Consolidation and growth

UltraTech Cement goals to take its put in capability from the present 150 million tonnes (mt) to 200 mt by FY27-end. The corporate appears to be on monitor to ship on its targets. The corporate added 15 mt (commercialised and contributing to revenues) within the final one 12 months and expects so as to add equally within the subsequent three years.

UltraTech has constructed near half its present capability by way of acquisitions. This consists of 21 mt from Jaypee Cements ($110 EV/tonne in July 2016), 6.2 mt from Binani ($140 EV/tonne in November 2018) and consolidated 14.6 mt from Century Textiles ($95 EV/tonne in Could 2018).

Within the final six months, the corporate has accomplished two extra — Kesoram Cements was acquired in a share-swap deal (at an implied valuation of $80 EV/tonne) in November 2023; in two transactions beginning June this 12 months, UltraTech acquired a controlling stake in India Cements at a median of $110 EV/tonne for 14.7-mt capability in South India.

Total, the 200-mt capability goal implies a quantity CAGR of 11 per cent until FY27, if delivered. In contrast with trade capability utilisation of 70 per cent, UltraTech has operated at 85 per cent in FY24 and is predicted to take care of the identical.

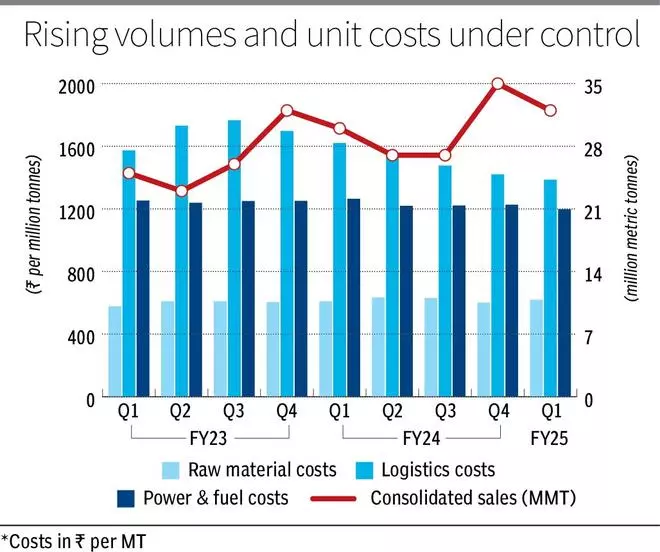

Effectivity enchancment

Major prices in cement manufacturing relate to uncooked supplies, energy and gas, and logistics. The corporate is about to enhance the 2 controllable elements, energy and logistics, considerably within the subsequent two years. Lead distances are focused for controlling logistics prices. The lead distance has decreased 15 km in Q1FY25 to 385 km for the consolidated operations. This resulted in 5 per cent/2 per cent year-on-year and quarter-on-quarter enchancment in Q1FY25 logistics prices on a per tonne foundation. The corporate has a goal to cut back by 25 km in subsequent two years and is positioned to positively shock on that entrance, going by the Q1 efficiency. The current acquisitions play a component in quantity development and in addition add to the geographical unfold within the nation, which is the premise for enchancment in lead distances.

In contrast with ₹7 per unit price of conventional energy, WHRS (waste warmth restoration system) prices a fraction and inexperienced energy prices ₹4 per unit. The corporate goals to have 60 per cent energy from WHRS and inexperienced energy by FY27 and 85 per cent by FY30. The corporate has improved from 25.7 per cent inexperienced energy in Q4FY24 to 29.4 per cent in Q1, which resulted in 2 per cent enchancment in gas price per tonne within the quarter.

Financials, valuation

The corporate has a excessive quantity development goal mixed with profitability enchancment. The consensus estimates count on income and PAT development of 12 per cent and 25 per cent CAGR in FY24-26 owing to twin affect. That is mirrored within the valuation premium accorded at 35 instances one-year ahead EPS in contrast with 10-year common of 28 instances.

However there are headwinds going through the corporate too. The realisations have been declining at 3 per cent within the final two quarters. This might be attributed to election-related pull again in demand and better aggressive depth. Whereas the election affect is a one-time phenomenon, the latter can be a structural issue. Uncooked materials prices, too, have been benign as crude prices have softened. This might be anticipated to inch up within the coming quarters even when a pointy rise will not be anticipated.

The first drivers for the trade are total demand and effectivity enchancment, and UltraTech is properly positioned on each the fronts. The rising demand in India has been met with elevated provide (leading to flat costs). India’s cement trade added 7 per cent capability in FY24 to achieve 626 mt and the general demand is predicted to maintain within the 6-8 per cent development vary in FY25. A bounce-back in rural housing is predicted to take the lead from city housing demand, on the again of sturdy monsoons, and are available out of sustained weak point in rural economic system within the final two years. The formidable nationwide infrastructure plan has sustained its momentum post-elections with capex outlays maintained at larger ranges.

On anticipated trade development of 6-8 per cent in volumes development, UltraTech can ship a 200-basis level premium together with enchancment in price metrics. However the valuations ought to restrain traders to holding the inventory in the intervening time.

Why

On monitor for capability growth

Energy and logistics prices to say no

#UltraTech #Cement #Buyers