This quote, attributed to novelist and thinker George Santayana, is ringing sound and robust at the moment within the IT sector, put up the shocker of a outcome from Infosys. Because the pandemic-induced want for digitisation, mixed with unprecedented fiscal and financial stimulus, resulted in a major however short-term bump-up in expertise spending, the so known as ‘digital transformation’ wave erased reminiscences of the previous.

Inventory valuations throughout the board zoomed well beyond historic vary and the truth that the Indian IT sector was a mature business with at finest long-term progress prospects of excessive single-digit to low double-digit progress was forgotten. Analysts, market commentators, buyers and fund managers and even a couple of managements fell prey, once more.

Overly optimistic promote aspect earnings progress estimate and worth targets, buyers pouring in cash at any worth and managements fixing share buyback worth at irrational ranges are some examples and function a stark reminder of the previous cycles forgotten.

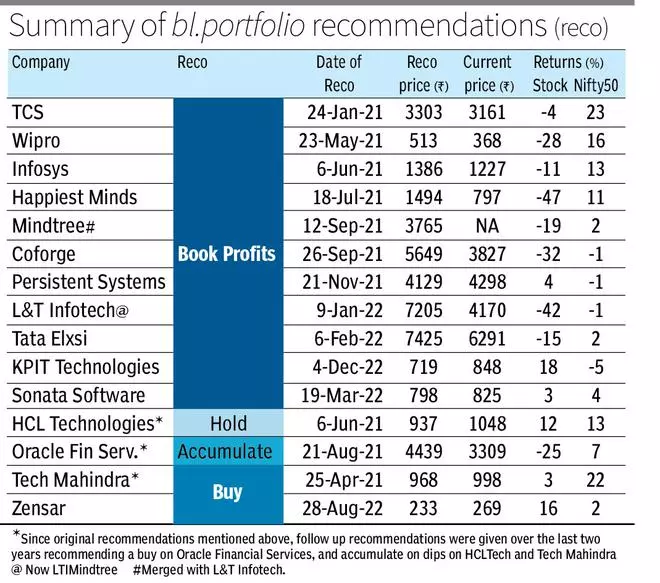

Nonetheless, at bl.portfolio, we had began flashing the crimson sign on the IT shares by June 2021 by once we had beneficial buyers to guide earnings within the high 3 IT shares then — TCS, Infosys and Wipro — and adopted up with suggestions to guide earnings in a lot of the mid-cap IT shares, which have been buying and selling at their costliest valuations put up the dotcom mania.

The rationale for warning was easy. Whereas the basics of the sector have been sturdy, with many Indian IT companies gamers being the best-in-class corporations, valuations throughout the board (barring a couple of) had manner outpaced fundamentals.

Within the investing world, that’s akin to binging on the following few days’ lunch at the moment, which suggests you’ll have to find yourself rationing or could also be even going with out meals over the following days.

That decision performed out, with buyers within the sector being starved of returns for the reason that Nifty IT index peaked in January 2022 at 39,370. It’s down 32 per cent since then. Fairly a carnage it has been, with shares like Wipro and some different mid-cap shares down by 50 per cent or extra. You’ll have to journey again to 2007-09 to witness this stage of carnage within the Indian IT sector.

Precisely a 12 months again, we had given our IT sector outlook in our Huge Story titled, ‘Is the celebration over for IT shares’ in bl.portfolio version dated April 24, 2022, whereby we had outlined explanation why it was time for bullish buyers to sober up. With shares certainly sobering up, allow us to now assess the place issues stand a 12 months on and what’s in retailer.

Valuations are higher now

‘What might be extra exhilarating than to take part in a bull market by which the rewards to homeowners of companies grow to be gloriously uncoupled from the plodding performances of the companies themselves. Sadly, nevertheless, shares can’t outperform companies indefinitely.’ – Warren Buffett

Within the two-year interval from February 2020 (pre-Covid highs) to March 2022, the Nifty IT index was up by 120 per cent. Guess what the rise in income and earnings of the index in the identical time interval have been? A extra sober 15 and 27 per cent respectively!

What precisely justifies paying 120 per cent extra for a product whose productiveness elevated by 27 per cent? In all probability the great tales of how digital transformation will guarantee excessive progress charge for longer, and the information that inflation is transitory and rates of interest will stay low for longer if not perpetually.

As these tales obtained debunked one after the other, so did the irrational exuberance on shares within the sector. Within the quick run, tales can rule inventory costs, however in the long term, it’s all the time the numbers that matter. That is the best way issues have performed out within the IT sector from the time of the Y2K/dotcom growth until now, and the longer the tales took time to get debunked within the markets, the extra painful the correction was.

One logical justification for the share costs being decoupled from earnings progress might be if shares have been undervalued earlier. Nonetheless, this doesn’t apply to a lot of IT sector/IT shares, which have been very effectively found by markets. Simply earlier than the pandemic hit, on a trailing PE foundation, the Nifty IT index was buying and selling at round a 5 per cent premium to its 5 and 10-year common of round 19 instances, implying that it was positively not undervalued. Within the absence of any vital acceleration in long-term earnings progress potential (which was absent), there was not a lot of a case for the inventory costs to considerably outperform earnings progress in 2020-2022.

Evaluation additionally exhibits that the trailing 5-year earnings CAGR (since 2017) of the Nifty IT index and the highest 4 IT companies corporations has ranged 7-12 per cent. There isn’t a vital proof of sustainable acceleration in earnings progress charge to warrant larger valuation versus historic vary.

Now, after the correction, are numbers and inventory costs in sync? Whereas not completely, it’s extra affordable with the index up by 60 per cent from February 2020 to now, whereas earnings are up by 36 per cent in the identical interval. The takeaway right here is that, a lot of the froth has been squeezed out.

Underneath regular conditions, it may be okay to begin shopping for into IT shares regularly. Nonetheless, it’s not clear how the worldwide financial system goes to be over the following few years, which makes the choice to take a position dicier.

Bleak international progress outlook

Till earlier than the collapse of the Silicon Valley Financial institution in March, the vary of financial predictions on the US financial system was as huge because it may ever be. Expectations of economists and market members ranged from laborious touchdown to tender touchdown to no touchdown. Whereas the primary risk was what the bears have been anticipating, the opposite potentialities have been extra supportive of the bulls’ outlook. Nonetheless, put up the banking disaster, the outlook for the financial system has obtained extra gloomy, tilting it extra in favour of bears.

The US Fed’s full 12 months financial projections point out the potential of a recession in 2022. Additional, the lately launched World Financial Outlook by the IMF forecasts international progress to fall to 2.8 per cent in 2023, from 3.4 per cent in 2022. However the extra necessary factor to notice are these – one, the forecast for superior economies is extra dire, with progress anticipated to greater than halve, from 2.7 per cent in 2022 to 1.3 per cent in 2023, with risk of it slipping under 1 per cent if monetary stress intensifies. Two, the IMF now expects international progress to settle at 3 per cent 5 years out, which is the bottom medium-term forecast in many years.

IT sector fortunes are instantly linked to international financial prospects, particularly the superior economies. The US accounts for 50-60 per cent of revenues for the highest 4 Indian IT companies gamers and Europe accounts for 25-30 per cent of revenues. The worldwide slowdown is already getting mirrored within the outlook of corporations, with Infosys now forecasting bruising decline in progress charges with fixed forex (CC) income progress for FY24 anticipated at 4-7 per cent versus a stellar 15.4 per cent in FY23. HCLTech has guided for FY 24 CC progress of 6-8 per cent versus 13.7 per cent in FY23. TCS doesn’t give steerage however was very cautious in its commentary.

Additional, commentary from corporations clearly signifies slowdown past the main BFSI vertical, implying a extra broad-based slowdown taking maintain.

IT spending will probably be sturdy when corporations in superior economies are benefitting from sturdy GDP progress, however when their income and margins get hit, at some stage their tech spending will face the axe, too. Consensus forecasts (Bloomberg) are for earnings of S&P 500 corporations to say no by 7 per cent in 2023, however this could intensify if a recession performs out.

Each time a recession/slowdown has taken maintain, the shares too have had deep corrections. The one distinction in 2020, although, was the fast rebound. That is probably not forthcoming this time as the extent of stimulus pumped into the financial system was a key issue driving that rebound. Each Central Banks and governments having been jarred by inflation, will probably be very cautious in stimulating the financial system this time round.

The tsunami of job cuts by tech corporations like Amazon, Microsoft and Accenture, together with of their cloud/digital companies, doesn’t lend optimism on a fast rebound.

Different transferring elements

Apart from broader macro uncertainties, there are a couple of different transferring elements for corporations within the sector to cope with. For one, what’s going to be the influence of the brand new wave of disruptive synthetic intelligence storming the expertise area? Generative AI, as this area is named, has garnered numerous consideration for the reason that launch of ChatGPT. It has showcased immense potential for automation and displacing human duties not simply in non-tech jobs, however even in tech-related duties like software program coding. Thus, it requires monitoring on how this impacts the IT service corporations.

That mentioned, each time disruptive modifications have performed out, Indian IT has tailored effectively. For instance, when the Cloud/SaaS wave was accelerating in the midst of final decade, there was 2-3 12 months adjustment interval because the legacy enterprise of IT corporations shrank and it took some time for them to make their digital enterprise the primary driver. Throughout this era IT shares gave flattish to unfavorable returns. Will there be comparable disruption this time? Traders must issue this. The winners and losers could also be totally different from the earlier part of disruption.

One other factor to think about is, what would be the influence of a steady rupee versus the USD throughout a recession? Throughout earlier recessions, there was a major depreciation in rupee vs the USD that acted as cushion for the financials of IT corporations. With India being seen now as shining gentle in a weak international financial system, the rupee could fare higher.

Thus, though as mentioned below ‘Valuation’ the froth seems to have been squeezed out, the various uncertainties and disruptions mentioned above proceed to name for persistence in the case of investing within the IT sector now.

Investor playbook

That there will probably be a major slowdown in IT sector attributable to international headwinds was foreseeable at first of the 12 months. But the Nifty IT index rallied by 10 per cent from begin of the 12 months until mid-February, solely to crash once more! Thus, the endgames are often tough and might be fairly unstable.

Elementary buyers should all the time be cautious to protect in opposition to market narratives and keep on with a pure valuation-based strategy. As mentioned, the uncertainties are quite a few now. The higher the uncertainty, the higher it’s essential to cut price for higher worth earlier than shopping for shares. One should deal with the pandemic-induced extra progress in IT sector as an aberration (for now). The valuations throughout this part have been a good higher aberration.

The latest correction within the sector could also be seen as the start of the tip of the bear marketplace for IT shares and worth would possibly emerge someday in the course of the course of the 12 months. On this context, inventory valuations ideally at a reduction or at the very least in step with the typical valuation of pre-Covid years may be an excellent place to begin to think about investing within the shares. Whereas this isn’t a holy grail strategy and may range from inventory to inventory and as new info flows, for now it’s a good benchmark for assessing the shares.

.jpg)

#bear #market #shares #ready #completely satisfied #hours