Torrent Pharma and Dr.Reddy’s eyeing promoter stake in Cipla would possibly simply be the beginning of an acquisition spree within the pharma area. We consider Indian Pharma could now flex its monetary muscle for each large and small offers, with sectoral sentiments on a excessive, stability sheets robust and all enterprise segments gathering momentum. Firms could now search to enhance inside growth with acquisitions.

What we wrote in October 2022 on the way in which ahead for Pharma has now performed out, with Nifty Pharma outperforming Nifty by 7 share factors. Now, focus can be on corporations’ outlined areas of curiosity for progress.

Taking the cue from this, we analyse the monetary power of high pharma gamers and the seemingly avenue they might pursue. We additionally current a valuation impression to the proposed plan.

Firing on all cylinders

All markets — the US, Europe, Rising Markets (EM) and even API operations — are reporting robust progress in Q1FY24. Solely India, which has been the torchbearer for progress within the final 5 years, has taken a backseat in Q1FY24 outcomes — single-digit progress with one-time NLEM worth changes.

US markets are reporting normalised worth erosion in generics after 2016. Due to this, mixed with the truth that most manufacturing vegetation have exited FDA observations (with few exceptions), new product launches will assist a better progress. The expansion story for branded merchandise in India and EM will keep afloat with product launches. Additionally, corporations predict 50-100 bps enchancment in FY24 EBITDA margins from decrease price of chemical substances and decrease logistics prices.

Generic Revlimid, launched by a lot of the key gamers, is as a lot a contributor to improved monetary well being as operations for the outward gaze. The profitable alternative ought to add ₹500-2,000 crore in earnings for every firm over FY23-26.

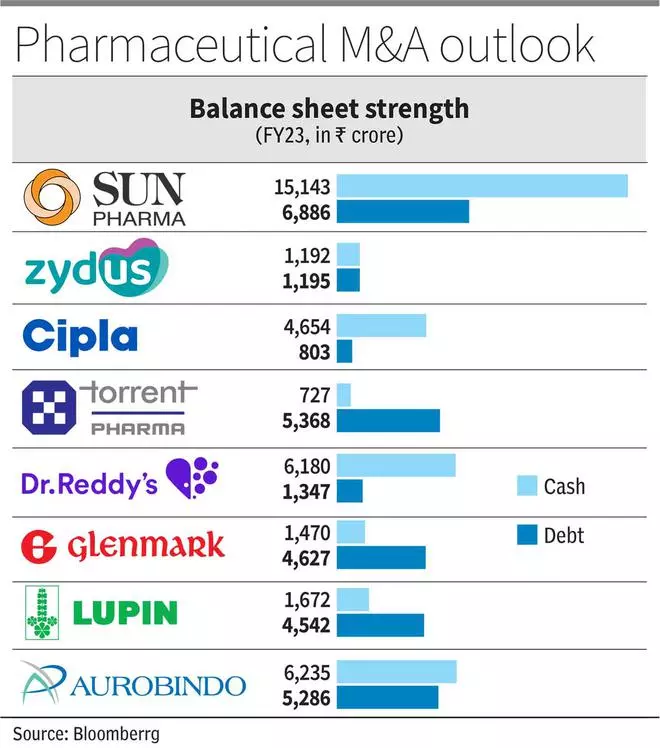

Because of this, stability sheet power will additional amplify for corporations. Solar, Cipla and Dr. Reddy’s have been ‘adverse internet debt’ corporations over the past 5 years and have reported extra money (internet of debt) of ₹4,000-8,000 crore in Q4FY23. Amongst the others, Lupin, Aurobindo and Zydus are additionally anticipated to maneuver to a robust money place within the subsequent one yr.

This robust money place would possibly make it crucial for corporations to pursue increased progress alternatives. Right here’s how we count on key gamers to maneuver ahead:

Greater glide path

Solar Pharma, Zydus Life Sciences, Cipla, Torrent and Dr.Reddy’s fall on this class, unrestrained by debt considerations, with a transparent line of growth and operational strengths.

Solar Pharma could prioritise capital allocation in worldwide ophthalmology and dermatology innovator molecules. The corporate constructed the required gross sales front-end within the US and can want a couple of extra merchandise to leverage the infrastructure developed for Ilumya, Cequa and Winlevi ( in-licensed in 2021) with acquired or developed belongings.

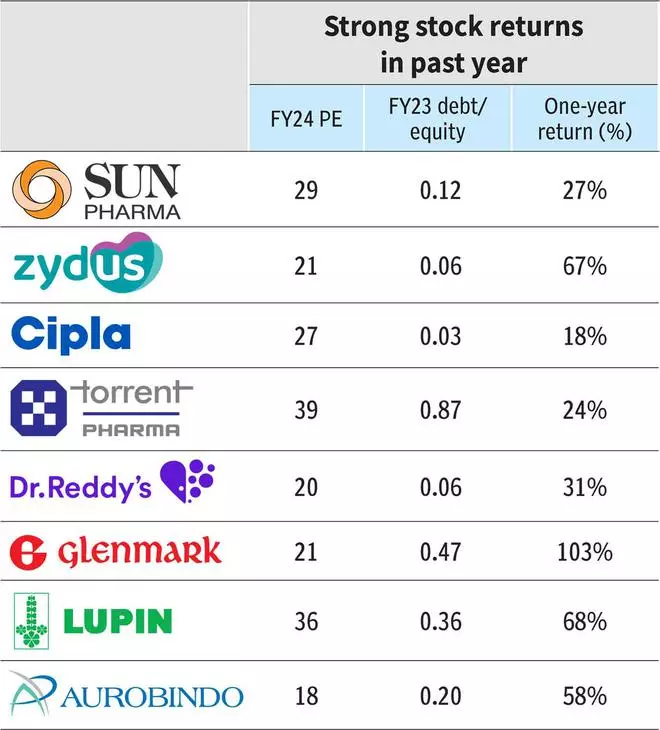

The pipeline belongings embody Deuruxolitinib in Section-III trials (lead asset of acquired Live performance Pharma for $576 million) and extra indication for Ilumya, and an in-house developed anti-diabetes molecule, which ought to have interaction the R&D finances of Solar Pharma sufficiently. Solar Pharma trades at 29x instances FY24 earnings and the present allocation technique of making excessive worth belongings for developed markets justifies the premium valuation and supplies an upward bias relying on belongings’ scientific trial outcomes.

Solar additionally intends to totally consolidate generic derma agency Taro (78 per cent stake at present); this will likely initially be seen negatively except the corporate presents a complete strategic acquire from the acquisition within the dermatological area.

Just like Solar’s speciality portfolio, Zydus Lifesciences has an formidable programme in Saroglitazar and different monoclonal antibodies below investigation for US markets. However the belongings have been launched in India and are developed in-house, implying a decrease price of growth. The corporate R&D pipeline consists of biosimilars and vaccines and calls for increased R&D funding as they progress. The asset growth from Zydus can assist valuations (21 instances FY24 earnings) however is coming at a value of decrease outlay in growth of shopper division, which has been acquired from Heinz in 2019 for ₹4,500 crore. A technique rethink on the division may be anticipated.

With regard to Cipla, there’s Cipla the asset — which is being hotly chased — and Cipla the corporate. Firstly, the corporate. Cipla, on its half, could most definitely bolster its India and Soth Africa operations with large model/advanced product buy in prescription or shopper healthcare segments. Cipla’s money allocation in branded enterprise helps a premium valuation of 27 instances FY24 earnings. The corporate has a robust platform in ‘One India’, and in respiratory and peptides whose inside growth can be a key funding alternative. Commerce generics led by Cipla and carefully adopted by Torrent, Mankind and Dr.Reddy’s, can be a tailwind for the corporate.

On a secondary stage, the corporate could search for belongings within the US that match the respiratory nature of its operations or allied segments. The interior pipeline has a number of inhalation units below growth and may have plant clearance to understand the belongings. The interior pipeline, partnered in some circumstances, ought to drive US market progress, given plant clearance.

Cipla the asset ought to rally its inventory worth within the brief time period whereas within the midst of a sizzling pursuit. The names of Torrent Pharma, Blackstone, Dr.Reddy’s and Bain Capital are making the rounds as a possible suitor to promoter stake (33 per cent). Solely a controlling stake would permit operational synergies to be explored, which would want further buy from follow-on open supply, which is one other short-term set off for the inventory. The extra leverage from acquisition on the eventual consolidated entity would possibly cap the enlargement plans of Cipla + “unknown”. However this stays speculative on the present stage.

Torrent Pharma is more likely to proceed with a predominant give attention to India. Even with Dahej closing FDA points (Indrad facility nonetheless below observations), Torrent Pharma could also be doubling down on Indian markets and extra particularly in complementing its top-tier therapies. Traditionally as nicely, Torrent Pharma has had a robust and successfull acquisition/integration historical past geared toward India. The premium a number of (31 instances FY24 EPS adjusted for amortisation bills) can maintain above common on branded enterprise and India focus.

The online-debt to EBITDA has improved to 1.3 instances as of June 2023 with additional enchancment anticipated. However the Cipla stake may suggest ₹35,000 crore money outgo (Torrent m.cap is ₹65,000 crore), to not point out the open supply. Additionally, core power of synergistic integration capabilities can be stretched to the restrict for Torrent. However the actual synergy is from cross-selling manufacturers, gross sales pressure optimisation in India and entry to respiratory pipeline within the US.

Just like Cipla, Dr.Reddy’s could prioritise investments in India and rising markets by way of product in-licensing or acquisitions in these markets, with secondary precedence to US markets. Dr.Reddy’s made a robust begin to its India portfolio with the acquisition of Wockhardt’s manufacturers in 2020 for ₹1,850 crore however has not introduced home offers of that measurement since. Actually, the corporate has acquired Mayne portfolio of US generics for $100 million in 2023 and has always divested tail-end manufacturers in India on the identical time.

The corporate, with near ₹5,000 crore of internet money, has been disciplined in its strategy to capital allocation (has shed cash-guzzling proprietary growth portfolio). Dr.Reddy’s valuation at 20 instances FY24 earnings lacks the sting of branded-heavy enterprise in India. The Cipla deal, a merger of equals with good home presence, can repair that if the corporate is ready to execute and combine.

Wishing for established order

With debt weighing on sources, Glenmark Pharma, Aurobindo and Lupin could need to stability debt compensation and capital allocation with near-term enchancment anticipated solely in Lupin and Aurobindo.

Glenmark and Dr.Reddy’s have divested Indian belongings/manufacturers both for portfolio rebalancing or to entry fast money which, in flip, favoured Mankind Pharma and Eris Lifesciences.

Glenmark’s R&D funding into Ichnos Sciences, its innovation platform, is a cumbersome build-up of belongings ($70-80 million per yr over 5 to 6 years), however with extremely lagging returns on funding. The corporate must monetise these belongings or lower spending to enhance margins in consolidated enterprise. The 4 scientific trial read-outs anticipated in FY24-25 must be a key monitorable. Glenmark has to promote 7-8 per cent from Glenmark Lifesciences (going by promoter holding obligations) which, coupled with model divestments in India and inside accruals, ought to cut back the numerous internet debt of ₹3,000 crore. Penalty of ₹700 crore to be paid in subsequent two years (anti-trust settlement within the US) could restrict the capex plans of Glenmark within the medium time period.

The inventory, buying and selling at 21 instances FY24 EPS, has re-rated within the present rally from a median 10-12 instances 1-year ahead earnings, pre-empting such modifications and a turnaround in capital allocation.

Lupin has cleared three of its 5 vegetation from US FDA observations and so has Aurobindo Pharma, which can present a big impetus to each the businesses in new product launches. The online debt has additionally come off to ₹1,300 crore in Q1FY24 (₹2,500 crore in Q4FY23) for Lupin, which ought to strengthen the stability sheet as nicely. The corporate has deliberate to ‘restructure’ its API unit however given the constructive turnaround in API trade, and Lupin as nicely, it could equally be seemingly the corporate could not go forward with the plan.

The corporate was in a serious price restructuring effort to enhance its EBITDA margins, which ought to finish in FY24 and add 100-200 bps to margins as nicely. Lupin’s high shelf launch is below approach with Spiriva and can add vital money within the subsequent one yr because the profitable product is with out competitors within the brief time period.

Lupin’s allocation goal could take form because it rebounds, operationally and financially. Lupin now has a robust respiratory portfolio within the US and should look so as to add different belongings to bulk up the US portfolio. Lupin spent ₹1,000 crore on acquisitions in FY23 itself, together with two respiratory manufacturers within the US. The corporate has introduced curbing spends on NCE growth and its inside pipeline could take priority, which incorporates generics: three nasal sprays in inhalation, 4 injectables, two advanced merchandise and two biosimilars. Spending in India could also be needed, given the heavy funding by rivals, and if not executed could have a bearing on its valuation already buying and selling at 36 instances FY24 EPS.

Aurobindo Pharma could also be placing its injectable asset Eugia Pharma in worth unlocking mode for the second time in two years, at a valuation of $2-2.5 billion, which is greater than half of Aurobindo’s valuation. The speciality pharma and injectables unit ($122 million in Q1FY24) has solely not too long ago proven robust progress as injectables have been impacted post-Covid. The corporate’s flagship oral stable enterprise has been rising at a robust tempo and the corporate could put money into smaller ANDA (new generics submitting) acquisition, slightly than inside growth, to avoid wasting on growth timelines.

Aurobindo Pharma could also be nearing its finish of funding part in Penicillin-G facility by PLI scheme the place near $160 million has been invested. Aurobindo additionally has a big funding behind biosimilars for worldwide market totalling $280 million to date. Dr.Reddy’s and Aurobindo plan to be within the subsequent wave of biosimilar launches by 2027-28 whereas Solar Pharma continues to be tentative about its biosimilar initiative. Aurobindo, valued at 18 instances FY24 EPS, lags friends on account of lack of branded enterprise (India). The vaccine, peptide and sophisticated portfolio below growth, whereas robust, are nonetheless generics with a restricted shelf life and therefore can bump up earnings however not valuation outlook.

#Solar #Pharma #Zydus #Cipla #Torrent #Pharma #Reddys #Indian #pharma #Gearing