Thought experiment

What occurs when an organization continues to reward workers with none enchancment of their productiveness? It can end result within the revenue margins of the corporate getting squeezed. Why? If the rise in salaries per worker is greater than the rise in income per worker, all different prices trending in keeping with income, will imply revenue margins must cut back. If different prices are capped, revenue margins might maintain for some time, however not for lengthy. That is what occurred for the IT corporations in FY22 and FY23, when income development was good, however a rise in salaries and subcontracting prices resulted in decline in revenue margins, and consequently earnings rising slower than income.

Buyers want to use this similar logic to share worth as nicely. What occurs when decrease development is rewarded with greater valuation? Could also be, at finest, inventory returns can maintain for some time (part 1), however ultimately it’ll underperform earnings development (part 2) and if earnings development too is low (part 3) , it may well find yourself being a double whammy for buyers in the long term.

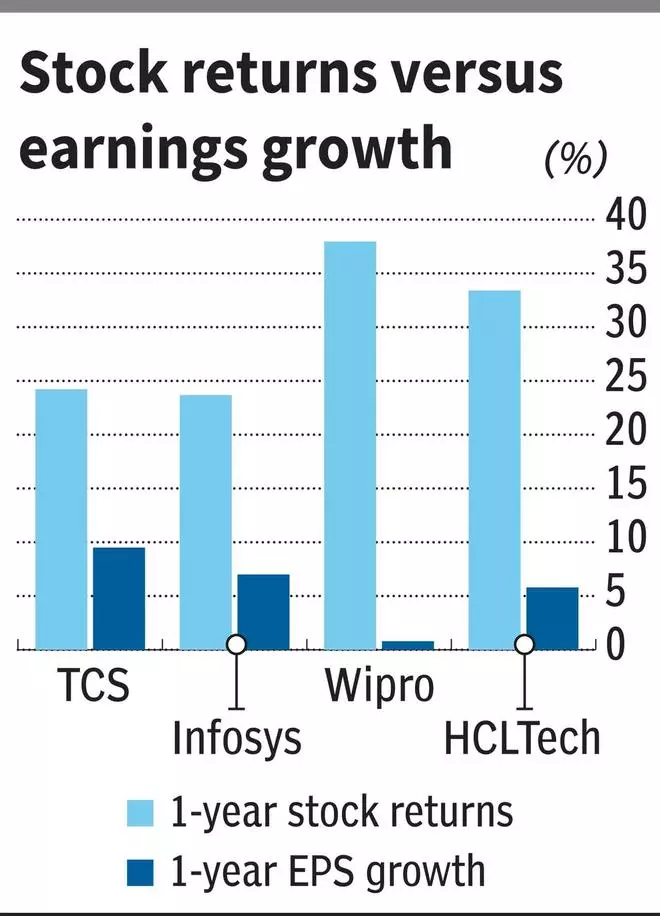

For IT shares, part 1 has performed out nicely over the past one yr as will be seen within the desk beneath, whereby shares have considerably outperformed earnings development.

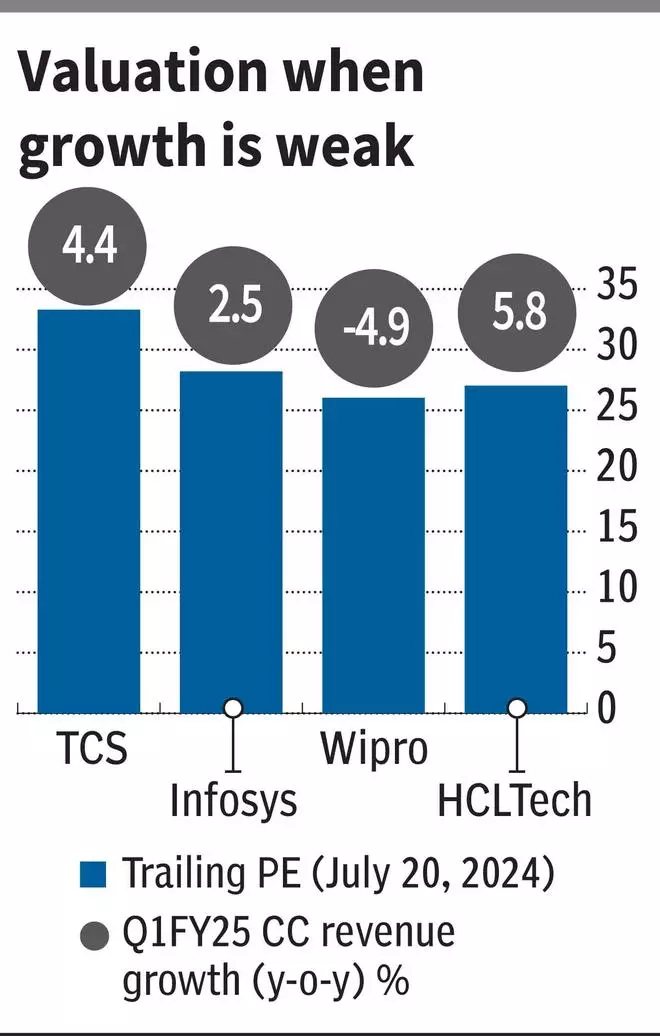

It could be cheap to make an argument that, if valuations had been low cost, then shares can outperform earnings development for some time. However then right here is a few information on how the IT shares are valued now when development is weak, versus how they had been valued when development was booming. We have now thought of the fixed foreign money income development metric right here, as operationally, it is likely one of the most necessary metrics that present data on underlying enterprise traits.

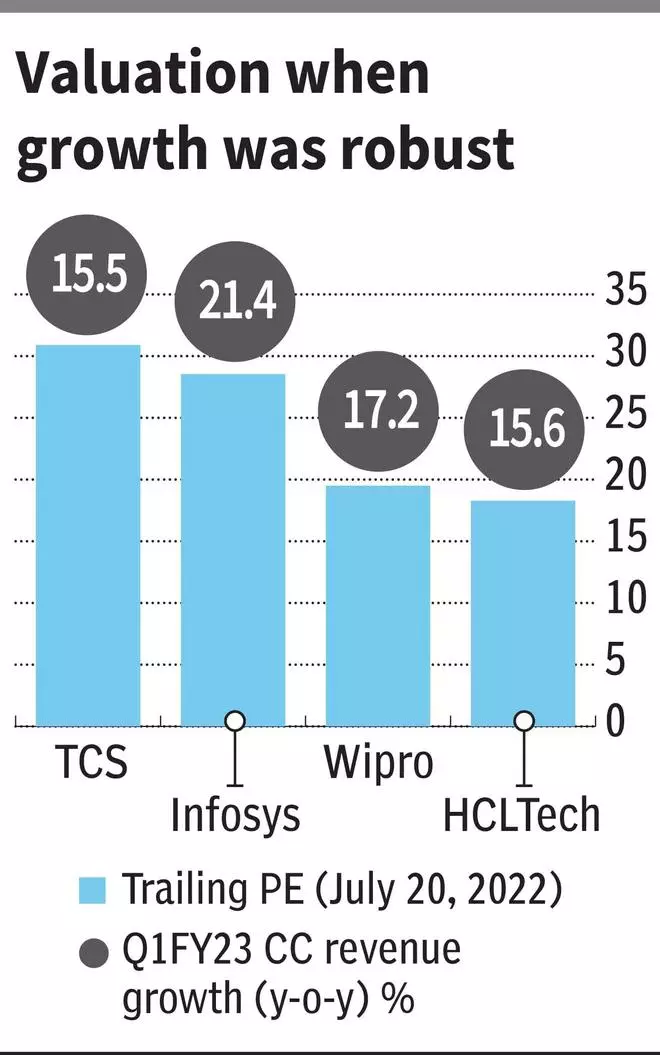

And right here is one other set of information to contemplate. How the IT shares had been valued when development was as weak as now within the earlier decade.

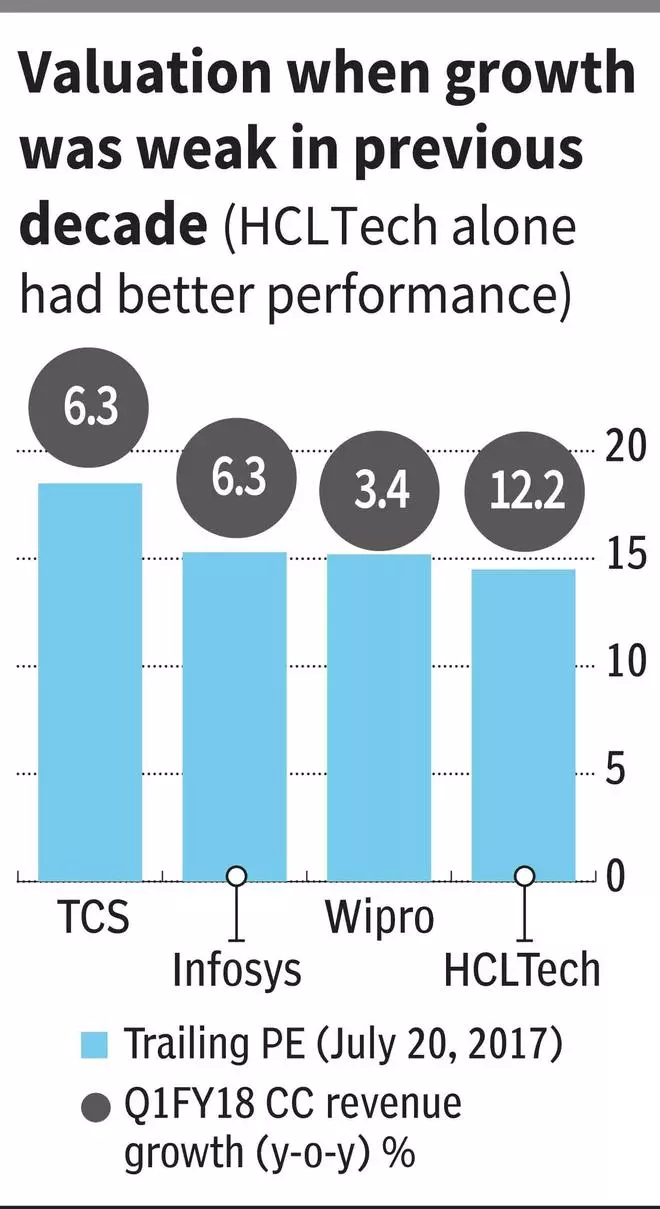

these charts, it’s fairly clear that the expansion over the subsequent few years needs to be considerably excessive to justify present valuations. Whereas buyers are expressing confidence on this, basic information factors and solely cautiously optimistic administration commentary don’t help this investor euphoria.

US GDP development is witnessing a deceleration versus CY23 and recession dangers stay for later a part of this yr or early subsequent yr. IT discretionary spending stays weak as per administration commentary and will be evinced from current quarterly outcomes as nicely. AI impression on IT companies corporations stays unsure. Whereas the businesses are gearing their investments in the direction of constructing AI capabilities, how precisely it’ll disrupt enterprise traits stays unclear.

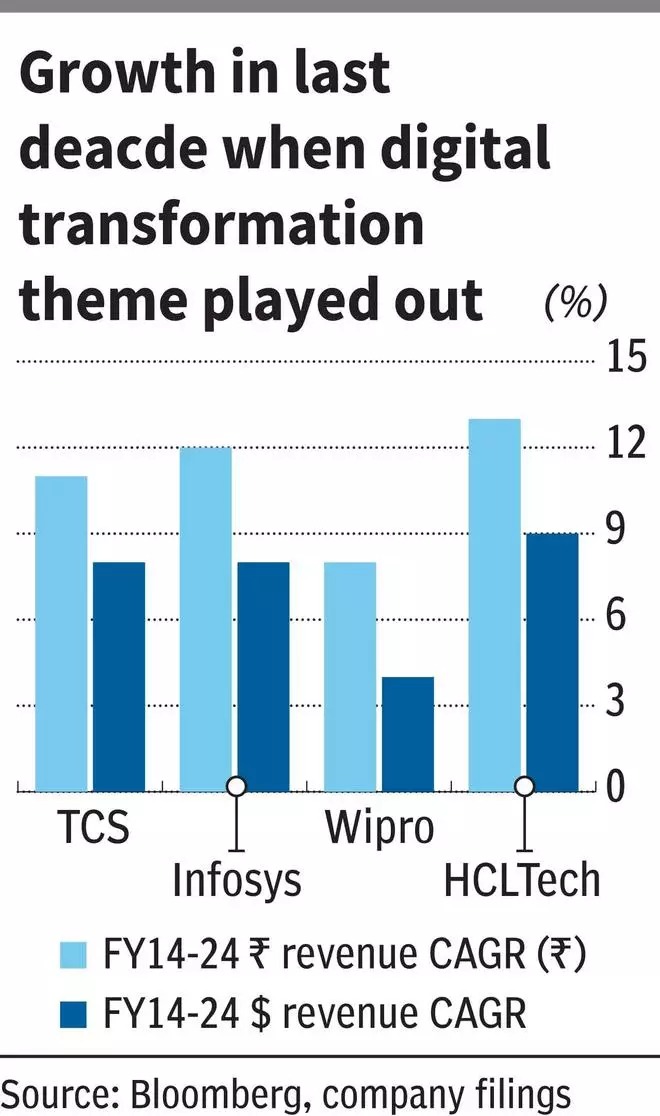

Even when one had been to contemplate the optimistic situation that the IT corporations will capitalise on the traits as they’ve throughout phases of earlier disruptions, right here is one other truth to contemplate. A lot of the digital/cloud revolution in IT companies occurred in the course of the 2014-24 decade. Throughout this era, the widespread adoption by enterprises of digital and cloud companies aside, there was additionally the Covid-driven accelerated digital spending. Throughout this era, the income development for the highest IT companies corporations was as follows:

In rupee phrases, the expansion within the earlier decade will be thought of fairly respectable. Nevertheless, it must be famous that this got here with the advantages of foreign money depreciation as will be seen from the distinction in income development in INR and USD phrases. So two issues must be stored in thoughts right here. Whereas AI theme can profit IT companies corporations, it might be difficult to repeat the expansion of earlier decade, given their bigger measurement right this moment. Development tapers as measurement will increase. Additional, whether or not foreign money advantages of the earlier decade will play out this decade too must be contemplated upon.

After the current upside in IT shares, the query that arises is: Is the worst over given the shares’/ Nifty IT underperformance from their prior peak in December-January 2022? Wanting on the information above, given present valuations and fundamentals, buyers might should endure a extra extended part of sub-par returns.

#TCS #Infosys #Wipro #HCLTech #shares #rally #derailed #easy #math