Our optimistic view on SFH was based mostly on this thesis. At worth of ₹78 in October 2021, the inventory was buying and selling at holding firm low cost of 42 per cent. This was after baking in some conservative assumptions in ascertaining the worth of some property (a number of unlisted investments valued at carrying worth). After largely being range-bound between 70 and 100 for practically two years (until July 2023), the inventory has seen a variety of investor curiosity and wealth creation within the final one yr.

At the moment, put up 250 per cent returns and buying and selling at ₹274.70, the holding firm low cost has shrunk to 13 per cent now (22 per cent, when money and liquid investments are included). Our thesis has largely performed out and we predict there’s not a lot worth left from a holding firm perspective and therefore advocate that traders ebook earnings.

Firm

SFH was spun off from Sundaram Finance as a part of a demerger scheme in 2018. Until then it was a wholly-owned subsidiary of Sundaram Finance with the principle goal of participating within the enterprise of investments, together with investments in monetary companies enablers, fin-tech investments. As a part of the demerger, the investments of Sundaram Finance in corporations engaged in non-financial companies have been vested with SFH.

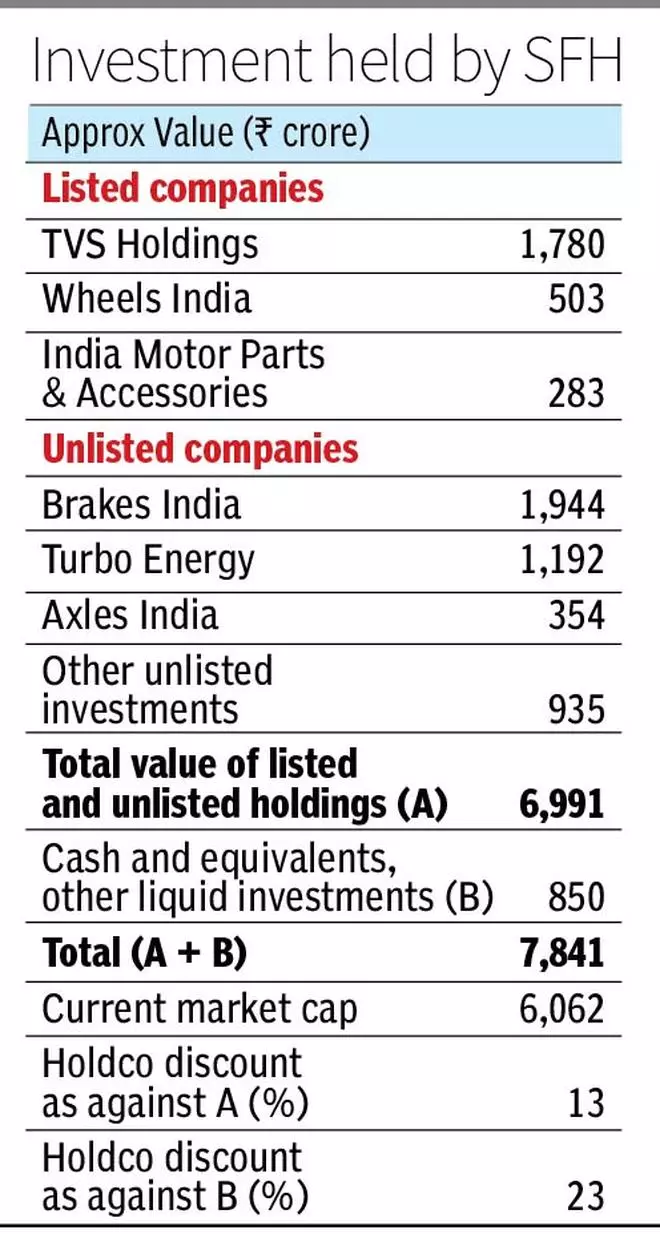

These non-controlling investments include a portfolio of auto element corporations primarily from throughout the TVS group, equivalent to Wheels India, Brakes India, TVS Holdings (previously Sundaram Clayton), Lucas-TVS, and many others. Thus, the corporate had a diversified portfolio of investments within the auto and auto elements house. Nearly the whole worth of the corporate was derived from the value of those underlying investments as the corporate’s standalone operations weren’t materials comparatively.

A lot of the value of those investments was not mirrored in shares of SFH. On the time of our optimistic view, the holding firm low cost was at 42 per cent on a conservative foundation. Among the important unlisted investments have been mirrored at carrying worth, which indicated conservative accounting. Nonetheless, in FY23, the corporate modified its accounting coverage for its investments in affiliate corporations from value foundation to truthful worth.

Therefore, in the present day, once we take into account the worth of its listed investments (based mostly on present market worth) and value of its unlisted investments (reflecting truthful worth now), we get a fairly clear image on the value of its investments. The underlying investments are price practically ₹7,000 crore. As towards this, its present market cap at ₹6,062 crore, implies a 13 per cent low cost now.

The corporate has liquid investments and money of round ₹850 crore and no important liabilities. When that is thought of, the holding firm low cost is larger at 23 per cent. Nonetheless, this isn’t a lot trigger for consolation as 22 per cent low cost is low based mostly on historic information for holding firm reductions, with the reductions having been as excessive as 85 per cent for some listed holdcos.

Additional, if and when the corporate sells any of its holdings to grasp worth, there can be tax liabilities associated to capital positive factors. Therefore, contemplating the whole money and liquid investments, too, to reach at Holdco low cost, whereas not improper, will not be prudent. The corporate’s standalone operations stay comparatively small and immaterial to its financials.

Just lately there have been some optimistic strikes by SEBI with introduction of particular name public sale mechanism for worth discovery of listed holding corporations that meet sure standards. Nonetheless, this will likely not have a lot affect on SFH in whose case the worth discovery has appeared to play out nicely within the final one yr. Additional, the inventory has additionally not reacted to this transfer by SEBI a number of weeks again, whereas different holdcos with deeper reductions have.

#Sundaram #Finance #Holdings #Buyers