) seems too excessive and unattractive. That is particularly when contemplating the truth that income progress has slowed fairly considerably in FY24 and there are execution dangers in launching new shops and rising the enterprise. Therefore, we advocate that traders needn’t subscribe to the difficulty and wait to see how the enterprise performs over the subsequent few quarters.

SLL doesn’t have a listed peer and a considerable quantity of the competitors is from the sellers of imported luxurious furnishings, predominantly from Europe.

Strengths

SLL operates beneath two segments — B2C and B2B. Within the B2C section, which accounts for round 80 per cent of income, the corporate manufactures bespoke furnishings, reminiscent of sofas, recliners, eating tables, espresso tables, wardrobes, kitchen models, beds and mattresses, beneath three totally different value factors — particularly, tremendous premium, luxurious and ultra-luxury. The value level begins from ₹1.5 lakh to ₹5 lakh and past.

Within the B2B section, the corporate is engaged in contract manufacturing for residence furnishing MNCs and a big vehicle firm. The B2B section accounts for round 20 per cent of income.

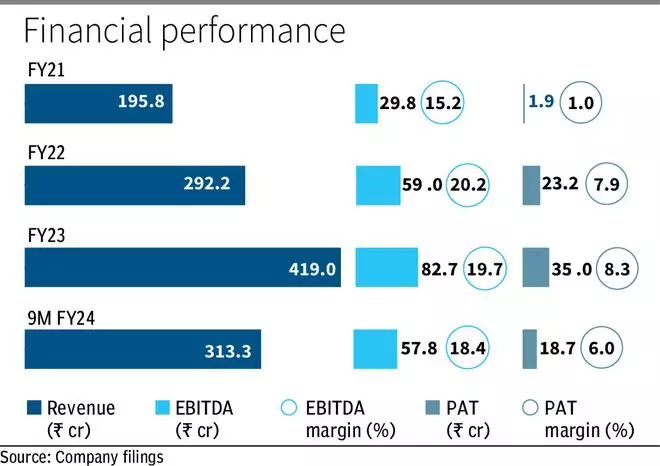

At the moment, SLL sells the manufactured furnishings in 62 shops, 38 being COCO and 24 being FOFO. For 9M FY24, COCO shops contributed 62 per cent to the full income, whereas the FOFO shops contributed a a lot decrease 13 per cent to the corporate’s general income. The whole retailer depend at 62 as of December 31, 2023, has elevated from 25 on the finish of FY21. A brand new retailer takes 4 to 5 years to mature (to achieve peak output), as estimated by the administration.

SLL’s key aggressive benefit lies in a vertically built-in enterprise mannequin, proper from dealing with procurement to delivering to retail. Specialising in bespoke furnishings, SLL contrasts with opponents who import from distant continents, providing agile lead occasions and flexibility to traits. This agility permits SLL to ship superior worth to prospects in comparison with its friends.

What works

The Indian housing market, significantly the luxurious section with models valued at ₹1.5 crore and above, has been in an upcycle. In accordance with Anarock, new launches in luxurious and ultra-luxury area, as a share of complete, have grown from round 10 per cent pre-pandemic to a peak of 27 per cent as of Q3 CY2023. The wealthy who flock to e-book such models are SLL’s goal prospects and when the booked models are delivered within the subsequent few years, the furnishings finances for these new models turns into the TAM (Complete Addressable Market) of SLL. The administration notes that 80 per cent of the corporate’s B2C enterprise comes from new development and solely the remaining is from refurbishing.

Additional, as per a RedSeer Report within the RHP, the variety of Indian prosperous households has grown twice between 2017 and 2022 and the luxurious PFCE (Personal Closing Consumption Expenditure) has grown at a CAGR of 26 per cent in the identical interval. The dimensions of the Indian luxurious furnishings market is predicted to outpace the expansion of the non-luxury market by 7 share factors to achieve ₹22,300 crore by FY27, from ₹6,700 crore (FY23). Additional, the organised sector market share, which was at 26 per cent in FY23, is projected to be 35 per cent by FY27.

SLL seems poised to piggyback on this rising luxurious spending by India’s wealthy.

These aside, the Authorities is in discussions with the business to implement PLI scheme for the furnishings sector. In December 2023, the DPIIT was reported to be working carefully with 24 sub-sectors, together with furnishings, to advertise import substitution. If profitable, this initiative might drawback opponents, whereas bolstering the corporate’s aggressive benefits.

What doesn’t work

Whereas the macro story is fascinating, there are dangers and different elements to think about right here. First is the slowdown in income progress in FY24. Income grew at a CAGR of 46 per cent, between FY21 and FY23, to ₹419 crore, rebounding from a low base in FY21 because of the pandemic. Estimated FY24 income (9M FY24 annualised/adjusted for seasonality) at ₹420-430 crore, represents a major slowdown with yr on yr progress at round 0-2.6 per cent.

Administration notes that FY24 numbers aren’t consultant of potential efficiency, due to delayed house handovers and disruptions resulting from retailer relocations and a hearth at one of many shops. Nevertheless, even when these are factored, which may clarify for 5-7 per cent lack of income, the expansion continues to be low.

Additional, the slowdown in progress that may be attributed to the delays and disruptions famous above, additionally factors to inherent enterprise dangers.

Amid the expansion slowdown, the asking valuation at a publish problem PE of 84 occasions (pre-issue PE of 76 occasions) is sort of expensive. Different dangers embrace the corporate being extremely depending on the luxurious housing market upcycle. Any dangers to the long-term sustainability of this upcycle would adversely have an effect on the corporate’s prospects.

Whereas the difficulty has priced in all the expansion alternatives, there are execution dangers so far as the scaling up is worried. Therefore, we advocate that traders acquire conviction first, most likely over the subsequent couple of quarters, and provides the difficulty a move for the second.

#Stanley #Life #IPO #Subscribe